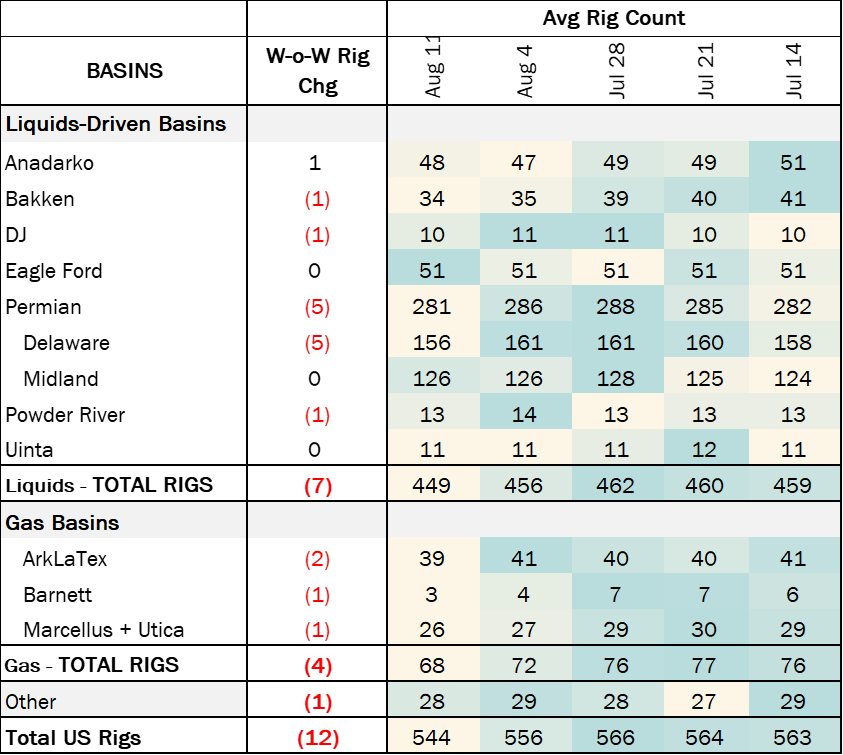

Executive Summary: Rigs: The US rig count decreased by 12 for the August 11 week, down to 544 from 556. Infrastructure: LOOP has missed out on growth in crude oil exports. Storage: East Daley expects a pull of 401 Mbbl from commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending August 23.

Rigs:

The US rig count decreased by 12 for the August 11 week, down to 544 from 556. Liquids-driven basins saw a net loss of 7 rigs, moving the count from 456 to 449. The Permian lost 5 rigs, all from the Delaware sub-basin. The Bakken, Denver-Julesburg and Powder River basins each lost 1 rig. The Midland Basin held steady at 126 rigs. The Anadarko basin gained 1 rig.

In the Bakken play, operator Iron Oil removed 1 rig. In the DJ Basin, operator H&R Well Services dropped 1 rig. In the Delaware, Mewbourne Oil released 2 rigs, and EOG Resources saw a decrease of 1 rig. Also in the Delaware, ConocoPhillips and Exxon each dropped 1 rig. In the Powder River Basin, Rockies Resources Holdings dropped 1 rig.

Infrastructure:

The Louisiana Offshore Oil Port (LOOP) is in many respects a premiere terminal asset, yet has missed rapid growth in Gulf Coast crude oil exports. LOOP’s location and nearby pipe constraints pose challenges to ramping exports, a key factor pushing proposals for other deepwater terminals.

Located in the Gulf of Mexico about 20 miles south of Port Fourchon, LOOP boasts several superlatives. It is the only deepwater terminal in the US, meaning LOOP is the only dock capable of loading a very large crude carrier (VLCC) without lightering – eliminating a time-consuming and expensive process. Owned by Shell (46.1%), MPLX (40.7%) and Valero Energy (3.2%), LOOP can load up to 100 Mb/hour of crude and connects to a major refinery hub.

But is LOOP a good match for exports? Southeastern Louisiana is far away from the Permian and Bakken, the two main sources of supply growth. East Daley forecasts Permian Basin oil production to increase by ~5% in 2024 and ~11% in 2025, according to the Production Scenario Tools. Bakken production grows 5% in 2024 and 8% in 2025. The light sweet barrels from the Bakken and Permian are ideal for export, but LOOP may not be the answer.

As currently configured, barrels imported on LOOP are delivered to the St. James market and to tanks in Clovelly, LA with 70+ MMbbl of storage capacity. LOOP’s owners also operate refineries in the area, including Marathon Garyville (597 Mb/d of capacity), Valero Saint Charles (340 Mb/d) and the Shell Norco refinery (500 Mb/d). Using East Daley’s Crude Hub Model, we project St. James refinery demand to remain flat through 2024 and 2025.

As currently configured, barrels imported on LOOP are delivered to the St. James market and to tanks in Clovelly, LA with 70+ MMbbl of storage capacity. LOOP’s owners also operate refineries in the area, including Marathon Garyville (597 Mb/d of capacity), Valero Saint Charles (340 Mb/d) and the Shell Norco refinery (500 Mb/d). Using East Daley’s Crude Hub Model, we project St. James refinery demand to remain flat through 2024 and 2025.

In order to boost exports from LOOP, investors would need to build more infrastructure to Clovelly. Zydeco Pipeline, the main system delivering barrels into Clovelly, runs nearly full and was at 87% utilization in May ‘24 (the latest data). Moreover, Zydeco and surrounding pipes are configured to carry crude oil to the refiners in St. James, rather than toward LOOP.

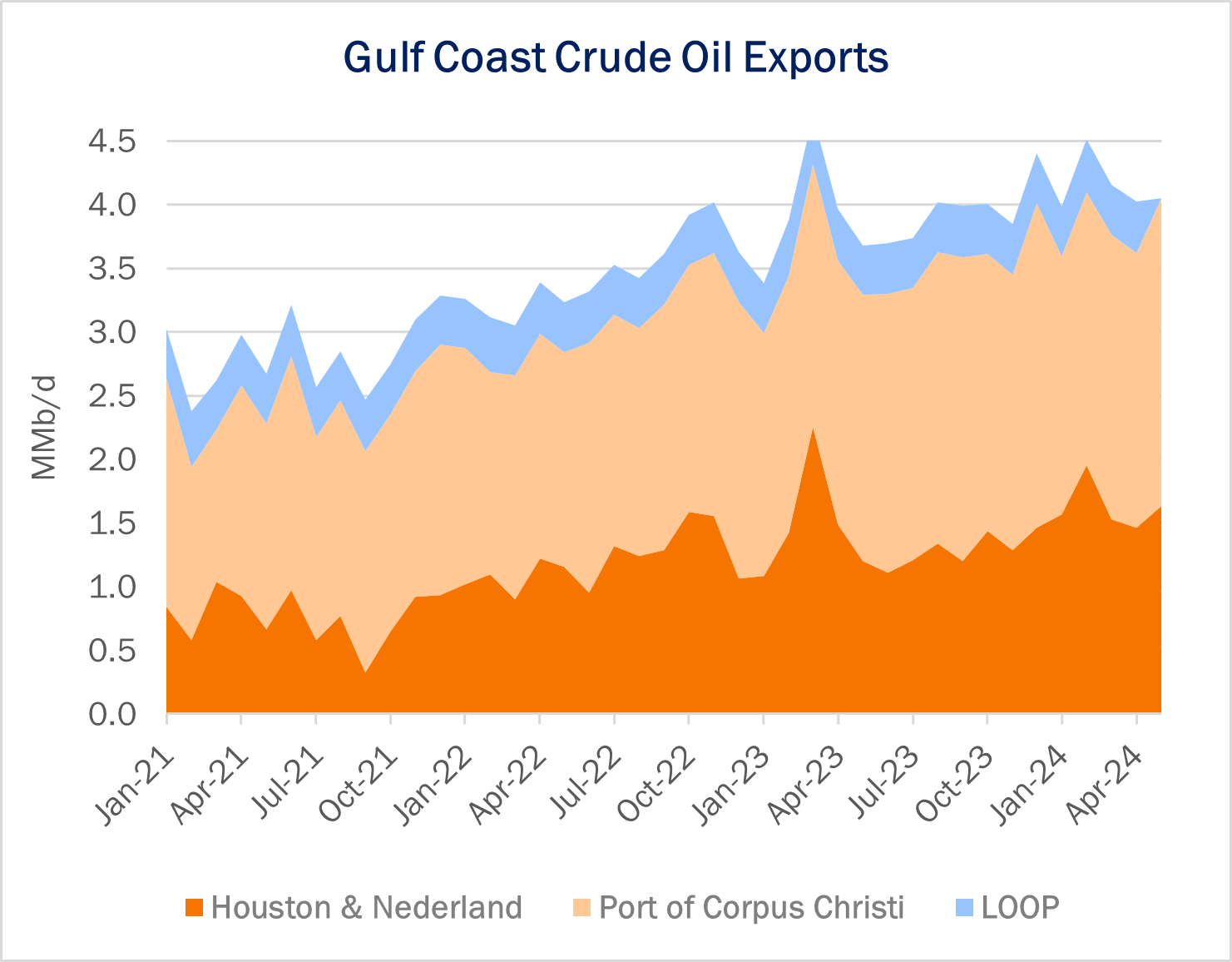

Given these hurdles, LOOP plays a limited role supporting oil exports. PADD 3 (Gulf Coast) crude oil exports have averaged over 4.1 MMb/d YTD in 2024 (through May ’24), according to EIA data, up 1.3 MMb/d since 2021. Yet LOOP only accounts for ~10% of those exports, while terminals located in the Port of Corpus Christi and around Houston and Nederland have driven growth (see figure).

East Daley does not believe pipe connectivity around Clovelly will improve any time soon, as we expect LOOP will continue to operate mainly as an import facility. Instead, the industry is competing to build up to four deepwater terminals offshore Texas that could also load VLCCs without lightering. The four proposals are Sentinel Midstream’s Texas GulfLink, Energy Transfer’s (ET) Blue Marlin, Enterprise’s (EPD) SPOT, and Phillips 66’s (PSX) Bluewater Texas. With existing ports nearing capacity on the Gulf Coast, exporters will need new infrastructure to move Permian and Bakken barrels to market.

Storage:

East Daley expects a 401 Mbbl withdrawal from commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending August 23. We expect total US stocks, including the SPR, will close at 800 MMbbl.

The US natural gas pipeline sample, a proxy for change in oil production, decreased 1.4% W-o-W across liquids-focused basins. Samples decreased by 3.2% in the Gulf of Mexico, 1.2% in the Permian, and 0.9% in the Williston. The decline was offset by samples increasing 1.7% in the Barnett. The Williston Basin and the Rockies have a high correlation between gas volumes and crude oil volumes, whereas the Permian Basin and Eagle Ford basins’ correlation is less than 45%. We expect US crude production to remain flat at 13.4 MMb/d.

The US natural gas pipeline sample, a proxy for change in oil production, decreased 1.4% W-o-W across liquids-focused basins. Samples decreased by 3.2% in the Gulf of Mexico, 1.2% in the Permian, and 0.9% in the Williston. The decline was offset by samples increasing 1.7% in the Barnett. The Williston Basin and the Rockies have a high correlation between gas volumes and crude oil volumes, whereas the Permian Basin and Eagle Ford basins’ correlation is less than 45%. We expect US crude production to remain flat at 13.4 MMb/d.

According to US bill of lading data, US crude imports increased by 18 Mb/d W-o-W to 6.67 MMb/d. More than 60% of the supply originated from Canadian pipelines into the US, with the remainder largely coming from ships carrying crude from Mexico, Venezuela and Argentina.

As of August 23, there was ~90 Mb/d of refining capacity offline, including downtime for planned and unplanned maintenance. EDA expects gross crude inputs into refineries to increase by ~90 Mb/d W-o-W, coming in at 16.8 MMb/d.

Vessel traffic monitored by EDA along the Gulf Coast decreased W-o-W. There were 21 vessels loaded for the week ending August 23 and 23 the prior week. EDA expects US exports to be 3.98 MMb/d.

The SPR awarded contracts for 3.25 MMbbl to be delivered in August 2024. The SPR has 378 MMbbl in storage as of August 23, 2024.

Regulatory and Tariffs:

Presented by ARBO

Tariffs:

Enbridge Pipelines (FSP) LLC A temporary discount was established applicable to the International Joint rates of heavy crude petroleum. FERC No 3.45.0 IS24- 685 (filed Aug 9, 2024) Effective September 1, 2024.

Red River Pipeline Company LLC The high viscosity charge was canceled as it is no longer needed based upon the pipeline receipts. A high viscosity penalty was added for crude petroleum in excess of 8 centistokes at 60 degrees F to limit high viscosity crude from entering the pipeline’s common stream, slowing the flow rate and reducing capacity. FERC No 2.17.0 IS24- 667 (filed July 31, 2024) Effective September 1, 2024.

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at [email protected] or phone at 202-505-5296. https://www.goarbo.com/