Executive Summary:

Infrastructure: US NGL production is outpacing fractionation capacity, with ~900 Mb/d of new capacity needed in Mont Belvieu by 2032 to maintain balance.

Exports: NGL exports declined in the week ending April 3, down 6.3% W-o-W.

Rigs: The total US rig count decreased during the week of March 28 from 514 to 513. Liquids-driven basins decreased W-o-W from 395 to 392.

Flows:

Infrastructure:

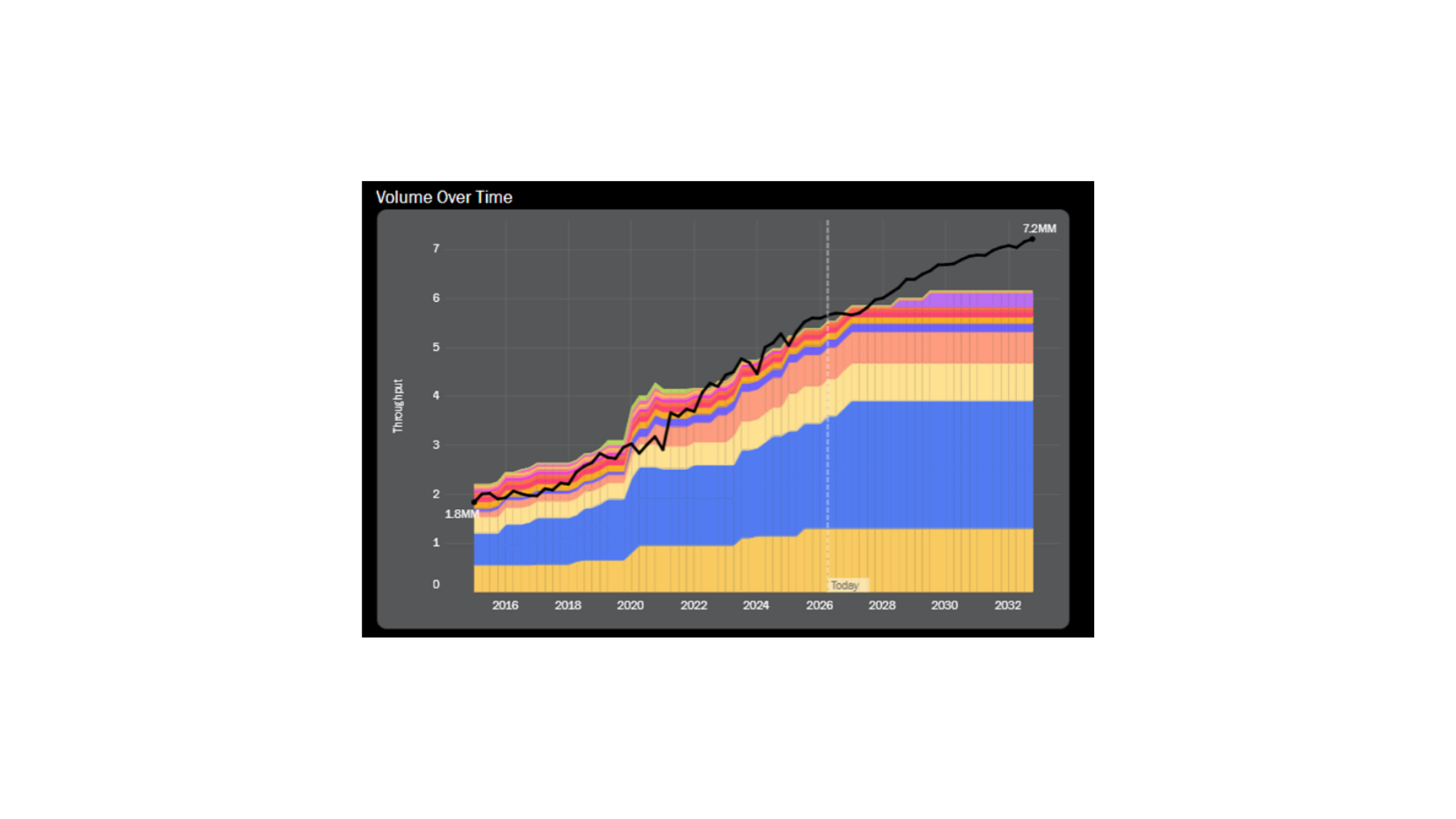

Surging US NGL production is beginning to outpace one of the most overlooked constraints in the value chain: fractionation. East Daley Analytics forecasts the need for ~900 Mb/d of incremental fractionation capacity in Mont Belvieu by 2032 to keep the system in balance.

Even with currently planned expansions, fractionation capacity comes under pressure by YE27. The tightening builds into a more visible structural imbalance later this decade; our NGL Hub Model shows ~200 Mb/d of excess Y-grade supply relative to frac capacity by YE28.

The implication is clear: Fractionation is no longer a background service in the NGL chain. It is becoming a core constraint on growth.

If capacity additions fail to keep pace with supply, the risk is not isolated to Mont Belvieu. Barrels begin to back up across the system, pressuring Y-grade pricing, weakening recovery and ultimately threatening upstream economics. In an extreme case, insufficient fractionation capacity could force production shut-ins further up the value chain.

That setup favors the incumbents. Enterprise Products (EPD), Energy Transfer (ET), Targa (TRGP), ONEOK (OKE) and Phillips 66 (PSX) are best positioned to capture the upside from a tightening fractionation market given their scale and integration in Mont Belvieu.

See East Daley’s NGL Hub Model for more detail on the outlook for NGL supply, demand and pipeline flows.

.

Exports:

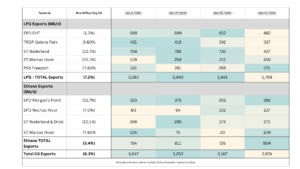

NGL exports declined in the week ending April 3, down 6.3% W-o-W.

At the terminal level, PSX Freeport posted a 17.6% increase in LPG exports, but pullbacks across most other terminals drove a 7.2% W-o-W decline overall.

For ethane exports, Enterprise’s Neches River had a 77.8% increase, but this gain was offset by decreases across rest of the terminals, resulting in a 3.4% overall drop in total ethane exports.

Rigs:

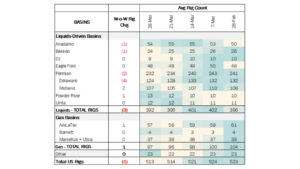

The total US rig count decreased during the week of March 28 from 514 to 513. Liquids-driven basins decreased W-o-W from 395 to 392.

- Anadarko (-1): Basin Operating Services LLC

- Bakken (-1): Kraken Resources

- Permian

- Delaware (-4): SM Energy

- Midland (+2): Ovintiv

- Powder River (+1): 1876 Resources LLC

Calendar: