Executive Summary:

Infrastructure: The Mountain Valley and Transcontinental pipelines are fighting for new market in North Carolina.

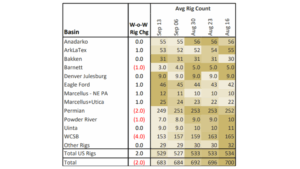

Rigs: The US gained 2 rigs for the week of Sept. 13, bringing the total rig count to 529.

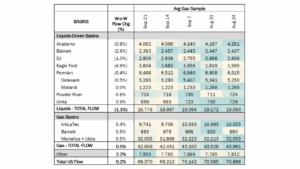

Flows: US natural gas volumes averaged 69.4 Bcf/d in pipeline samples for the week ending Sept. 21, up 0.2% W-o-W.

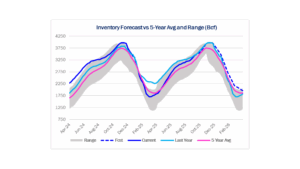

Storage: Traders expect the EIA to report a 77 Bcf injection for the week ending Sept. 19.

Infrastructure:

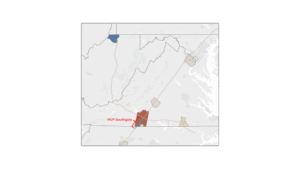

Mountain Valley Pipeline (MVP) and the Transcontinental Gas Pipe Line (Transco) are locked in a bruising fight for market in North Carolina, pitting MVP’s Southgate against Transco’s Southeast Supply Enhancement (SESE) project.

The Federal Energy Regulatory Commission (FERC) rang the starting bell in February when the agency asked Transco to provide documentation on the overlap between its SESE project and MVP’s Southgate. The pipeline, owned by Williams (WMB), provided FERC with maps detailing the nearly identical routes of Transco and Southgate (see pipeline map from East Daley Analytics’ Data Center Demand Monitor). Many places along the routes showed the two pipelines sharing easements and crossing paths.

MVP initially filed its amended Southgate application on Feb. 3, three days before FERC requested the route maps from Transco. MVP called out the SESE expansion in the application, stating that it “would not meet the purpose and need of the Amendment Project of diversifying the natural gas supply in the region or the requests of Mountain Valley and Transco to provide separate pipelines to each serve their customer requirements.” MVP further said that SESE “would not meet several of the Amendment Project objectives that Foundation Shippers considered prior to contracting for capacity,” such as resiliency, operational flexibility and risk diversification.

Transco punched back in mid-March, filing a motion to intervene on the Southgate project. In the motion, Transco called MVP’s statements “a mischaracterization” of its SESE project that “attempts to support Southgate at the expense of facts.” Now the second round had begun.

The following month, FERC issued an environmental information request (EIR) from Transco seeking details about the Southgate/SESE overlap and how both companies were evaluating alternatives together for segments of the projects that might need line adjustments.

Transco’s strongest punch came on May 7 in its filed response. Transco said SESE could be modified to incorporate the volumes from Southgate into its own project, an outcome that would allow Transco to maintain its near-monopoly on gas service in North Carolina. Adding insult to injury, Transco on June 20 included its EIR responses in a comment on the Southgate docket. Five days later, FERC requested MVP Southgate file an EIR that included a response to Transco’s comment.

Round three began on June 26, when FERC requested that Transco explain how SESE could be modified to accommodate Southgate. Transco filed its explanation on July 7. MVP then hit back, turning to its foundation shippers, Duke Utilities and the Public Service Company of North Carolina (PSNC), for support of the Southgate expansion. In comments, the two utilities reiterated the value of supply diversity and directly attacked Transco. PSNC stated that there has been a “rapid rise of daily Operational Flow Orders (‘OFOs’) … that often significantly limit PSNC’s service options in both directions on the pipeline. In fact, for the last several years, it has become common practice to see Transco issue OFOs covering more than 200 days each year.” PSNC also detailed emergency actions and delivery pressure concerns related to Transco. While Duke’s comments weren’t as critical of Transco, they still highlighted the increased fuel security of a second supply source.

FERC continues to actively review both projects. It’s unclear how the agency will rule on this case, or if more rounds await the two parties. FERC’s current schedule for the Southgate project expects the Environmental Assessment to be issued in October, with the final authorization decision occurring before Jan. 1, 2026.

Rigs:

The US gained 2 rigs for the week of Sept. 13, bringing the total rig count to 529. The Permian (-2), Barnett (-1) and Powder River (-1) lost rigs while the ArkLaTex (+1), Eagle Ford (+1), Marcellus – NE PA (+1) and Marcellus+Utica (+1) gained rigs W-o-W.

At the company level, ET (-4), SMC (-2) and San Mateo Midstream (-2) lost rigs and EPD (+3), TRGP (+2), PSX (+1), MPLX (+1), OKE (+1), ENLC (+1), KMI (+1) and KNTK (+1) gained rigs W-o-W.

See East Daley Analytics’ weekly Rig Activity Tracker for more information on rigs by basin and company.

Flows:

US natural gas volumes averaged 69.4 Bcf/d in pipeline samples for the week ending Sept. 21, up 0.2% W-o-W.

Major gas basin samples increased 0.5% W-o-W to 42.7 Bcf/d. The Haynesville sample increased 0.4% to 9.7 Bcf/d, and the Marcellus+Utica sample rose 0.5% to 32.0 Bcf/d.

Samples in liquids-focused basins declined 1.1% W-o-W to 18.8 Bcf/d. The Eagle Ford sample fell 4.6% to 1.6 Bcf/d, while the Bakken sample decreased 2.6%.

Storage:

Traders and analysts expect the Energy Information Administration (EIA) to report a net injection of 77 Bcf for the week ending Sept. 19. An injection of 77 Bcf would increase the surplus to the five-year average by just 1 Bcf to 205 Bcf. The storage deficit to 2024 would flip to a surplus of 24 Bcf – the first time storage would be in a surplus to the prior year since late January ‘25.

East Daley’s updated end-of-season inventory forecast stands at 3.912 Tcf in this month’s Macro Supply & Demand Report. Our latest outlook assumes 10-year normal weather for the next six weeks and no hurricane disruptions. An early view on winter is also included in the latest Macro Report. Generally speaking, we expect storage withdrawals to trail last year as growth in LNG feedgas demand is counterbalanced by a production ramp over the next several months. Our longer term storage outlook is highlighted in the graph below.

See the latest Macro Supply & Demand Report for more analysis on the storage outlook.

Calendar:

Subscribe to East Daley’s The Daley Note (TDN) for midstream insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.