Executive Summary:

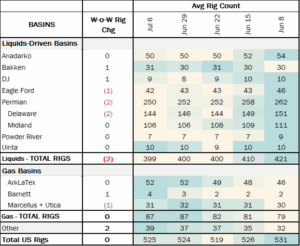

Rigs: The total US rig count increased to 525 during the week of July 6.

Infrastructure: The Bureau of Land Management approved a rail terminal expansion in the Uinta Basin that would boost takeaway for producers.

Storage: East Daley expects a 275 Mbbl withdrawal from storage for the week ending July 18.

Rigs:

The total US rig count increased during the week of July 6 to 525. Liquids-driven basins increased by 1 W-o-W from 400 to 399.

- Permian (-2):

- Delaware (-2): EOG Resources, ConocoPhillips

- Eagle Ford (-1): Grit Oil & Gas Management

- Bakken (+1): Exxon

- Denver-Julesburg (+1): Vessels Tom

Infrastructure:

Uinta Basin oil producers could see much-needed takeaway added soon after the Bureau of Land Management (BLM) approved a rail terminal expansion under an expedited review process.

Coal Energy Group 2, a subsidiary of Wildcat Midstream, seeks to expand the 270-acre Wildcat Terminal near Helper, UT by installing additional unloading bays, upgrading the loading systems and building a dedicated tank farm. The terminal can currently move 20 Mb/d of waxy Uinta crude from tanker trucks onto unit-train rail cars, according to the BLM application; the project would take loading capacity to ~100 Mb/d. The BLM approved the proposal on July 7 after a 14-day environmental review.

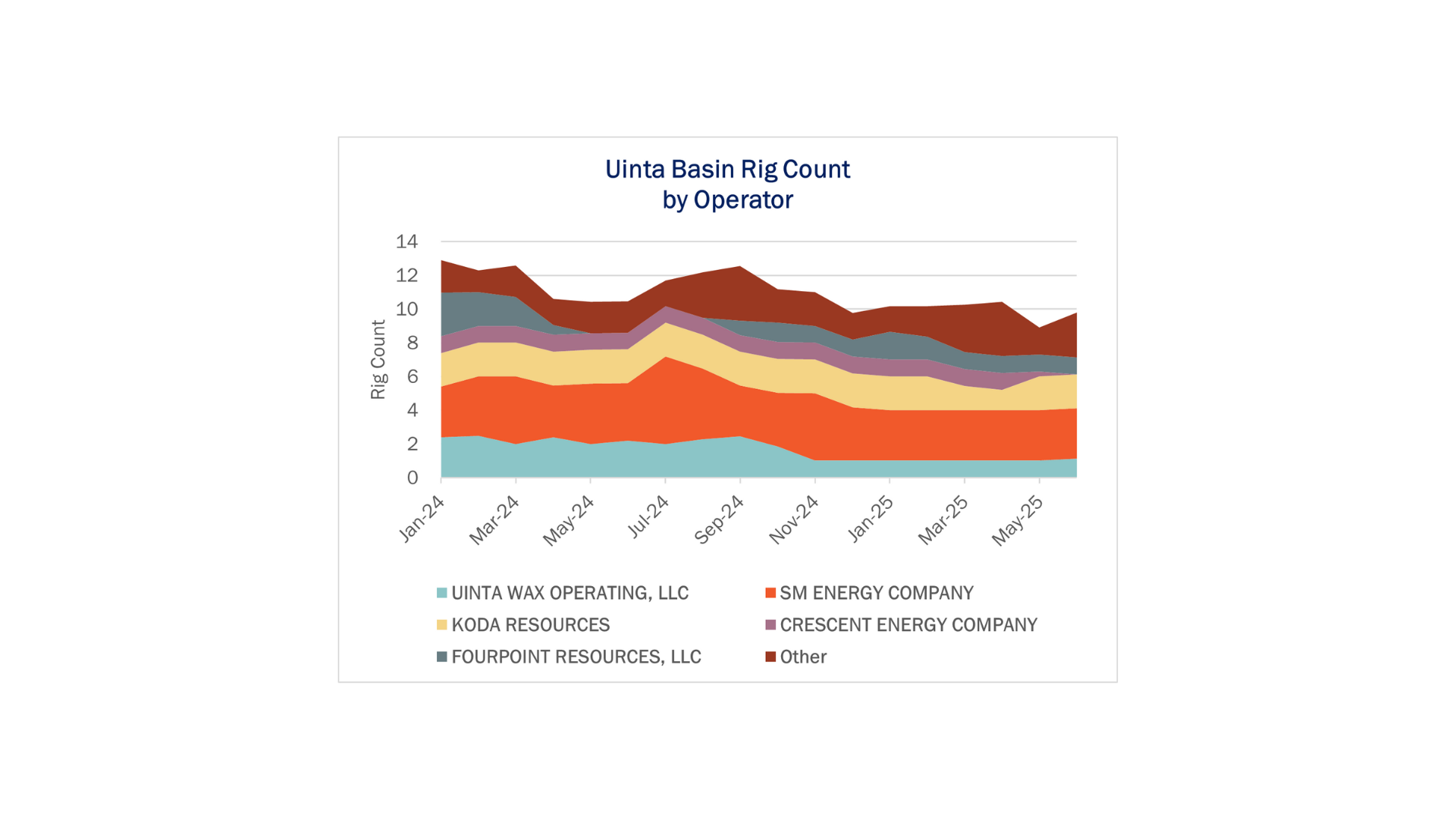

East Daley Analytics’ Uinta Basin Crude Oil S&D Report projects 2025 output to average ~184 Mb/d. The remote basin in northeastern Utah has longstanding takeaway constraints, limiting demand mostly to local refineries near Salt Lake City and some railing capacity.

With the Wildcat expansion enabling up to 80 Mb/d of new crude flow, Uinta operators can deploy more rigs. Using the Uinta Production Scenario Tool, East Daley estimates 2 additional rigs would add ~40 Mb/d of incremental production by 4Q28, bringing the average rig count to 11 from 9 currently in the basin.

Our review points to plenty of upside from the Wildcat expansion, though producers may be reluctant to commit capital now due to lower crude oil prices. Wildcat Midstream says it is still seeking commercial commitments to back the full expansion.

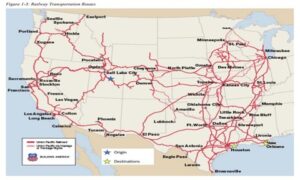

The incremental barrels are likely to be railed to Gulf Coast refineries and blending terminals in PADD 3. The Wildcat Terminal connects to the Union Pacific and Burlington Santa Fe rail systems, which carry the crude to refineries in Texas and Louisiana, according to the BLM application (see map).

The Wildcat expansion will compete with Savage’s proposed Wellington Transload Terminal, both serving as transload stations to move Uinta crude out of the basin. A third proposal to expand the Uinta Basin Railway (an in-basin short line) will allow more direct access to the national rail network. With much of the infrastructure already in place, the Wildcat Terminal can jump ahead of other greenfield projects to begin service.

Storage

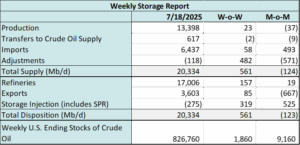

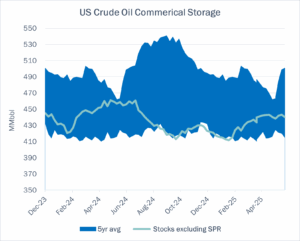

East Daley expects a 275 Mbbl withdrawal from commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending July 18. We expect total US stocks, including the SPR, will close at 826.8 MMbbl.

The US natural gas pipeline sample, a proxy for change in oil production, increased 0.75% W-o-W across all liquids-focused basins. Samples increased 1.95% in the Permian and 1.19% in the Rockies. The increases were partially offset by decreases of 1.95% in the Williston and 1.54% in the Eagle Ford. The Rockies and the Gulf of America have a high correlation between gas volumes and crude oil volumes, whereas the Permian and Eagle Ford basins correlation is less than 45%.

We expect US crude production to be 13.4 MMb/d. According to US bill of lading data, US crude imports increased to 6.4 MMb/d. More than 60% of the supply originated from Canadian pipelines and vessels into the US, with the remainder largely coming from vessels carrying crude from Mexico and Nigeria.

As of July 18, there was ~507 Mb/d of refining capacity offline, including downtime for planned and unplanned maintenance. EDA expects gross crude input into refineries to increase, coming in at 17 MMb/d.

Vessel traffic monitored by EDA along the Gulf Coast increased W-o-W. There were 21 vessels loaded for the week ending July 18 and 18 the prior week. EDA expects US exports to be 3.6 MMb/d.

The SPR awarded contracts for 6.0 MMbbl to be delivered to Choctaw February–May ‘25 and 2.4 MMbbl to be delivered to Bryan Mound April–May ‘25. The SPR has 403 MMbbl in storage as of July 18, 2025.

Regulatory and Tariffs:

Presented by ARBO

Tariffs:

Bridger Pipeline, LLC Rates were increased by the FERC index. Joint rates are less than or equal to the sum of the local rates. Effective July 1, 2025.

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at [email protected] or phone at 202-505-5296. https://www.goarbo.com/