Executive Summary:

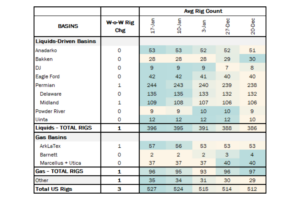

Rigs: The total US rig count increased during the week of Jan. 17 from 524 to 527.

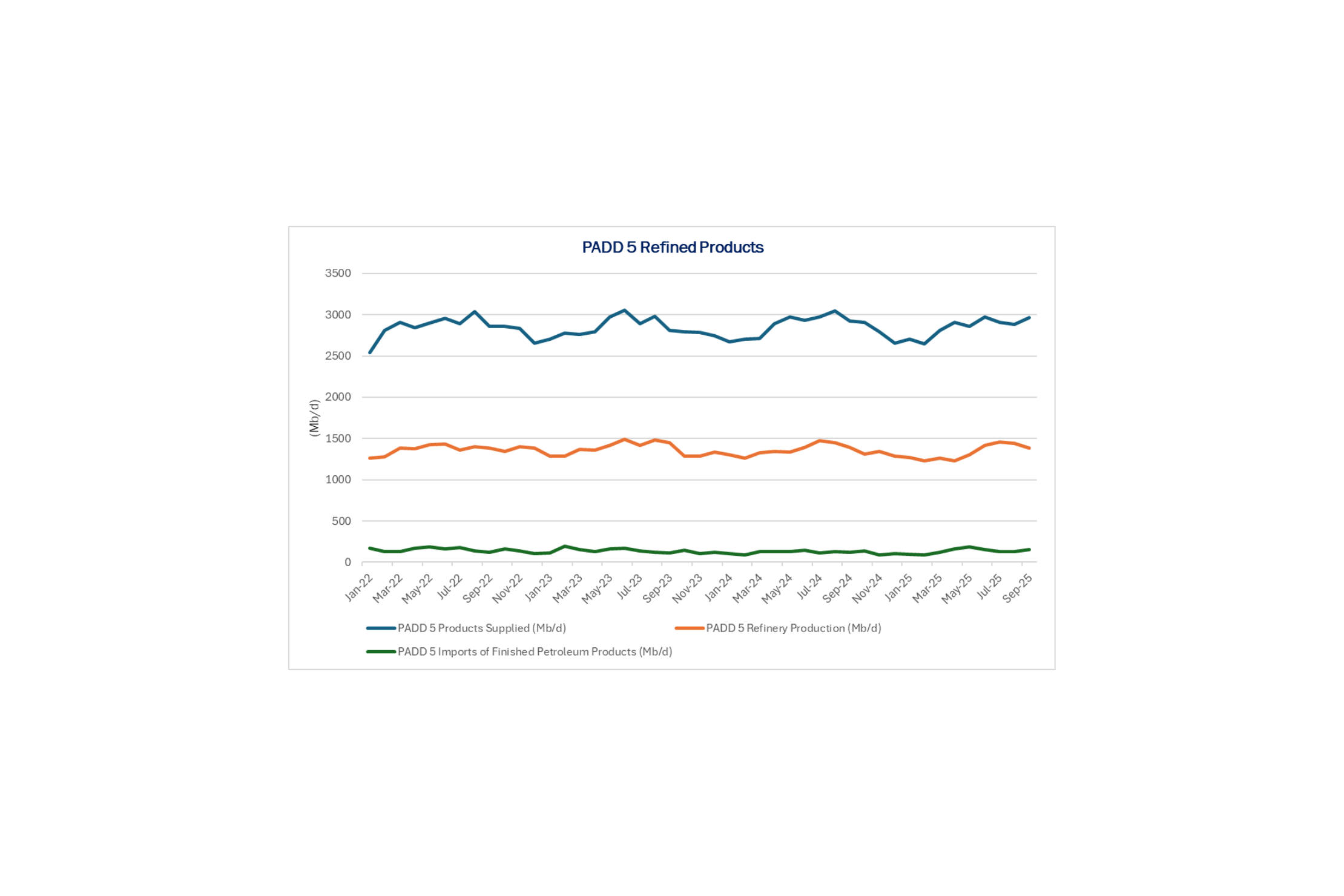

Infrastructure: California’s demand for refined products is in the spotlight after Phillips 66 and Kinder Morgan launched a second open season for the Western Gateway Pipeline.

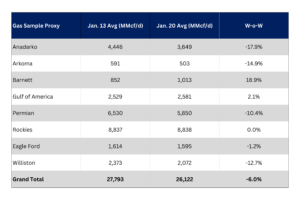

Supply & Demand: The US natural gas pipeline sample, a proxy for change in oil production, decreased 6.0% W-o-W across all liquids-focused basins.

Rigs:

The total US rig count increased by 3 during the week of Jan. 17, from 524 to 527. Liquids-driven basins gained 1 rig W-o-W, from 395 to 396.

- Permian:

- Midland (+1): LRP Energy LLC

Infrastructure:

California’s demand for refined products is in the spotlight after Phillips 66 (PSX) and Kinder Morgan (KMI) launched a second open season for the Western Gateway Pipeline. The company aims to lock in commitments for the remaining capacity while expanding the project’s commercial reach.

The latest open season, launched Jan. 16, follows a successful first open season in October that drew significant shipper interest and executed some firm commitments. The biggest change in the second round is new access to the Los Angeles market via KMI’s Santa Fe Pacific Pipeline (SFPP), along with additional origin points that broaden supply optionality.

East Daley covered the original open season for Western Gateway, outlining how Kinder Morgan would reverse the western leg of the SFPP system from Colton, CA to Phoenix, AZ. The reversal would enable east-to-west product flows into California, with additional connectivity into Las Vegas via KMI’s Calnev Pipeline. The project also would reverse the Gold Pipeline, which currently moves refined products from Borger, TX to St. Louis, to push volumes westward instead. The Gold Pipeline connects to PSX refineries in Borger; Ponca City, OK; and Wood River, IL, representing 700 Mb/d of combined capacity.

The shipper interest generated during the first open season appears to be a key driver behind the latest announcement. While the core route is unchanged, the second open season includes a few important commercial expansions. First, it adds direct access to the Los Angeles market via a joint tariff, supported by the planned reversal of one of KMI’s existing SFPP lines between Watson and Colton, CA. Second, the latest open season adds additional origin points, allowing for greater supply diversification and customer optionality. As outlined in the updated project language, Western Gateway Pipeline will be fed by supplies connected to Borger, as well as other origin points.

With competitive pressure rising from HF Sinclair’s and ONEOK’s competing refined products projects, Phillips 66 and Kinder Morgan appear focused on differentiating Western Gateway through a combination of multiple supply entry points and expanded market connectivity. Early shipper interest indicates Western Gateway is competitively positioned. If developed as proposed, the project could contribute to a longer-term shift in California supply toward domestic refined products and away from overseas imports.

Supply and Demand

The US natural gas pipeline sample, a proxy for change in oil production, decreased 6% W-o-W across all liquids-focused basins. This occurred due to freeze-offs caused by the massive winter storm across the US this past weekend.

The only weekly increases occurred in the Barnett by 18.9% and Gulf of America by 2.1%. On top of this, decreases were seen in the rest of the basins. The most significant decreases occurred from the Anadarko by 17.9%, Arkoma by 14.9% and Permian by 10.4%. The Rockies and the Gulf of America have a high correlation between gas volumes and crude oil volumes, whereas the Permian and Eagle Ford basins correlation is less than 45%.

As of Jan. 26, there is currently 0 Mb/d of refining capacity offline for planned maintenance, as refinery outages remain at a low.

Vessel traffic monitored by EDA along the Gulf Coast remained the same W-o-W. There were 29 vessels loaded for the week ending Jan. 24, the same as last week. Vessel traffic has seen multiple W-o-W increases from the 18 vessels loaded the week of Dec. 20, 2025.

Presented by ARBO

Tariffs:

Gray Oak Pipeline, LLC: Certain available capacity discounts were increased.

Magellan Pipeline Company, L.P.: The tariffs were revised to add a new product and to update the product grade document to be consistent with ONEOK’s product grade documents.

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at [email protected] or phone at 202-505-5296. https://www.goarbo.com/