Executive Summary:

Infrastructure: Wisconsin is becoming a growth market for natural gas, thanks to a booming data center industry.

Rigs: The US gained 1 rig for the week of Nov. 22, bringing the total rig count to 515.

Flows: US natural gas volumes in pipeline samples averaged 70.7 Bcf/d for the week ending Nov. 30, up 1.8% W-o-W.

Storage: Traders expect the EIA to report an 18 Bcf withdrawal for the week ending Nov. 28.

Infrastructure:

Wisconsin is emerging as a hot growth market for natural gas, backed by a burgeoning data center industry. Two major pipeline projects are set to reshape Midwest gas flows to supply increasing demand in the Upper Midwest.

TC Energy’s (TRP) Wisconsin Reliability Project (WRP) on ANR Pipeline and DT Midstream’s (DTM) Guardian 3 expansion of Guardian Pipeline together will add ~680 MMcf/d of deliverability between the Chicago hub and Wisconsin.

WRP expands the ANR mainline by 144 MMcf/d through a combination of pipeline replacement and facility upgrades. The project replaces 51 miles of pipe with larger steel and installs hybrid electric/gas compressors at the Kewaskum and Weyauwega compressor stations to boost reliability and flexibility. TC Energy started construction in late 2024 and placed the $700MM expansion in service on Nov. 1. The project is backed by 10-year contracts with several utilities and local distribution companies, including North Shore Gas, Wisconsin Electric Power, Wisconsin Public Service Corp., and Wisconsin Power and Light.

DT Midstream also recently upsized its Guardian 3 expansion after receiving strong interest in an open season. DTM awarded around 328 MMcf/d to five shippers following a binding open season in September. Including previous commitments made in July, the total planned expansion reaches ~540 MMcf/d, or a 40% increase of Guardian’s current capacity. The 260-mile Guardian Pipeline already serves major load centers from the Chicago hub into Wisconsin.

The Upper Midwest is a growing focus of data center developers. In the Data Center Demand Tracker, East Daley Analytics is monitoring about 16 GW of announced data center projects across Wisconsin and Illinois from prominent technology companies like Microsoft (MSFT) and Meta (META). These projects, if fully realized, could create up to 1 Bcf/d of additional gas demand. Among the largest data center developments are Microsoft’s Mount Pleasant facility in Wisconsin, with a total load of ~2.7 GW, and Project Cardinal in Illinois at around 2.4 GW.

See East Daley’s Data Center Demand Tracker, part of the Macro Supply & Demand Report package, for more on the natural gas market outlook. Along with data centers, natural gas demand is increasing in the Midwest from coal plant retirements, renewable integration and growing industrial load. Wisconsin has historically relied on coal-fired generation, and gas is seeing new opportunities as older plants are shut down. The ANR and Guardian expansions align pipeline infrastructure with this emerging load.

The Permian Basin at a Crossroads: Download Why This Pipeline Boom is Different

The Permian’s next big buildout is already taking shape — but this time, the drivers aren’t producers chasing oil. East Daley’s latest white paper reveals how gas demand from AI data centers, LNG exports, and utilities is rewriting the midstream playbook. Over 9 Bcf/d of new capacity and $12 billion in investments are reshaping flows, turning the Permian into a gas powerhouse even as rigs decline. Read Part II: Why This Pipeline Boom is Different

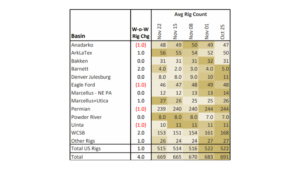

Rigs:

The US gained 1 rig for the week of Nov. 22, bringing the total rig count to 515. The Permian (-1), Anadarko (-1), Eagle Ford (-1) and Uinta (-1) lost rigs while the Barnett (+2), ArkLaTex (+1) and Marcellus+Utica (+1) gained rigs W-o-W.

At the company level, Kinder Morgan (-3), Energy Transfer (-1), ONEOK (-1), Western Midstream (-1), Salt Creek Midstream (-1) and Tallgrass (-1) lost rigs while MPLX (+2), Williams (+2), Targa Resources (+1), M6 Midstream (+1), Hess Corp. (+1) and Brazos Midstream (+1) gained rigs W-o-W.

See East Daley Analytics’ weekly Rig Activity Tracker for more information on rigs by basin and company.

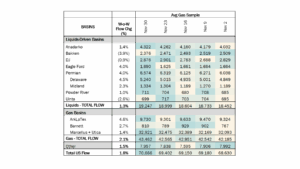

Flows:

US natural gas volumes in pipeline samples averaged 70.7 Bcf/d for the week ending Nov. 30, up 1.8% W-o-W.

Major gas basin gained 2.1% W-o-W to average 43.5 Bcf/d. The Haynesville sample increased 4.6% to 9.7 Bcf/d, while the Marcellus+Utica sample rose 1.4% to 32.9 Bcf/d.

Samples in liquids-focused basins increased 1.3% to 19.2 Bcf/d. The Permian sample gained 4.0% to 6.6 Bcf/d, while the Eagle Ford sample also rose 4.0% W-o-W.

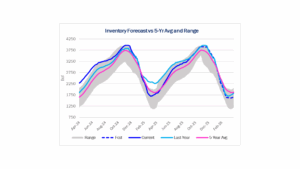

Storage:

Traders and analysts expect the Energy Information Administration (EIA) to report an 18 Bcf net withdrawal for the week ending Nov. 28. An 18 Bcf withdrawal would increase the surplus to the five-year average by 25 Bcf to 185 Bcf. The storage comparison to last year would move to a 24 Bcf deficit.

Last week was cold across the country as a polar vortex began to spread from the Upper Midwest through the Northeast and Southeast midweek. The impact to demand was only slightly muted by the Thanksgiving holiday. This current week will remain cold across the country and will not have the benefit of a two-day holiday. Peak cold will hit Thursday and Friday (Dec. 4-5) with Lower 48 average temperatures about 10 degrees cooler than the 10-year average.

The cold weather pattern will extend through the first two weeks of December, and the market should see its first set of triple-digit withdrawals. Last year had similar weather, resulting in net withdrawals of 190 Bcf and 125 Bcf for the weeks ending Dec. 6 and 13, respectively. The January prompt-month contract has moved up about $0.30 to $4.88/MMBtu while Henry Hub cash is edging above $4.60, the highest prices since the second week of March 2025.

See East Daley Analytics’ latest Macro Supply & Demand Report for more analysis on the winter market outlook.

Subscribe to East Daley’s The Daley Note (TDN) for midstream insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.