The battle for Bakken NGLs could prove a costly one for ONEOK (OKE). Kinder Morgan (KMI) is taking on the basin leader with its decision to convert Double H Pipeline from crude to NGLs service. KMI has several options to take market share, according to East Daley’s review of the Bakken midstream.

The 462-mile Double H Pipeline runs adjacent to OKE’s Bakken NGL and Elk Creek pipelines, connecting operators in the Williston Basin to the Guernsey market in Wyoming. We expect a dual shock to crude oil and NGL markets from the Double H conversion, with impacts to ripple through the Rockies and Midcontinent.

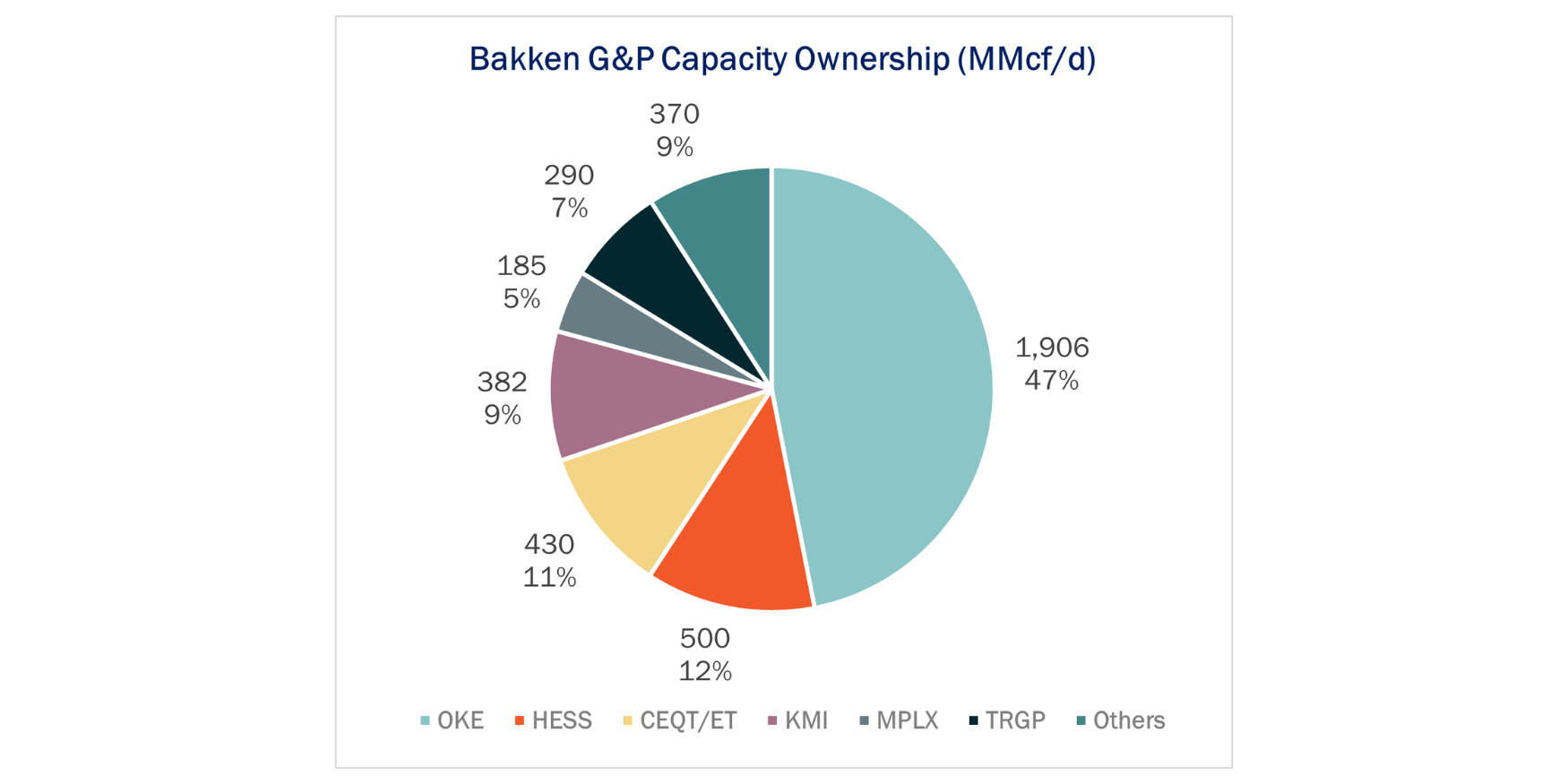

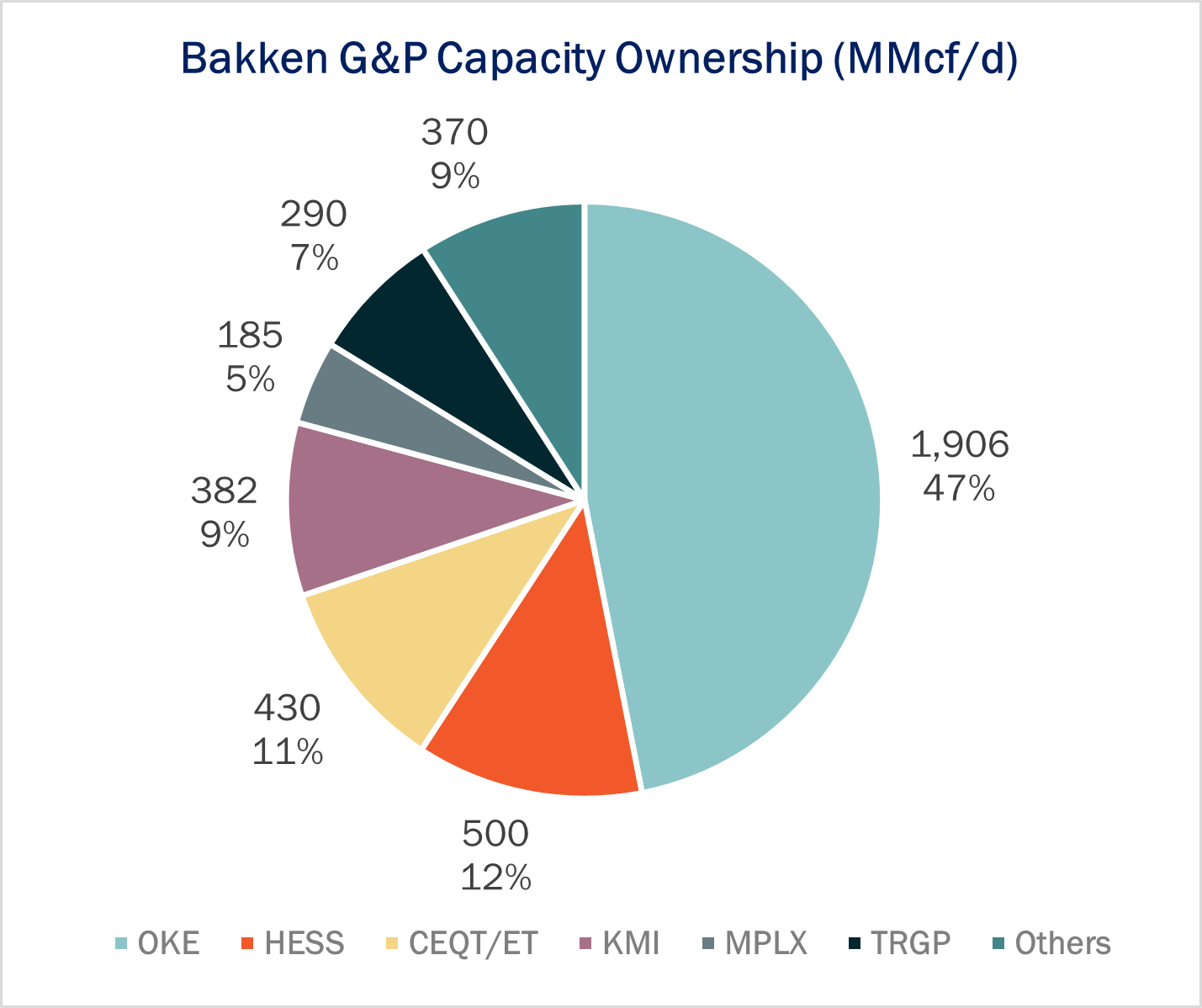

It won’t be easy for KMI to knock ONEOK off its throne. ONEOK would still be the dominant player as the company controls about 47% (~1.9 Bcf/d) of the gas processing capacity in the Bakken, according to plant data in the NGL Hub Model (see figure).

But volumes from other midstream players may be up for grabs. Hess Midstream (HESS), Energy Transfer (ET), MPLX and Targa Resources (TRGP) combine for 1.4 Bcf/d of gas processing capacity in the basin and could benefit from diversification on Double H.

Kinder Morgan will need to build out connections between Double H and (possibly third-party) plants, as well as partner with other pipelines to move NGLs to market (Conway or ideally Mont Belvieu). Two options are ET’s White Cliffs Pipeline from the Denver-Julesburg Basin, or Williams’ (WMB) Overland Pass Pipeline. ET also has a presence in the Bakken G&P business via its acquisition of Crestwood Equity (430 MMcf/d of processing capacity), which could help fill up Double H and allow ET to recover those barrels for its downstream NGL assets.

According to East Daley’s Financial Blueprints, a ~30 Mb/d drop in OKE’s Bakken NGL Pipeline gathering volumes and Elk Creek long-haul volumes would result in a ~$85MM impact to annual EBITDA. This hit represents ~8% of OKE’s combined Bakken NGL and Elk Creek pipeline earnings, or 1% of total company earnings for FY24. The impact on OKE could be offset by higher-than-expected Bakken production, specifically from increased ethane recovery. On the downside, there may be rate risk as well, but we expect joint rates between Double H and downstream pipes would be in line with current Elk Creek rates (~$0.21/gal). — Ajay Bakshani, CFA Tickers: COP, CVX, DVN, EPD, ET, KMI, OKE.

Join Our Next Webinar: Natural Gas Heading into a Super-Volatility Cycle

East Daley is here to help you get ahead of volatility. Don’t miss this exclusive webinar diving into the next volatility cycle in Natural Gas on August 7th at 10 AM MST. Register here.

Propane Supply and Demand Report and Data Set: Coming Soon

Propane Supply and Demand is a Data File & Report that includes historical and forecasted supply and demand components for propane including gas plant propane production, refinery propane production, domestic demand from steam crackers and other consumption, plus propane (LPG) exports. Learn more about the Propane Supply and Demand Report and Data Set.

Sign Up for the Crude Oil Edge

East Daley’s Crude Oil Edge provides weekly updates on the US crude oil market including supply and demand fundamentals, basin-level views, and analysis of market constraints and infrastructure proposals. We explore sub-basin dynamics and provide market insights on crude oil flows, production growth, and import and export characteristics. Sign up now for the Crude Oil Edge.

The Daley Note

Subscribe to The Daley Note (TDN) for midstream insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices and EDA research likely to affect markets in the short term.