Executive Summary:

Infrastructure: A powerful Arctic storm that swept through the US has put the brakes on natural gas production and lit a spark under prices this week.

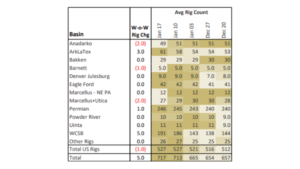

Rigs: The US rig count was flat for the week of Jan. 17 at 527 rigs.

Flows: US natural gas volumes in pipeline samples averaged 66.0 Bcf/d for the week ending Jan. 25, down 4.3% W-o-W.

Storage: Traders and analysts expect the EIA to report a 230 Bcf storage withdrawal for the week ending Jan. 23.

Infrastructure:

A powerful Arctic storm that swept through the US has put the brakes on natural gas production and lit a spark under prices.

Heny Hub spot prices surged past $30/MMBtu on Monday (Jan. 26) as the Arctic front brought snow, sleet and frigid temperatures across a wide swath of the Lower 48, stretching from the Southwest across the East Coast. The front-month Henry Hub Feb ’26 contract has also rallied, doubling over the past week to trade at $7.20 late Wednesday afternoon (Jan. 28)

Pipeline samples show US gas production dropped over 9 Bcf/d over the weekend and early this week as the Arctic blast disrupted operations in the field. The front brought sub-zero temperatures to the Midwest, record snowfall in parts of the Northeast, plus ice storms and power outages across the Midcontinent and Southeast. Meteorologists predict the Lower 48 east of Chicago, including the nation’s largest population centers, will be cold for the balance of the month, and that this could be one of the coldest stretches of the past 30 years.

The Arctic blast has fired up bullish spirits in natural gas. Spot prices in Appalachia jumped past $30/MMBtu, and deals were reported over $50 at citygates in the Northeast, reflecting the market squeeze from lost production and strong heating demand.

East Daley’s review of pipeline samples show the largest production losses on Monday and Tuesday (Jan. 26-27) of 9-10 Bcf/d. Samples were down over 2 Bcf/d in the Permian Basin, where temperatures fell into single digits over the weekend, with similar declines in Appalachia and the Haynesville. Our pipeline samples do not fully capture US gas production, so actual supply losses were likely larger from the storm.

Freeze-offs impact supply when extreme cold envelops multiple points in energy delivery systems. Wellheads and pipes can clog as water and heavier NGLs freeze in the wellbore. Gathering systems can lose pressure or access to power during extreme weather, and gas processing plants can be forced to curtail or operate below capacity.

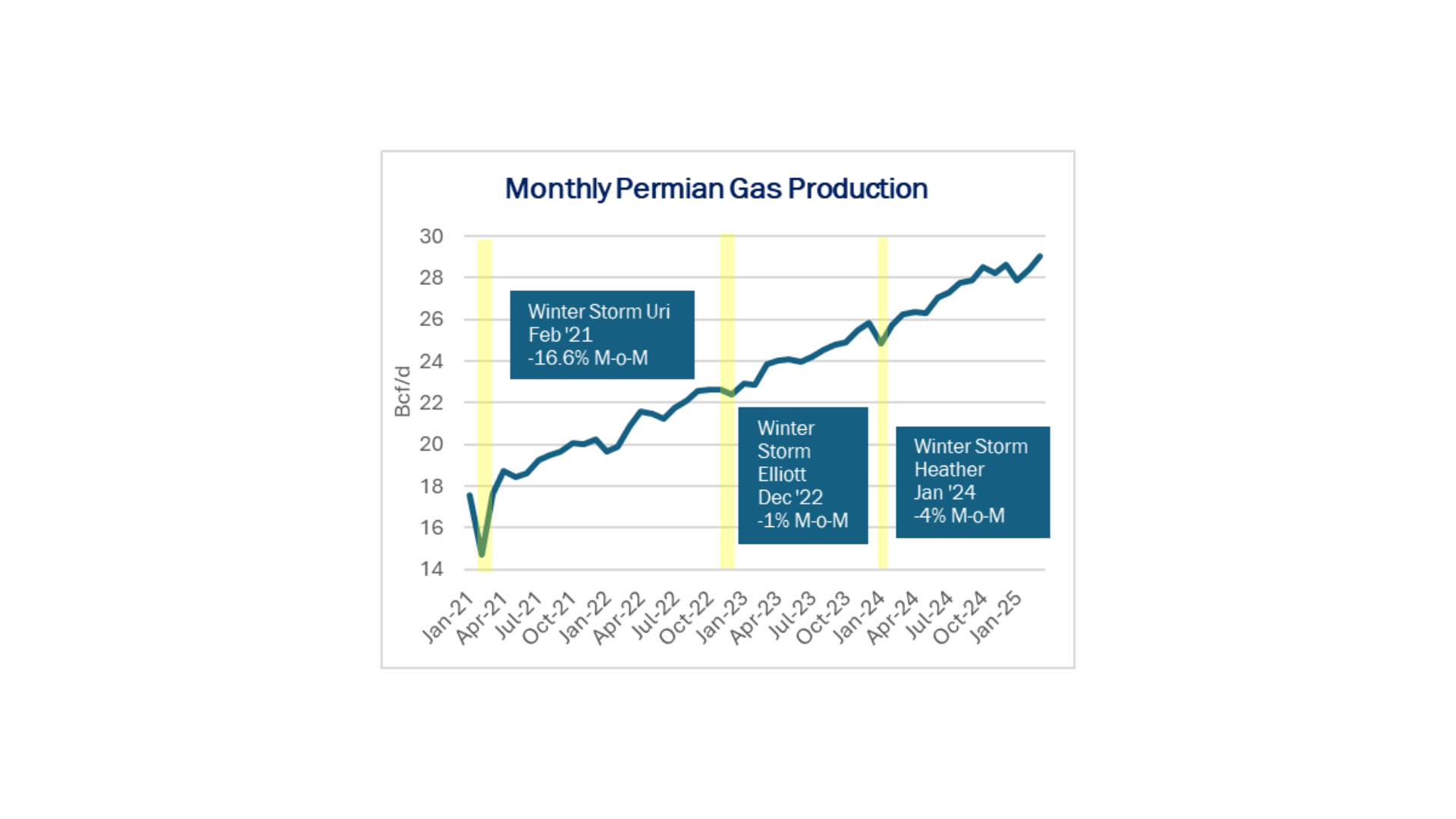

Recent extreme winter events show this pattern clearly. In February 2021, Permian natural gas production fell 16.6% M-o-M as a result of Winter Storm Uri (see figure). Delivery also took a hit during Winter Storm Elliot in Dec ’22 and Winter Storm Heather in Jan ’24.

Not all of the impacts from the storm are bullish for prices. Several industrial consumers on the Gulf Coast reportedly shut down as the front moved through Texas and Louisiana, including refiners and petrochemical plants. LNG exports also have been curtailed at Gulf Coast facilities.

As a result of the cold blast, all eyes in gas markets will be on the next two Energy Information Administration (EIA) gas storage surveys for the weeks ending Jan. 23 and Jan. 30, when a combined 570 Bcf of gas could be withdrawn (see storage coverage below). The frigid weather is likely to whipsaw the market back into deficit territory before the end of the month, setting up a much tighter market for the balance of winter.

Rigs:

The US rig count was flat for week of Jan. 17 at 527. The Anadarko (-2), Marcellus+Utica (-2) and Barnett (-1) lost rigs W-o-W while the Haynesville (+3) and Permian (+1) gained rigs.

See East Daley Analytics’ weekly Rig Activity Tracker for more information on rigs by basin and company.

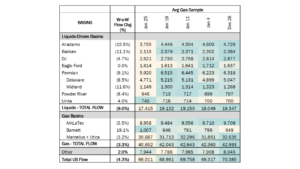

Flows:

US natural gas volumes in pipeline samples averaged 66.0 Bcf/d for the week ending Jan. 25, down 4.3% W-o-W.

Flows in major basins reflected the start of shut-ins over the weekend from extreme weather. The Haynesville sample declined 5.5% W-o-W to 9.0 Bcf/d, while the Marcellus+Utica fell 3.2% to 30.7 Bcf/d. Conversely, the Barnett sample jumped 19.0% to 1 Bcf/d.

Samples in liquids-focused basins declined 9.0% to 17.4 Bcf/d. The Anadarko sample fell 15.5% to 3.8 Bcf/d, and the Permian sample was down 9.1% W-o-W.

Storage:

Traders and analysts expect the Energy Information Administration (EIA) to report a 230 Bcf storage withdrawal for the week ending Jan. 23. A 230 Bcf draw would narrow the surplus to the 5-year average to 155 Bcf from 177 Bcf last week. The surplus to last year would increase from 141 Bcf last week to 218 Bcf.

Last year saw a massive 321 Bcf withdrawal for the third week of January, thus the reason why the smaller withdrawal expected this week will dramatically expand the surplus to last year. However, the storage withdrawal for the week ending Jan. 29 (EIA release on Feb. 5) is expected to be massive, so big that it will likely wipe out the current surplus to the five-year average and erase most of the surplus to last year.

The reaction to cold weather this week has been a “buy the rumor” event, based on how large the storage pull is reported in EIA’s survey next week. With production dropping due to freeze-offs and electric, residential and commercial demand remaining stout due to frigid conditions across the US, the Lower 48 has leaned heavily on storage gas. Early estimates for the withdrawal could be well above the 359 Bcf record withdrawal reported for the first week of January 2018. There are only four weekly EIA surveys where the Lower 48 withdrew more than 300 Bcf, and some analysts speculate this pull could come closer to 400 Bcf.

See East Daley’s latest Macro Supply & Demand Report for more analysis on the winter market outlook.

Subscribe to East Daley’s The Daley Note (TDN) for midstream insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.