Executive Summary:

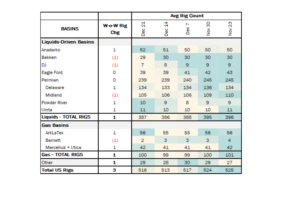

Rigs: The total US rig count increased during the week of Dec 21 from 513 to 516.

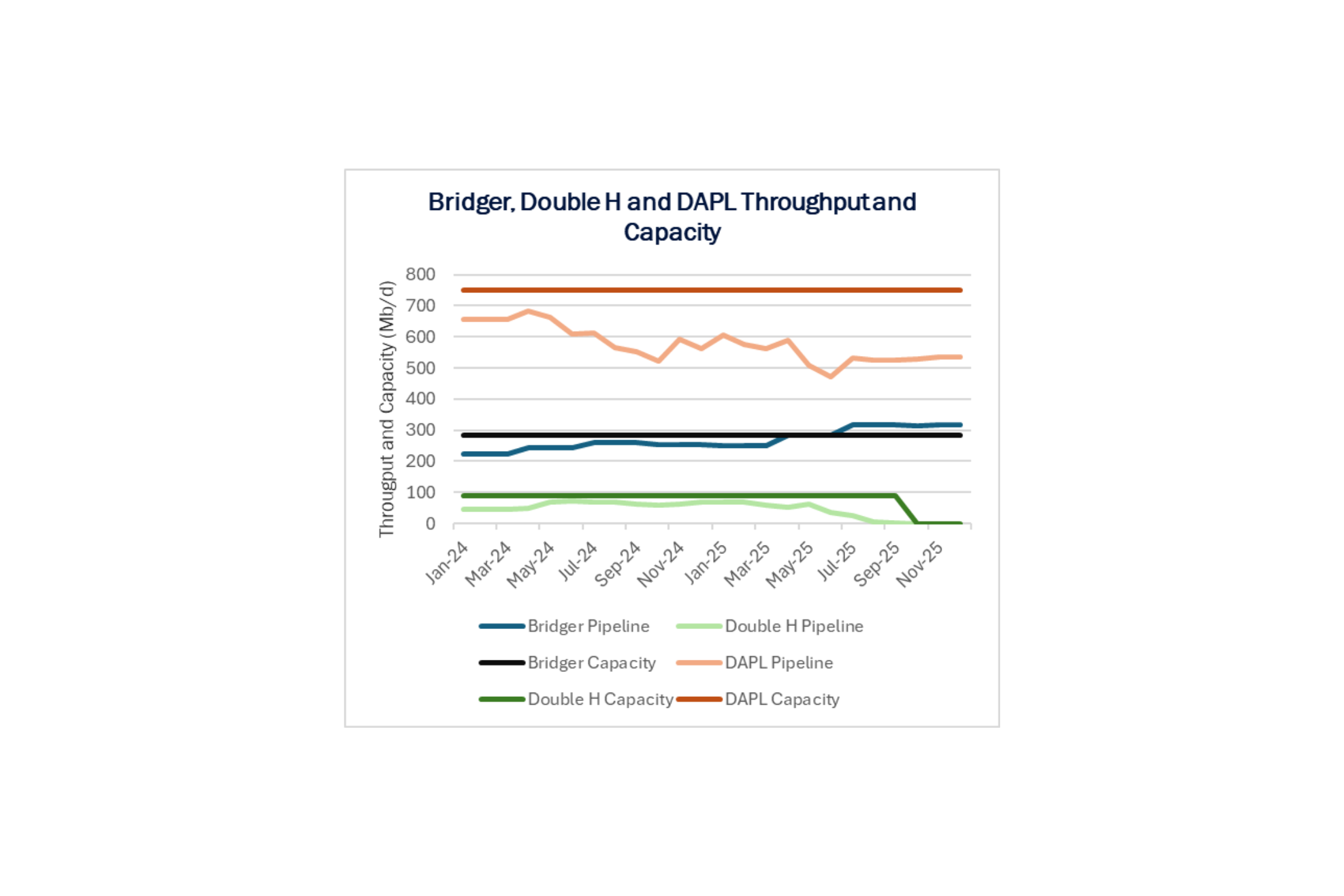

Infrastructure: Crude markets have lost the services of Kinder Morgan’s (KMI) Double H Pipeline, which suits the True Companies just fine.

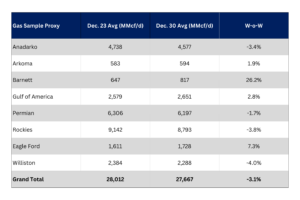

Supply & Demand: The US natural gas pipeline sample, a proxy for change in oil production, decreased 3.1% W-o-W across all liquids-focused basins.

Rigs:

The total US rig count increased during the week of Dec 21 from 513 to 516. Liquids-driven basins increased one rig W-o-W from 386 to 387.

- Anadarko (+1): Vincent Oil

- Uinta (+1): SM Energy

- Powder River (+1): Ballard Petroleum

- Permian:

- Delaware (+1): Chevron

- Midland (-1): ExxonMobil

- Bakken (-1): Chord Energy

- DJ (-1): ExxonMobil

Infrastructure:

Crude markets have lost the services of Kinder Morgan’s (KMI) Double H Pipeline, which suits the True Companies just fine. True’s Bridger Pipeline saw a big jump in volumes out of the Bakken in 3Q25 when KMI began converting Double H to NGLs. We expect Dakota Access Pipeline (DAPL) will also benefit when updated shipper data is available.

Kinder Morgan in 2024 announced plans to convert the Double H crude oil line to NGL transport. Shippers began migrating off Double H in 3Q25, and KMI temporarily closed the pipeline in 4Q25 to complete upgrades ahead of the conversion. Double H runs from Dore, ND to the Guernsey market in Wyoming and could carry up to 88 Mb/d of crude oil. Throughput in 2024 averaged 60 Mb/d, according to East Daley Analytics’ Crude Hub Model.

The Permian Basin at a Crossroads: Download Why This Pipeline Boom is Different

The Permian’s next big buildout is already taking shape — but this time, the drivers aren’t producers chasing oil. East Daley’s latest white paper reveals how gas demand from AI data centers, LNG exports, and utilities is rewriting the midstream playbook. Over 10 Bcf/d of new capacity and $12 billion in investments are reshaping flows, turning the Permian into a gas powerhouse even as rigs decline. Read Part II: Why This Pipeline Boom is Different

We predicted at the time of the KMI announcement that the Double H conversion would constrain Bakken egress, a view supported by the latest pipeline data. Bridger Pipeline utilization, which averaged 85.9% in 2024, surged to 99.6% through September. Looking deeper, Bridger throughput in 3Q25 averaged 317 Mb/d, or 10% above its nameplate capacity of 285 Mb/d. The gains are directly in line with the gradual closing of Double H, and suggest that True is using drag-reducing agents (DRAs) to move barrels over Bridger’s capacity limit.

DAPL is another pipeline that is likely to absorb volumes displaced by the Double H closure. DAPL has run at 72.5% average utilization through 2025, leaving ~206 Mb/d in spare capacity to take more barrels out of the Bakken.

Supply and Demand

The US natural gas pipeline sample, a proxy for change in oil production, decreased 3.1% W-o-W across all liquids-focused basins.

The Eagle Ford sample gained 7.3%, the Arkoma increased 1.9% and the Gulf of America rose 2.8%. On top of this, the Barnett sample jumped by 26.2%. These increases coincide with decreases in the rest of the basins. The most notable decreases occurred in the Anadarko (-3.4%), Permian (-1.7%), Rockies (-3.8%) and Williston (-4.0%). The Rockies and the Gulf of America have a high correlation between gas volumes and crude oil volumes, whereas the Permian and Eagle Ford basins correlation is less than 45%.

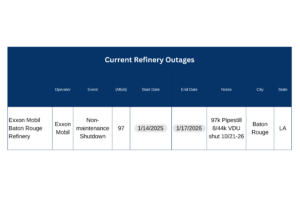

As of Jan. 5, there is currently no refining capacity offline for planned maintenance, as refinery outages remain at a low. Later this month, a non-maintenance shutdown of 97 Mb/d is expected for half of a week at ExxonMobil’s Baton Rouge refinery.

Vessel traffic monitored by EDA along the Gulf Coast increased W-o-W. There were 26 vessels loaded for the week ending Jan. 3, following a two-week increase from 23 the week ending Dec. 27 and 18 the week ending Dec. 20.

Presented by ARBO

Tariffs:

Gray Oak Pipeline, LLC: Certain available capacity discounts were increased.

Magellan Pipeline Company, L.P.: The tariffs were revised to add a new product and to update the product grade document to be consistent with ONEOK’s product grade documents.

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at [email protected] or phone at 202-505-5296. https://www.goarbo.com/