Executive Summary:

Infrastructure: ARM Energy and PIMCO announced FID on the Mustang Express Pipeline to move Permian gas from Katy to the Louisiana border.

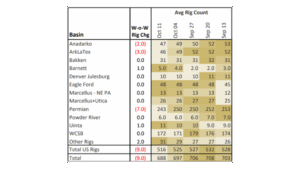

Rigs: The US lost 9 rigs for the week ending Oct. 11, bringing the total rig count to 516

Flows: US natural gas volumes averaged 68.8 Bcf/d in pipeline samples for the week ending Oct. 19, down 0.1% W-o-W.

Storage: Traders expect the EIA to report an 80 Bcf injection for the week ending Oct. 17.

Infrastructure:

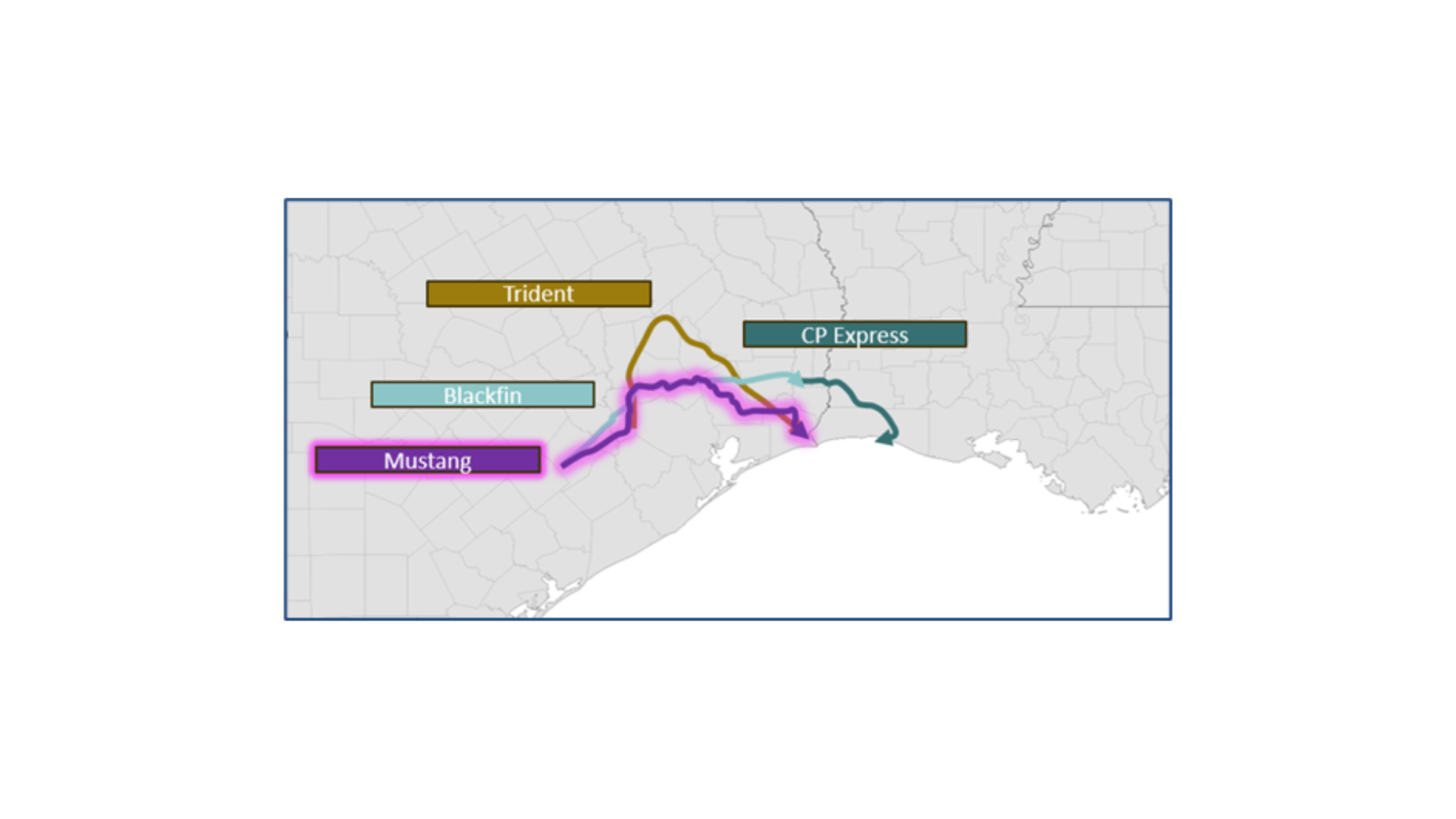

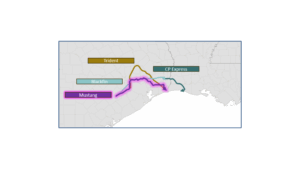

ARM Energy and PIMCO have taken a final investment decision (FID) on the 42-inch Mustang Express Pipeline. The $2.3B project is backed by an anchor shipper commitment from Sempra Energy’s (SRE) Port Arthur LNG Phase 2, which made FID in September.

Announced Oct. 9, Mustang Express will add 2.5 Bcf/d of new capacity from the Katy hub to Port Arthur and is expected to start service by late 2028. The project includes laterals between Katy and Tres Palacios and to the Golden Triangle storage facility near Port Arthur, providing optionality to access valuable storage on both ends of the pipeline. It also opens up a natural gas super-highway from the Waha hub through Katy to LNG demand on the Louisiana border, providing an outlet for volumes on the recently FID’d Eiger Express.

Less than 3 Bcf/d of pipeline capacity currently runs between Katy and the Gillis hub in Louisiana, limiting the amount of Texas gas supply that can reach the highest concentration of LNG demand growth. However, Mustang Express is the latest of several pipes in development to expand that corridor and build a seamless route from the Permian to Gillis-based LNG demand.

WhiteWater’s Blackfin Pipeline (3.5 Bcf/d) is nearing completion but needs the CP Express header (under construction) to properly connect to LNG demand at Venture Global’s (VG) CP2 LNG project. It’s not clear what other interconnects that line could have, so we forecast volumes to grow in line with CP2’s ramp schedule, starting in 2027. Kinder Morgan’s (KMI) Trident pipeline will add 2 Bcf/d by early 2027, supported by commitments from Golden Pass LNG. We expect these newbuild pipes will support prices at both the Katy and Waha hubs by reducing the risk of capacity constraints from wellhead to demand.

For a closer look at Gulf Coast supply and demand fundamentals, see East Daley’s Houston Ship Channel Supply & Demand report.

The Permian Basin at a Crossroads: Download the Latest White Paper

The Permian Basin is the heart of the US energy industry, supplying half of crude oil and NGL production and nearly 20% of natural gas. Yet market pressures are forcing changes, prompting billions in new pipeline investments and reorienting how operators approach the storied basin. East Daley’s new white paper, The Permian Basin at a Crossroads, is the first of a 3-part series looking at the shifts underway in the Permian. In this series, we reveal how LNG demand and AI data centers could transform Permian gas into a primary revenue driver. We also review the multi-billion-dollar infrastructure needed to unlock this shift, and what’s at stake for oil, gas and midstream operators. — Click here to download the The Permian Basin at a Crossroads white paper!

Rigs:

The US lost 9 rigs for the week ending Oct. 11, bringing the total rig count to 516. The Permian (-7), ArkLaTex (-3) and Anadarko (-2) lost rigs while the Barnett (+1) and Uinta (+1) gained rigs W-o-W.

At the company level, ET (-4), EPD (-3), WES (-2), ENLC (-1), XTO Energy (-1) and Aethon Energy (-1) lost rigs while TRGP (+1), PSX (+1), MPLX (+1), WMB (+1), KNTK (+1) and San Mateo Midstream (+1) gained rigs W-o-W.

See East Daley Analytics’ weekly Rig Activity Tracker for more information on rigs by basin and company.

Flows:

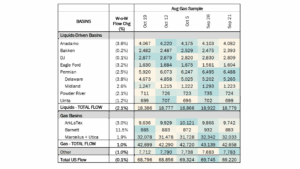

US natural gas volumes averaged 68.8 Bcf/d in pipeline samples for the week ending Oct. 19, approximately flat (-0.1%) W-o-W.

Major gas basin samples increased 1.0% W-o-W to 42.7 Bcf/d. The Haynesville sample declined 3.0% to 9.6 Bcf/d, while the Marcellus+Utica sample increased 1.9% to 32.1 Bcf/d.

Samples in liquids-focused basins declined 2.1% W-o-W to 18.4 Bcf/d. The Permian sample fell 2.5% to 5.9 Bcf/d, while the Anadarko sample decreased 3.6%.

Storage:

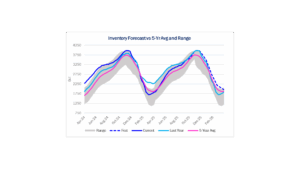

Traders and analysts expect the Energy Information Administration (EIA) to report a net injection of 80 Bcf for the week ending Oct. 17, a similar injection pace to the 80 Bcf injected for the week ending Oct. 10.

An 80 Bcf injection would increase the surplus to the five-year average by 3 Bcf to 160 Bcf. The storage surplus to last year would increase by 1 Bcf to 24 Bcf.

Including Thursday’s report, the next three weeks of injections should total 190 Bcf to close out the formal injection season at 3,910 Bcf. This would leave storage 21 Bcf below last year and at a 157 Bcf surplus to the five-year average of 3,753 Bcf. The November prompt month contract rallied on Tuesday to just below $3.50/MMBtu, the highest close since Oct. 8. The rally came as expectations for a higher end-of-season inventory were dashed by forecasts showing colder weather to close out the last week of October.

See East Daley Analytics latest Macro Supply & Demand Report for more analysis on storage and the winter market outlook.

Calendar:

Subscribe to East Daley’s The Daley Note (TDN) for midstream insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.