Executive Summary:

Infrastructure: Sempra Energy is moving forward with Port Arthur Phase 2, capping a strong summer for LNG project financing.

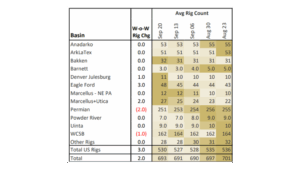

Rigs: The US gained 3 rigs for the week of Sept. 20, bringing the total rig count to 530.

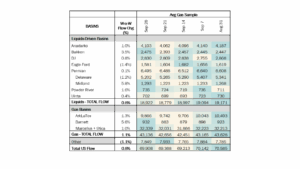

Flows: US natural gas volumes averaged 69.9 Bcf/d in pipeline samples for the week ending Sept. 28, up 0.8% W-o-W.

Storage: Traders expect the EIA to report a 65 Bcf injection for the week ending Sept. 26.

Infrastructure:

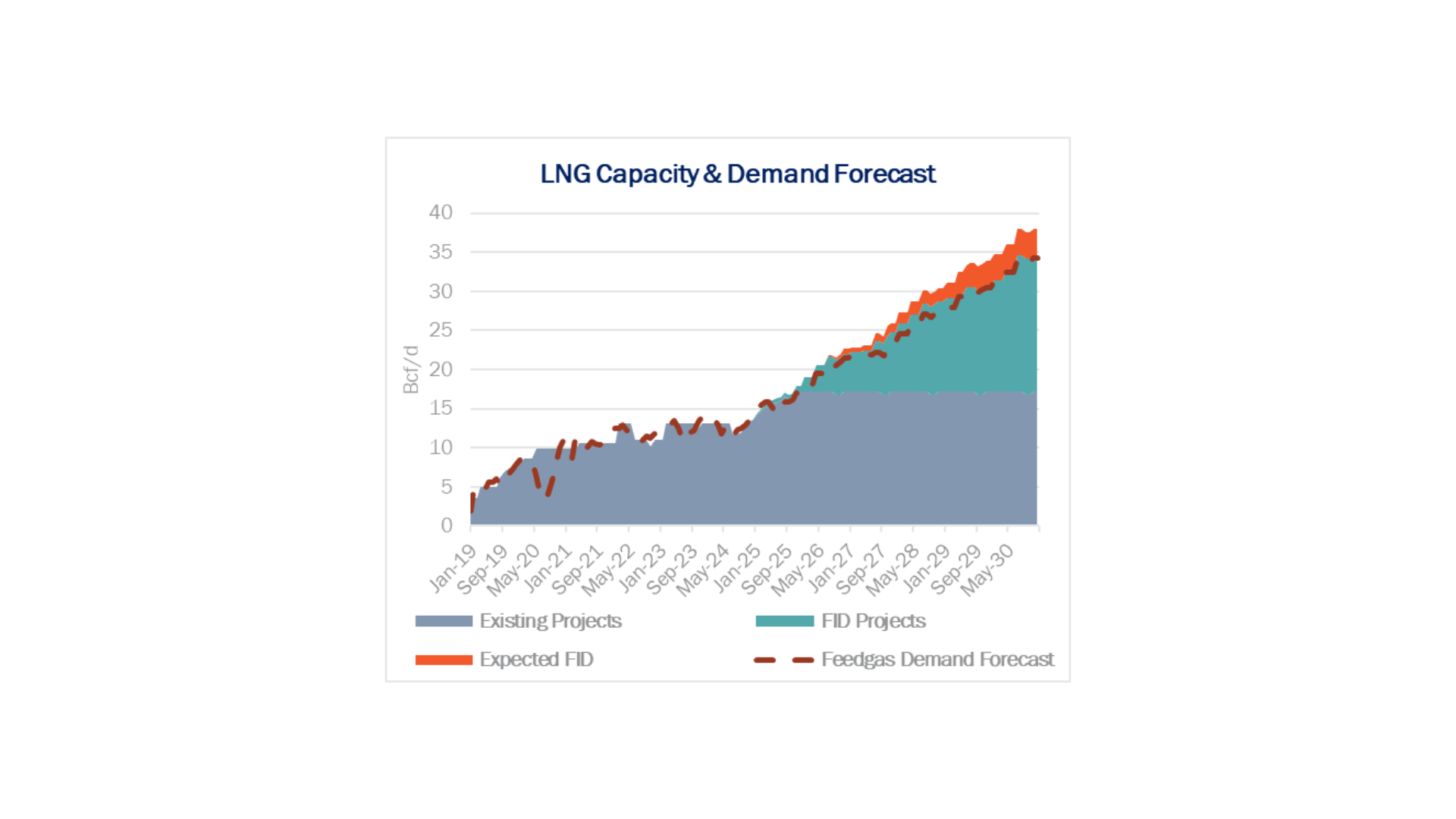

It’s been a strong summer for LNG project financing, with over 7.5 Bcf/d of projects reaching a final investment decision (FID) since the end of April. The latest is Sempra Energy’s (SRE) Port Arthur Phase 2, continuing a strong outlook for natural gas demand growth.

Last Tuesday (Sept. 23), Sempra announced FID on Port Arthur Phase 2 to build two additional liquefaction trains (13 Mtpa), doubling the capacity of Port Arthur LNG to just under 4 Bcf/d. Trains 1 and 2 are expected to begin service in 2027 and 2028, and Trains 3 and 4 are expected to reach commercial operations in 2030 and 2031.

Phase 2 carries an estimated price tag of $12B, SRE said, plus an additional $2B of Capex for “shared common facilities” to upgrade infrastructure at the Port Arthur facility. Funding for Phase 2 is supported by equity from a consortium of investors, including Blackstone Credit, KKR, Apollo, and Goldman Sachs Credit. The investor group together acquired a 49.9% minority stake in Phase 2 for $7B.

Rio Grande LNG also made FID on Rio Grande LNG Train 4 earlier this month, adding another 6 Mtpa. The Train 4 decision brings total FID’d capacity at the facility to 24 Mtpa, or over 3 Bcf/d of feedgas demand by 2030. TotalEnergies holds a 17.1% stake in NextDecade (NEXT) and took an additional 10% stake in the JV to develop Train 4, along with partners Global Infrastructure Partners, GIC, and Mubadala. Venture Global (VG) made FID on Phase 1 of the CP2 LNG project at the end of July.

Historically, LNG facilities have reached FID once roughly 80% of the liquefaction capacity is contracted to counterparties. Increasingly this is no longer the case, as more outside investors are taking equity stakes in projects. Sempra took FID on Port Arthur Phase 2 with just 56% of the capacity under contract, but expects to enter into additional offtake agreements. Woodside Energy’s (WDS) Louisiana LNG made FID at just 8% of contracted capacity after Stonepeak acquired a 40% stake in the project.

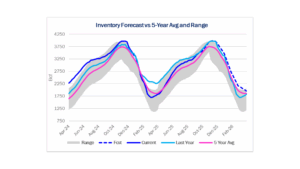

In total, East Daley forecasts 20.8 Bcf/d of incremental LNG feedgas capacity will be online by the end of the decade, on top of the 17.2 Bcf/d of current capacity. Our current estimate in the Macro Supply & Demand Report for total LNG feedgas demand is 34.2 Bcf/d by YE30, assuming 90% average utilization across all facilities (see figure above).

Most of these facilities, including Sempra’s Port Arthur LNG, will be sourcing volumes from the Gillis hub in Louisiana. Gillis will have plenty of capacity in the short term as new lines like Williams’ (WMB) Louisiana Energy Gateway and Momentum’s NG3 rapidly fill to close out 2025, but will likely need additional capacity to reach FID in 2030 and beyond. For a closer look at the Gillis supply and demand outlook, see our Southeast Gulf S&D Report.

Rigs:

The US gained 3 rigs for the week of Sept. 20, bringing the total rig count to 530. The Permian (-2) lost rigs while the Eagle Ford (+3), Marcellus+Utica (+2) and Denver-Julesburg (+1) gained rigs W-o-W.

At the company level, TRGP (-3), PSX (-1), OKE (-1) and Brazos Midstream (-1) lost rigs while ET (+4), ENLC (+3), EPD (+2) and WMB (+1) gained rigs W-o-W.

See East Daley Analytics’ weekly Rig Activity Tracker for more information on rigs by basin and company.

Flows:

US natural gas volumes averaged 69.9 Bcf/d in pipeline samples for the week ending Sept. 28, up 0.8% W-o-W.

Major gas basin samples increased 1.1% W-o-W to 43.1 Bcf/d. The Haynesville sample increased 1.3% to 9.9 Bcf/d, and the Marcellus+Utica sample rose 1.0% to 32.3 Bcf/d.

Samples in liquids-focused basins gained 0.8% W-o-W to 18.9 Bcf/d. The Eagle Ford sample fell 4.6% to 1.6 Bcf/d, while the Bakken sample decreased 2.6%.

Storage:

Traders and analysts expect the Energy Information Administration (EIA) to report a net injection of 65 Bcf for the week ending Sept. 26. A 65 Bcf injection would decrease the surplus to the five-year average by 20 Bcf to 283 Bcf. This would mark the first time in four weeks that the surplus would drop. The storage surplus to last year would increase by 11 Bcf to 33 Bcf.

With five weeks left in the official injection season, inventory levels are on track to pass 3,900 Bcf. Should injections match the 5-year average for the next five weeks, stocks would reach 3,936 Bcf by the end of October, or just 5 Bcf above last year’s levels.

Depending on weather, storage injections sometimes extend beyond the end of October; last year injections continued into the first week of November, and working gas peaked at 3,972 Bcf. November 2024 was a net injection month as well. In East Daley’s new monthly Macro Supply & Demand Report, we anticipate November 2025 will be a net injection month like last year. We believe production is strong enough to extend the injection season again, perhaps into the second week of November. We assume 10-year normal weather in our forecast.

See the latest Macro Supply & Demand Report for more analysis on storage and the winter market outlook.

Calendar:

Subscribe to East Daley’s The Daley Note (TDN) for midstream insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.