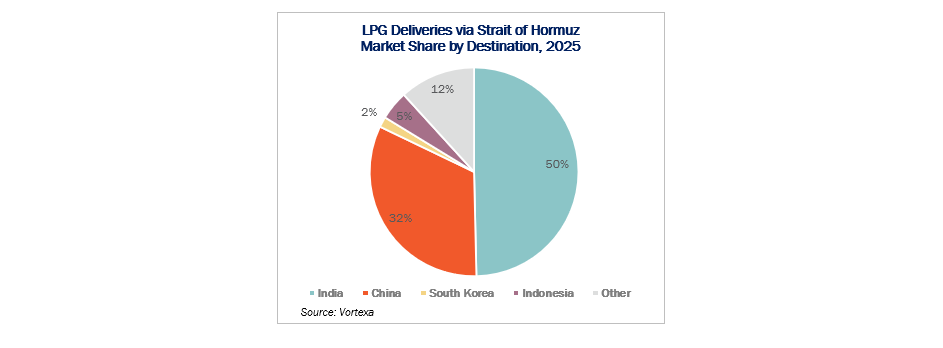

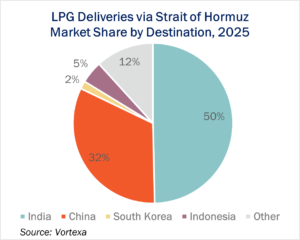

The market already understands the macro story: India cannot easily replace LPG cargoes from the Persian Gulf disrupted by the Iran war, and the US is the only scalable alternative. The next layer of analysis is where East Daley has the edge. This will not be a uniform US export response. It will be a terminal-by-terminal response.

The binding constraint is no longer simply LPG availability. It is export infrastructure. Which docks have open capacity, which operators have flexibility in product mix, and which terminals can actually move additional barrels into India over the next 30 to 45 days?

India’s residential LPG demand requires blended cargoes of propane and butane, adding another layer of constraint to the US export response. Not every terminal can easily assemble mixed LPG cargoes, and butane-handling capacity in particular is already tight at several key facilities.

India’s residential LPG demand requires blended cargoes of propane and butane, adding another layer of constraint to the US export response. Not every terminal can easily assemble mixed LPG cargoes, and butane-handling capacity in particular is already tight at several key facilities.

Details are available in East Daley Analytics’ NGL Hub Model. Energy Transfer’s (ET) Nederland terminal appears effectively maxed out on butane capacity. While the company is planning storage and infrastructure expansions, those additions will not be available in the near term. Phillips 66’s (PSX) Freeport terminal is similarly running near capacity. That leaves a smaller group of facilities capable of increasing shipments in the short term, primarily Targa Resource’s (TRGP) Galena Park and Enterprise Products’ (EPD) Hydrocarbons terminals.

Operational disruptions also compound the constraint. Recent fog events along the Gulf Coast delayed vessel movements and left several cargoes backed up at export docks. East Daley’s latest LPG export forecast in the NGL Hub Model shows roughly 100 Mb/d of theoretical spare capacity across Gulf Coast (PADD 3) terminals for March 2026, though filling that space may prove difficult given product mix limitations and scheduling delays.

Outside the Gulf Coast, ET’s Marcus Hook terminal in the Northeast provides another potential outlet. East Daley estimates roughly 75 Mb/d of available export capacity there, though cargoes would face longer sailing distances to India.

Looking ahead, Enterprise’s Neches River Phase 2 expansion could materially shift the export picture if disruptions persist. The project is scheduled to begin service in 2Q26. If operational in early April, it could capture a significant share of incremental demand, potentially adding as much as 360 Mb/d of export capacity.

In the near term, replacement supply from the US to India will likely emerge unevenly, with cargoes concentrated at terminals that have both spare dock space and the ability to assemble blended LPG barrels. – Julian Renton Tickers: EPD, ET, PSX, TRGP.

Download Part II of East Daley’s Permian Basin White Paper Series

Download Part II of East Daley’s Permian Basin White Paper Series

The Permian Basin’s next big buildout is already taking shape, but this time the driver isn’t crude oil. In The Permian Basin at a Crossroads: Why This Pipeline Boom is Different, East Daley Analytics’ latest white paper reveals how gas demand from AI data centers, utilities and LNG exports is rewriting the midstream playbook in the leading US basin. Over 10 Bcf/d of new capacity and $12 billion in investments are reshaping flows, turning the Permian into a gas powerhouse even as rigs decline. Read Part II: Why This Pipeline Boom is Different

Meet Daley, the Best AI Tool in Energy

Meet Daley, the newest member of our energy team. Our new AI assistant is live and available to all East Daley Analytics clients. Early feedback has been phenomenal. Daley is platform-specific and only pulls from East Daley’s own proprietary data and content. It’s not open-source or generic AI, but built to understand our structure, language and analytics. Whether you’re looking for a specific metric, forecast or explanation, Daley can get you there quicker. — Reach out to learn more about Daley!

The Daley Note

Subscribe to The Daley Note for energy insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices and EDA research likely to affect markets in the short term.