Tallgrass Energy’s plan to construct a gas pipeline from the Permian Basin to Rockies Express Pipeline (REX) has shaken up the midstream space. The project would be a boon for Permian producers, but could also affect how REX receives gas from traditional supply sources.

Tallgrass on May 13 announced precedent agreements for the new pipeline out of the Permian. REX currently has contracts to source ~3.1 Bcf/d from Northeast interconnects, ~0.9 Bcf/d from Rockies interconnects, and ~0.275 Bcf/d from interconnects in the Midwest. East Daley Analytics believes some of this supply could be displaced if Tallgrass can sign up Permian customers for the full 2.4 Bcf/d offered in the upcoming open season.

To balance the Macro Supply & Demand model, East Daley currently estimates gross gas production in the Permian Basin will grow 1.7 Bcf/d by 2030. Northeast gas production grows 3.5 Bcf/d in our forecast, and supply from Rockies basins increases 0.5 Bcf/d over the same period.

Some of this growth potential in the Northeast and Rockies may be at risk if the Tallgrass project runs full. Of course, surging power demand estimates could support a larger gas market. EDA forecasts 5.5 Bcf/d of demand growth by 2030 in the Macro Supply & Demand report; however, data centers present a much larger opportunity set than we credit, with power and infrastructure bottlenecks tempering our current outlook.

Some of this growth potential in the Northeast and Rockies may be at risk if the Tallgrass project runs full. Of course, surging power demand estimates could support a larger gas market. EDA forecasts 5.5 Bcf/d of demand growth by 2030 in the Macro Supply & Demand report; however, data centers present a much larger opportunity set than we credit, with power and infrastructure bottlenecks tempering our current outlook.

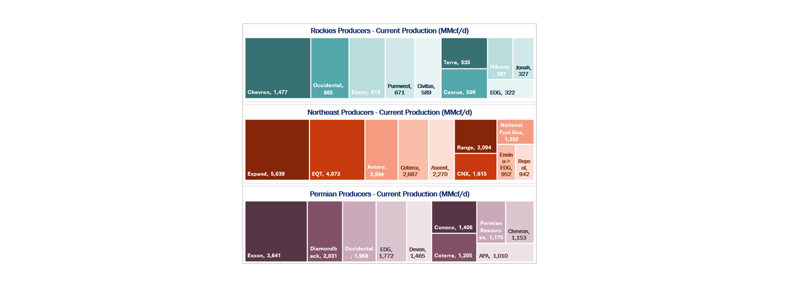

If increased Permian production does push back on Northeast and Rockies growth, E&Ps in these regions face downside risk to the growth outlook. EDA tracks producer volumes by basin in Energy Data Studio, including supply that could be affected by the Tallgrass project (see figure). Notably, EQT and Antero Resources (AR) are the second- and third-largest producers in the Northeast but do not have offsetting exposure to potential Permian growth. These two companies are also among the top three shippers on REX, and could see more competition as their gas competes directly with Permian sources.

Alternatively, gas demand could grow to a magnitude that requires all the existing REX receipts, plus the planned 2.4 Bcf/d Tallgrass is offering in the open season. Flow data indicates significant seasonal volatility in samples at points west of Illinois. During periods of peak demand, utilities in Chicago draw gas from both ends of the pipe, and there is potential for increased demand based on the 7.7 GW of data centers planned in Illinois. In either case, the upside is evident for producers with gassier Permian acreage. – Zach Krause Tickers: AR, EQT.

NEW – The Burner Tip

The Burner Tip provides East Daley’s weekly coverage of natural gas markets. Every Thursday, The Burner Tip brings you our expert perspective on drivers shaping prices and flows in North America — including production trends, infrastructure dynamics, and forward-looking fundamentals — all grounded in EDA’s proprietary data and models. Whether you’re trading, investing, or managing risk, The Burner Tip delivers the insights you need to drive smarter strategy. Subscribe now to The Burner Tip!

Data Center Demand Monitor – Available Now!

The Data Center Demand Monitor is your go-to source for tracking data center projects and demand. We monitor and visualize nearly 300 US data center projects. Use Data Center Demand Monitor to forecast demand, identify pipeline corridors and track data center projects. — Request your demo now of the Data Center Demand Monitor!

The Daley Note

Subscribe to The Daley Note for energy insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices and EDA research likely to affect markets in the short term.