Executive Summary:

Infrastructure: East Daley estimates that at least 17 Bcf/d of gas production was lost at the peak of Winter Storm Fern, setting up a potentially record storage withdrawal in Thursday’s EIA report.

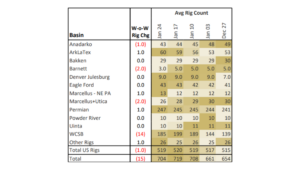

Rigs: The US rig count declined by 1 for the week of Jan. 24, bringing the total count to 519.

Flows: US natural gas volumes in pipeline samples averaged 65.8 Bcf/d for the week ending Feb. 1, down 4.3% W-o-W.

Storage: Traders and analysts expect the EIA to report a 370 Bcf storage withdrawal for the week ending Jan. 30, what would be a record high.

Infrastructure:

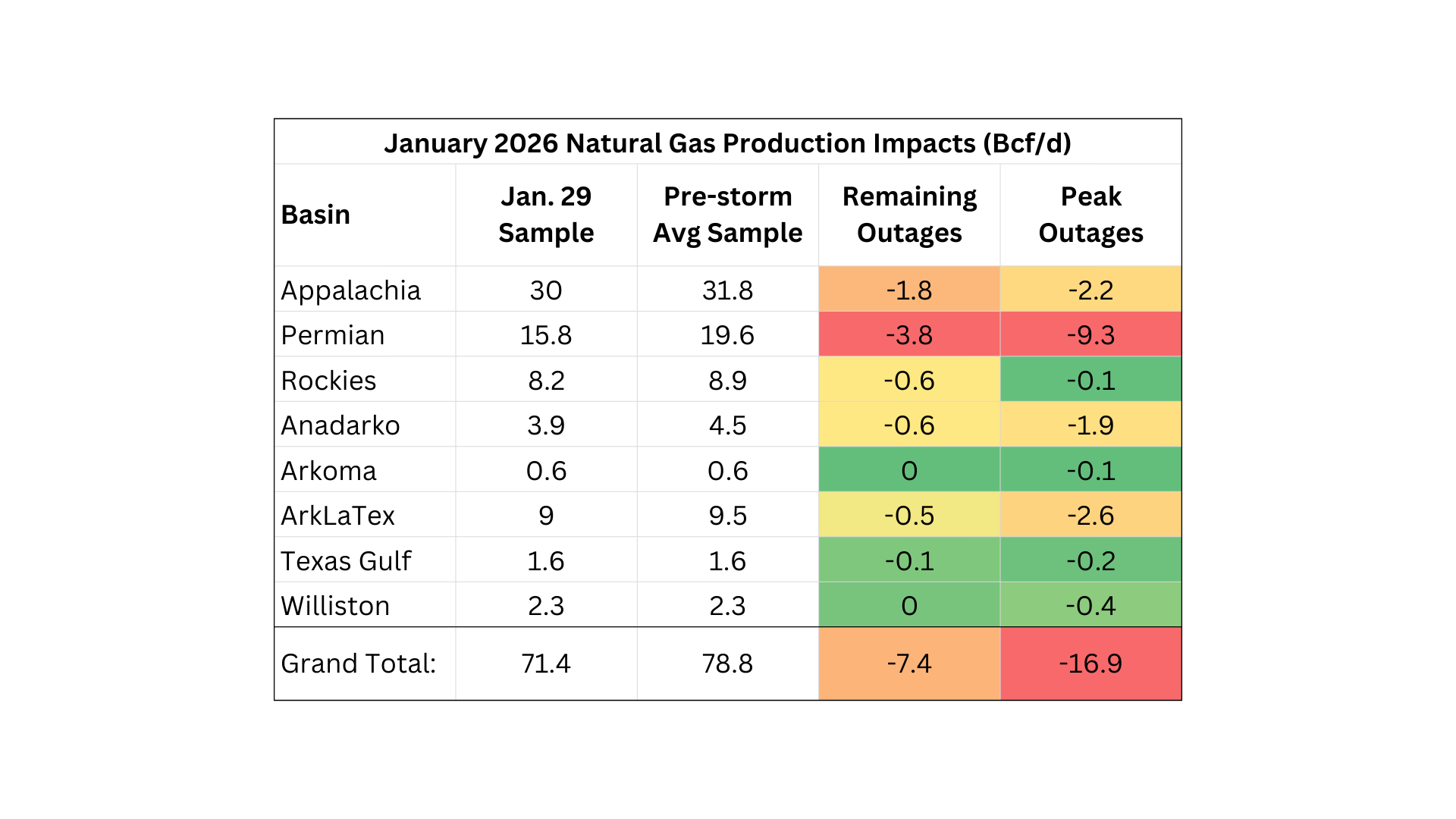

East Daley Analytics estimates that at least 17 Bcf/d of gas production was lost at the peak of last week’s powerful winter blast. Outages lingered through the end of the week from the weather event, named Winter Storm Fern by meteorologists.

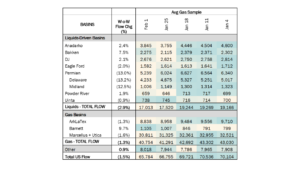

Pipeline samples show that 7.4 Bcf/d of natural gas remained offline as of last Thursday (Jan. 29) due to Fern (see table) as frigid temperatures lingered in major markets. These represent conservative estimates since our samples don’t fully capture Lower 48 gas production.

At least 16.9 Bcf/d was curtailed at the peak of the winter storm last Monday and Tuesday (Jan. 25-26), mostly in the Permian Basin, Appalachia, Anadarko and ArkLaTex (Haynesville).

Haynesville production had mostly recovered by the end of the week, as power outages were likely causing most of the outages vs wellhead freeze-offs. However, 5.6 Bcf/d remained offline between the Permian and Appalachia Thursday.

Fern brought sub-zero temperatures to the Midwest, record snowfall in the Northeast, plus ice storms and power outages across the Midcontinent and Southeast. Natural gas prices briefly spiked on the weather. Henry Hub spot prices jumped past $30/MMBtu, and deals were reported over $50 at citygates in the Northeast Jan. 26-27, reflecting the market squeeze from lost production and strong heating demand.

Freeze-offs impact hydrocarbon production when extreme cold envelops multiple points in the delivery system. Wellheads can clog as water and heavier NGLs freeze, and gathering and processing systems can lose access to power.

The lost supply will contribute to a potentially record storage withdrawal in Thursday’s storage report from the Energy Information Administration (see storage coverage below). Market estimates predict a 370 Bcf gas withdrawal for the week ending Jan. 30.

While a hit to Permian output, the impacts of Fern were likely softened thanks to new state regulations. Following Winter Storm Uri in Feb ‘21, Texas implemented regulations requiring operators to winterize systems and equipment to avoid more drastic supply losses. For perspective, East Daley estimates gas supply decreased 7% M-o-M in the Permian in January 2026. During Uri, Permian supply decreased by 15% M-o-M in Feb ‘21. The reduced impact during this storm may point toward more resilient production equipment deployed during the past five years.

Rigs:

The US rig count declined by 1 for the week of Jan. 24, bringing the total rig count to 519. The Marcellus+Utica (-2), Barnett (-2) and Anadarko (-1) lost rigs while the ArkLaTex (+1), Marcellus–NE PA (+1) and Permian (+1) gained rigs W-o-W.

At the company level, Energy Transfer (-3), EnLink (-2), Targa Resources (-1), Phillips 66 (-1), Kinder Morgan (-1), DT Midstream (-1), Producers Midstream (-1) and San Mateo (-1) lost rigs while Enterprise (+2), MPLX (+2), Kinetik (+2) and Western Midstream (+1) gained rigs W-o-W.

See East Daley Analytics’ weekly Rig Activity Tracker for more information on rigs by basin and company.

Flows:

US natural gas volumes in pipeline samples averaged 65.8 Bcf/d for the week ending Feb. 1, down 1.5% W-o-W.

Flows in major basins reflected continued impairments from Winter Storm Fran. The Haynesville sample declined 1.3% W-o-W to 8.8 Bcf/d, while the Marcellus+Utica slid 1.6% to 30.8 Bcf/d.

Samples in liquids-focused basins declined 2.9% to 17.0 Bcf/d, led by a sharp 13% drop in the Permian sample. However, the Anadarko and Bakken samples rose as operations began to recover from the winter storm.

Storage:

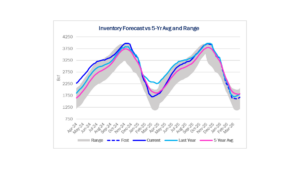

Traders and analysts expect the Energy Information Administration (EIA) to report a 370 Bcf storage withdrawal for the week ending Jan. 30. A 370 Bcf draw would flip the current surplus to the 5-year average to a 37 Bcf deficit. The surplus to last year would also be whittled down to just 31 Bcf.

A 370 Bcf storage withdrawal would be an all-time weekly record and would result in the highest monthly withdrawal since January 2018. We saw a brief period of deficits in mid-December 2025, but warm weather managed to wipe that out through the first two weeks of January.

Prices ran up last week as the mild temperatures flipped to extreme cold, with the prompt-month Henry Hub contract hitting $7.46/MMBtu last Wednesday (Jan. 28). However, weather forecasts flipped over the weekend for February, and the market sold off once again. The March prompt month fell 26% ($1.12) on Monday.

Prices ran up last week as the mild temperatures flipped to extreme cold, with the prompt-month Henry Hub contract hitting $7.46/MMBtu last Wednesday (Jan. 28). However, weather forecasts flipped over the weekend for February, and the market sold off once again. The March prompt month fell 26% ($1.12) on Monday.

The current 10- to 15-day forecast pushes total February gas-weighted heating degree days (GWHDDs) below the 10-year normal level (warmer), whereas on Jan. 24, weather models had GWHDDs well above the 10-year and 30-year levels. According to X Weather (Maxar) data, the forecast for February GWHDDs fell by 190, or 23% from last week to this week.

In East Daley’s latest Macro Supply & Demand Report, we maintain that the storage inventories will remain below the five-year average through the end of March, an up-and-down winter notwithstanding.

Subscribe to East Daley’s The Daley Note (TDN) for midstream insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.