Executive Summary:

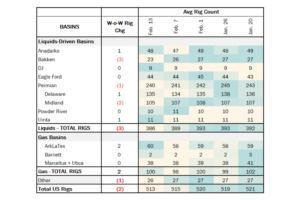

Rigs: The total US rig count decreased during the week of Feb. 13 from 515 to 513.

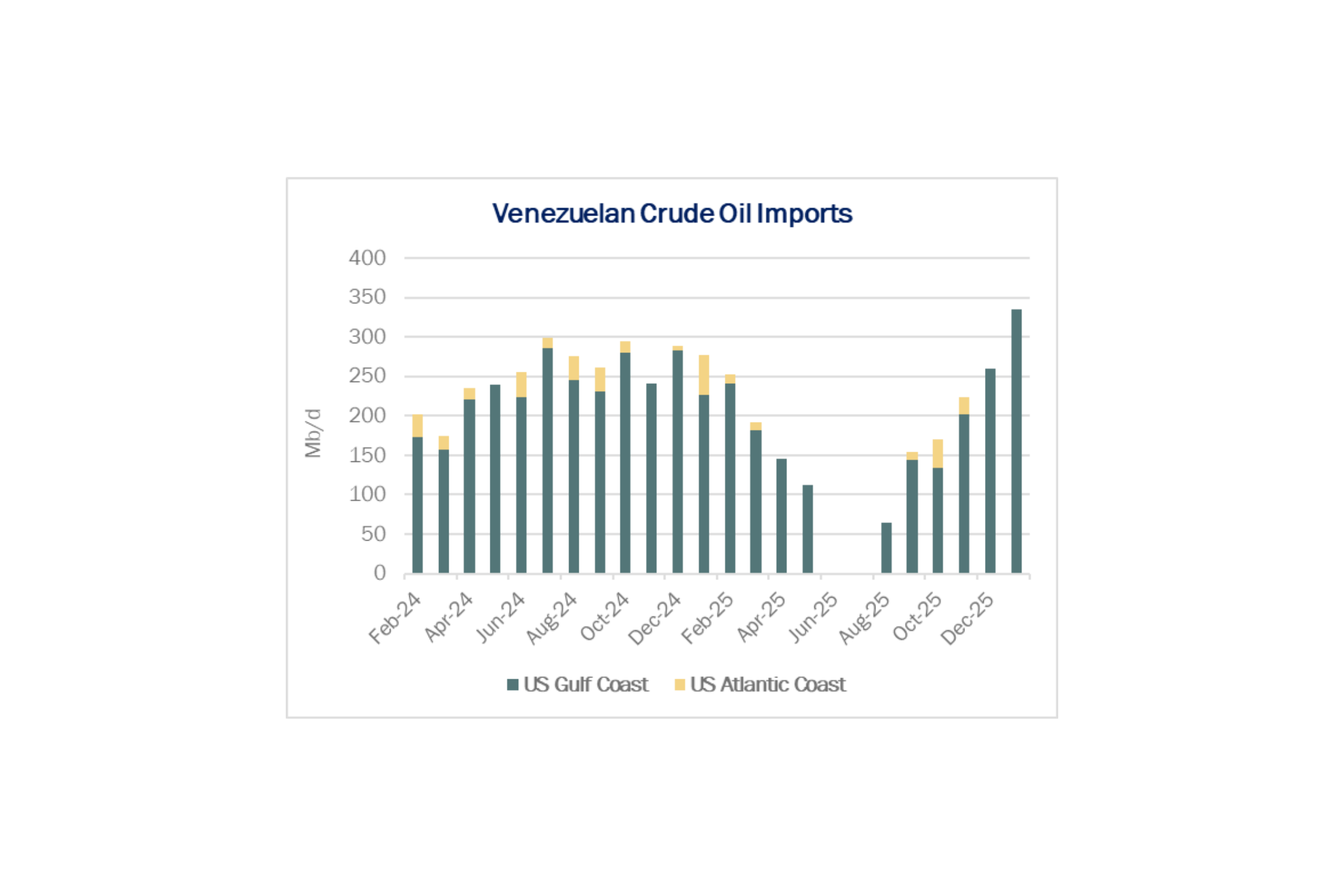

Infrastructure: Valero Energy plans to increase imports of Venezuelan crude as sanctions ease and trade flows reopen.

Supply & Demand: The US natural gas pipeline sample, a proxy for change in oil production, decreased -0.9% W-o-W across all liquids-focused basins.

Rigs:

The total US rig count decreased during the week of Feb. 13 from 515 to 513. Liquids-driven basins decreased 3 rigs W-o-W, from 389 to 386.

- Anadarko (+1): Continental Resources

- Bakken (-3): Devon Energy

- Permian:

- Delaware (+1): EOG Resources

- Midland (-2): Hannathon Petroleum

Uinta (+1): Star Oil Operating Co

Infrastructure:

Valero Energy (VLO) is positioning to capitalize on improved access to the Venezuela market as sanctions ease and trade flows reopen.

The company has engaged with three authorized sellers of Venezuelan crude oil and expects to purchase up to 6.5 MMbbl in March (~210 Mb/d). If those volumes materialize as planned, Valero would join Chevron (CVX) as the largest US refiners of Venezuelan crude.

Chevron imported ~220 Mb/d of Venezuelan crude in January and plans to raise import volumes in the coming months. Phillips 66 (PSX) and CITGO Petroleum are also joining the trend by moving to buy heavy crude directly from Venezuela’s state-owned PDVSA starting in April 2026.

This strategy fits well with Valero’s refinery network. Venezuela produces heavy sour crude, and Valero has some of the most advanced heavy-cracking assets on the Gulf Coast. VLO can run these barrels through its Texas City, Bill Greehey and Port Arthur refineries. Valero has ample experience with Venezuelan barrels; before sanctions were imposed in 2019, the company processed ~240 Mb/d of Venezuelan heavy crude.

Since then, Valero has upgraded its ability to process heavy crude. In 2023, VLO completed a major coker project at Port Arthur, increasing the refinery’s crude throughput capacity to ~435 Mb/d and boosting its ability to upgrade heavy, high-resid crude slates. The expansion gives Valero more flexibility to absorb Venezuelan volumes today than it had in the pre-sanctions period.

As Venezuelan volumes return, the impact will extend beyond Valero’s slate into the broader heavy crude market. Venezuelan heavy competes directly with Western Canadian Select (WCS) and Mexican Maya due to similar quality and refining economics. On its 4Q25 earnings call, management acknowledged this dynamic and indicated that Venezuelan crude will comprise a significant portion of its heavy slate in the coming months.

If Venezuelan crude continues to ramp, it could displace other heavy barrels in the Gulf Coast market, or force these suppliers to lower prices to remain competitive. That risk is particularly acute for Canadian barrels. For example, VLO’s Texas City refinery received ~827 Mb of crude in January from South Bow (SOBO) Marketing, a company closely tied to Canadian heavy crude logistics.

Valero is well positioned to capture upside from returning Venezuelan heavy sour volumes given its Gulf Coast refiners and expanded coking capacity. As supply ramps, the company could enhance its feedstock margin advantage, while WCS and Maya barrels face heightened competitive pressure on the Gulf Coast. – Keland Rumsey Tickers: CVX, PSX, SOBO, VLO.

Supply and Demand

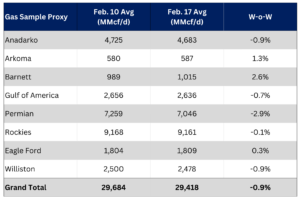

The US natural gas pipeline sample, a proxy for change in oil production, decreased -0.9% W-o-W across all liquids-focused basins.

Following the late-January freeze-offs associated with Winter Storm Fern, volumes showed mixed W-o-W performance and continue to normalize. On a basin level, the Barnett and Arkoma increased 2.6% and 1.3%, respectively. The Permian declined 2.9%, and the Anadarko and Williston each decreased 0.9%. The Rockies, Eagle Ford and Gulf of America all remained relatively flat.

Production remains below early February levels but is stabilizing after Fern. The Rockies and the Gulf of America have a high correlation between gas volumes and crude oil volumes, whereas the Permian and Eagle Ford basins correlation is less than 45%.

As of Feb. 25, there are no active refinery outages.

Vessel traffic monitored by EDA along the Gulf Coast increased W-o-W. A total of 27 vessels were loaded for the week ending Feb. 21, marking an increase following declines in each of the prior two weeks.

Presented by ARBO

Tariffs:

Gray Oak Pipeline, LLC: Certain available capacity discounts were increased.

Magellan Pipeline Company, L.P.: The tariffs were revised to add a new product and to update the product grade document to be consistent with ONEOK’s product grade documents.

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at [email protected] or phone at 202-505-5296. https://www.goarbo.com/