Executive Summary:

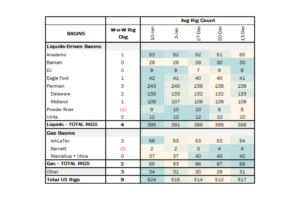

Rigs: The total US rig count increased by 9 during the week of Jan. 10 from 515 to 524.

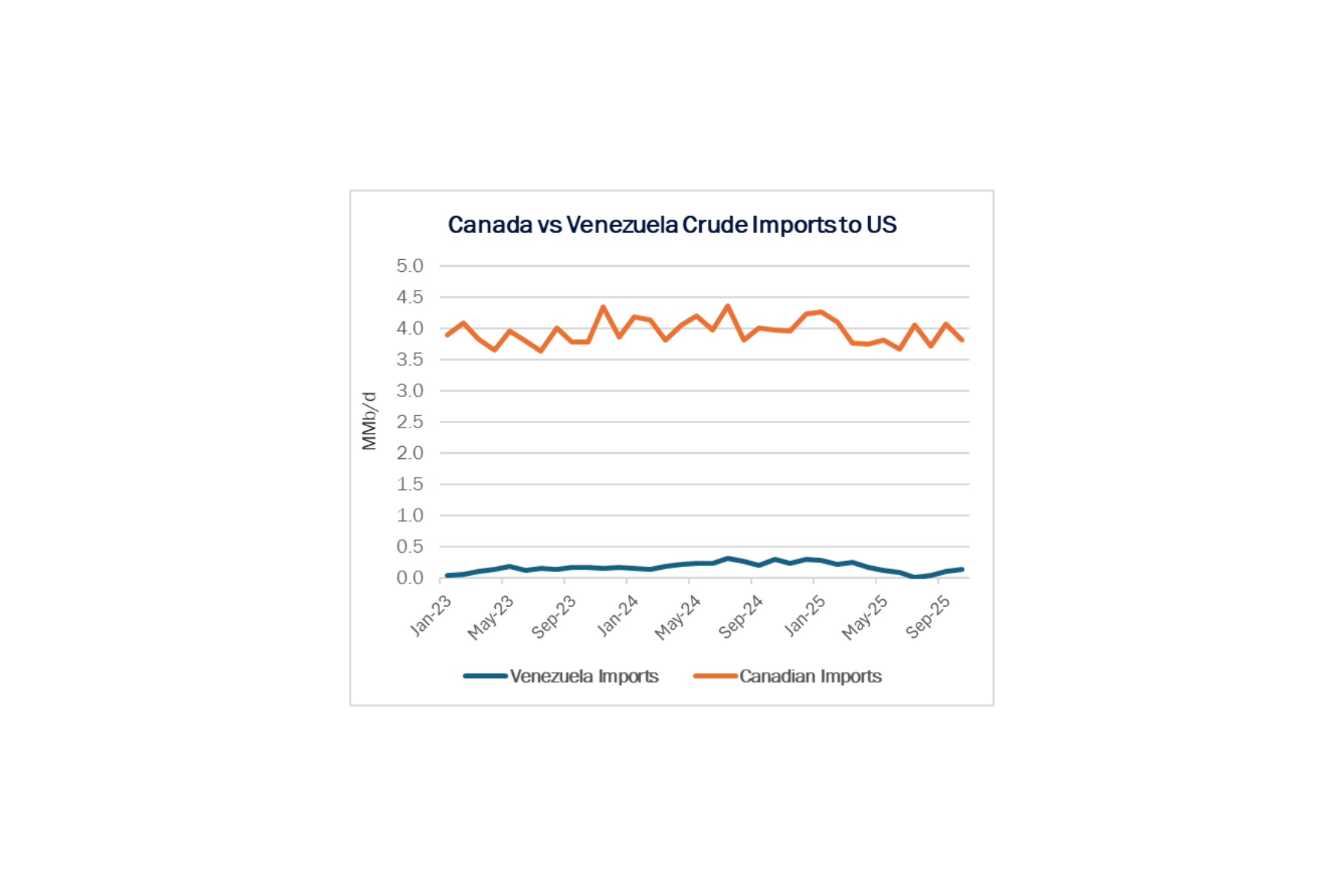

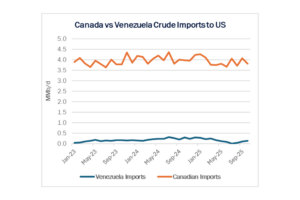

Infrastructure: Boosting Venezuelan oil imports would boost competition for Gulf Coast refineries and undercut Canadian volumes.

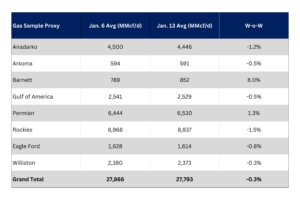

Supply & Demand: The US natural gas pipeline sample, a proxy for change in oil production, decreased 0.3% W-o-W across all liquids-focused basins.

Rigs:

The total US rig count increased by 9 during the week of Jan. 10 from 515 to 524. Liquids-driven basins increased 4 rigs W-o-W from 391 to 395.

- Anadarko (+1): Petroquest Energy

- Eagle Ford (+1): SM Energy

- Permian:

- Delaware (+2): EOG Resources, ConocoPhillips

- Midland (+1): ExxonMobil

- Powder River (-1): WRC Energy

Infrastructure:

Is the US intervention in Venezuela bullish or bearish for energy? Oil prices have gyrated wildly since the US seized Venezuelan President Nicolas Maduro on Jan. 3, and equity prices are higher for several companies.

President Trump faced some skepticism when he met with top energy executives last Friday (Jan. 9) to drum up interest for $100B in investments in the Venezuelan oil sector. ExxonMobil (XOM) CEO Darren Woods said the country is “uninvestable” without significant changes to its legal and commercial systems. XOM, along with ConocoPhillips (COP), are former investors in Venezuela whose assets were nationalized under previous governments. Chevron (CVX) is the only US firm currently active in Venezuela.

Oil prices are another sticking point to a deal. Current and WTI futures under $61/bbl don’t encourage new investments in risky places. Prices are at the point where growth has even stalled in the Permian Basin, where many potential Venezuela investors operate.

The Permian Basin at a Crossroads: Download Why This Pipeline Boom is Different

The Permian’s next big buildout is already taking shape — but this time, the drivers aren’t producers chasing oil. East Daley’s latest white paper reveals how gas demand from AI data centers, LNG exports, and utilities is rewriting the midstream playbook. Over 10 Bcf/d of new capacity and $12 billion in investments are reshaping flows, turning the Permian into a gas powerhouse even as rigs decline. Read Part II: Why This Pipeline Boom is Different

We are skeptical the administration and industry can thread this needle, and bring more Venezuelan crude to market without displacing some Lower 48 supply or pressuring prices. But parties could potentially reach an “America First” deal that places market risk on Canadian production and supporting infrastructure.

Venezuelan crude is a close substitute for the heavy barrels mined in the Canadian oil sands. If Venezuelan barrels are brought to market, they would create more competition for capacity in the US Gulf Coast refinery complexes designed to process these heavy barrels.

If Canadian volumes are displaced, demand would also decline for condensate volumes out of the Midwest (PADD 2) on pipelines like Enbridge’s (ENB) Southern Lights and Pembina’s (PBA) Cochin. In addition to reduced condensate transport, volumes on crude pipelines from Canada to the US such as TransMountain, Keystone and the Enbridge Mainline may be pressured.

If US producers can capitalize on returning Venezuelan barrels to market, those facing the most risk are likely to be Canadian producers and Canadian midstream companies.

Supply and Demand

The US natural gas pipeline sample, a proxy for change in oil production, decreased 0.3% W-o-W across all liquids-focused basins.

The only weekly increases occurred in the Barnett by 8.0% and the Permian by 1.3%. Small decreases were seen in other basins. The most significant decreases occurred from the Rockies (-1.5%), Eagle Ford (-0.8%) and Anadarko (-1.2%). The Rockies and the Gulf of America have a high correlation between gas volumes and crude oil volumes, whereas the Permian and Eagle Ford basins correlation is less than 45%.

As of Jan. 20, there is currently no refining capacity offline for planned maintenance, as refinery outages remain at a low.

Vessel traffic monitored by EDA along the Gulf Coast increased W-o-W. There were 29 vessels loaded for the week ending Jan. 17, continuing a four-week increase from the 18 vessels loaded the week of Dec. 20, 2025.

Presented by ARBO

Tariffs:

Gray Oak Pipeline, LLC: Certain available capacity discounts were increased.

Magellan Pipeline Company, L.P.: The tariffs were revised to add a new product and to update the product grade document to be consistent with ONEOK’s product grade documents.

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at [email protected] or phone at 202-505-5296. https://www.goarbo.com/