Executive Summary:

Infrastructure: Escalating military conflict in the Middle East has added gasoline to a bullish setup for US LPG exporters.

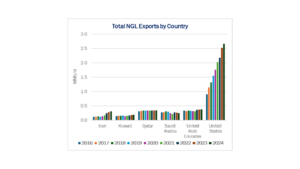

Exports: NGL exports surged 10.8% W-o-W for the week ending Feb. 27, driven by a sharp rebound in ethane exports, which jumped 75% W-o-W.

Rigs: The total US rig count decreased during the week of Feb. 21 from 519 to 518. Liquids-driven basins decreased W-o-W from 389 to 388.

Flows: US natural gas volumes in pipeline samples declined 1.3% W-o-W, averaging 81.7 Bcf/d for the week ending March 1.

Calendar: Basin Supply and Demand Updates

Infrastructure:

Escalating military conflict in the Middle East has added gasoline to a bullish setup for US LPG exporters. East Daley Analytics expects near-term dislocation in the global LPG market resulting from the war and a key terminal outage, creating upside for several companies.

The US and Israel launched joint strikes against Iran over the weekend, killing the country’s supreme leader, Ayatollah Ali Khamenei. Iran retaliated with a wave of drone and missile attacks targeting infrastructure in neighboring states, effectively shutting tanker traffic through the Strait of Hormuz.

The Middle East hostilities follow a recent outage at the Juaymah LPG terminal in Saudi Arabia. On Feb. 23, Saudi Aramco halted LPG exports after finding damage to part of its delivery system.

According to Vortexa ship tracking data, Juaymah exports average more than 170 Mb/d, with February volumes tracking closer to 180 Mb/d prior to the disruption. A significant share of those barrels move to India, the same demand center where US suppliers have been working to expand market share.

For perspective, US LPG exports to India have reached highs near 180 Mb/d but more frequently remain below 100 Mb/d. Juaymah alone represents a swing supplier equivalent to the full upside case for US shipments to India.

According to East Daley’s NGL Hub Model, all major US Gulf Coast terminals have exposure to India, including Energy Transfer’s (ET) Nederland, Enterprise’s (EPD) EHT, Targa Resource’s (TRGP) Galena Park and Phillips 66’s (PSX) Freeport. Even Marcus Hook in the Northeast has placed cargoes in the subcontinent. The infrastructure and supply are available. The key variables are price and freight.

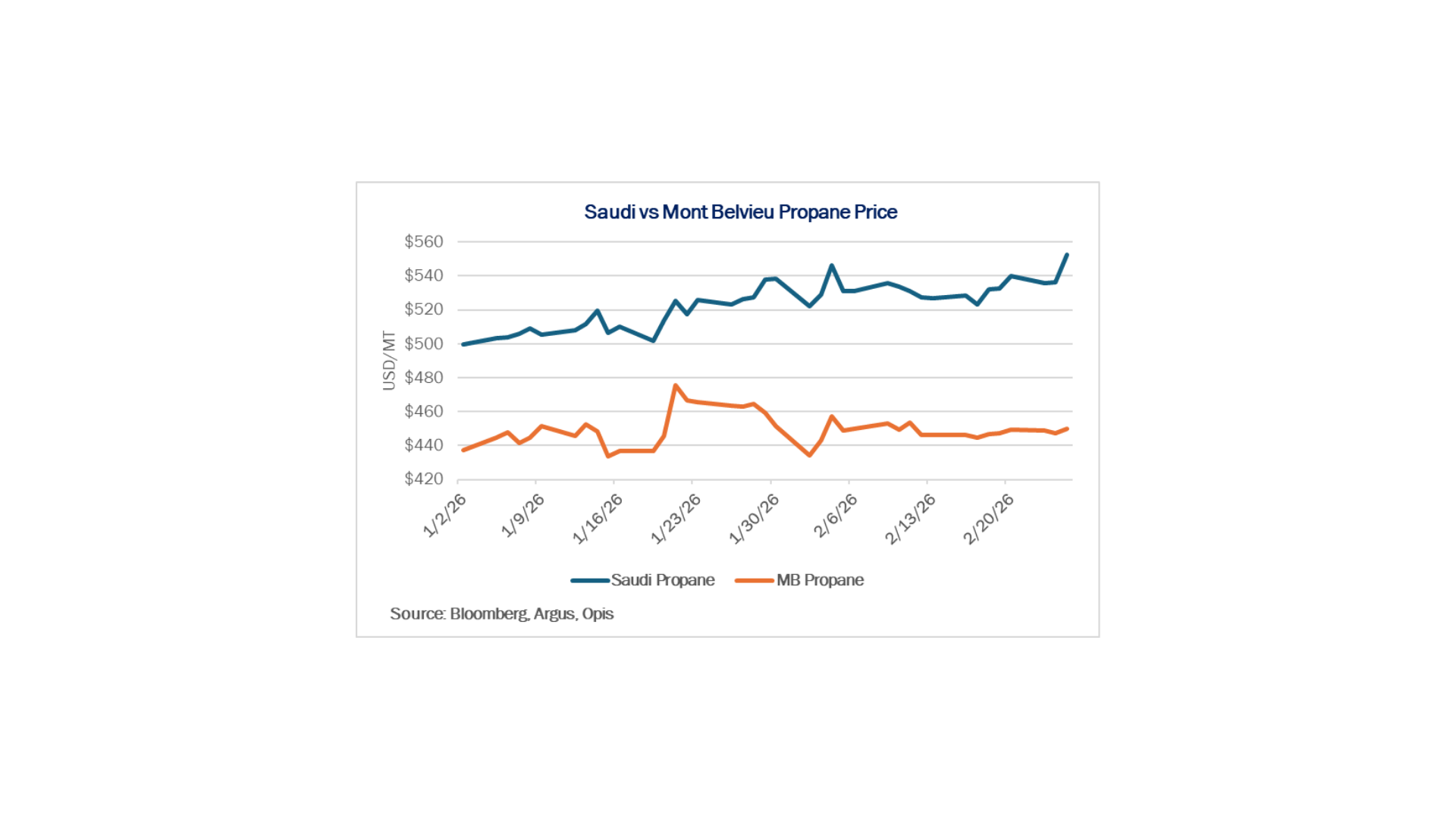

Mont Belvieu pricing is relatively weak relative to Saudi propane (shown in figure), keeping US LPG competitive on a delivered price basis. Freight costs to India are higher than from the Middle East, which compresses delivered margins.

East Daley expects near-term upside in US export volumes, particularly from terminals with open capacity such as ET – Nederland and EPD – EHT. If the Juaymah outage and Strait of Hormuz closure drag on, India and other Asian customers will need ready supply and flexibility. The US is the only supplier positioned to respond quickly.

The duration of the disruptions will determine whether this is a brief trade opportunity or a more durable shift in flows.

Exports:

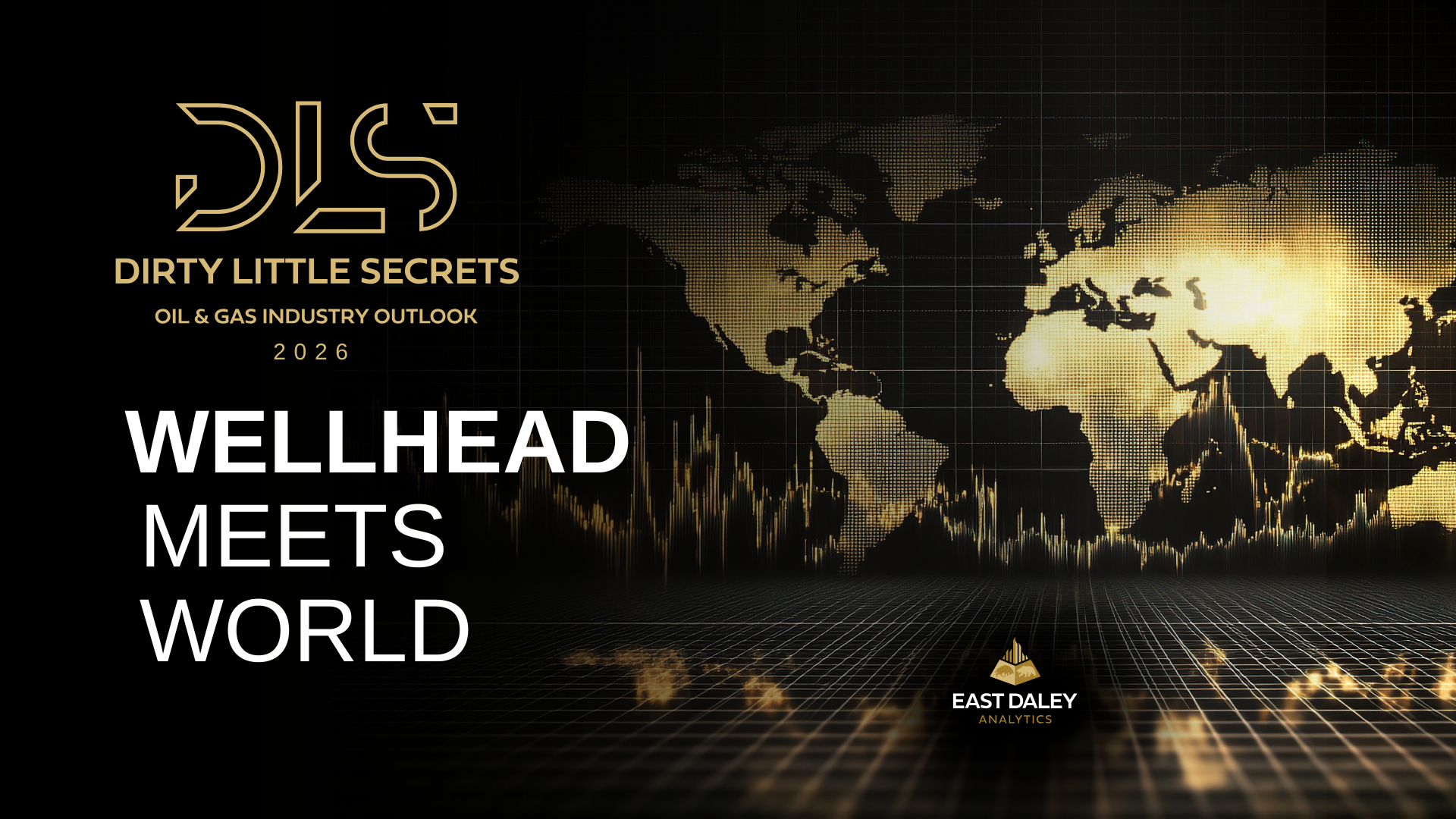

NGL exports rose 10.8% W-o-W for the week ending Feb. 27, driven by a sharp rebound in ethane exports, which jumped 75% W-o-W.

For LPG, declines at ET – Marcus Hook (-63%) and TRGP’s Galena Park (-21.9%) were partially offset by a 38.3% increase at PSX – Freeport, resulting in a 3.4% W-o-W decrease in total LPG exports.

On the ethane side, EPD’s Morgan’s Point was the only terminal to decline, falling 26.5% W-o-W. All other terminals posted sharp increases, with Neches River and ET’s Nederland and Orbit both surging more than 200% W-o-W, pushing total ethane exports up 75%.

Rigs:

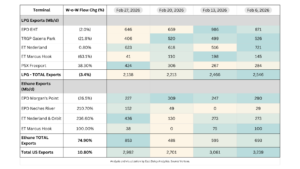

The total US rig count decreased during the week of Feb. 21 from 519 to 518. Liquids-driven basins decreased W-o-W from 389 to 388.

- Anadarko (+2): Territory Resources

- Eagle Ford (+1): Kilam Oil

- Permian (-3)

- Delaware (-2): ExxonMobil

- Midland (-1): Double Eagle

- Powder River (-1): EOG Resources

Flows:

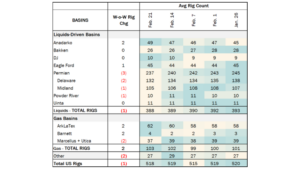

Note: East Daley has vetted our US pipeline samples and upgraded the data tagging, resulting in a more robust capture of production trends from the daily samples.

US natural gas volumes in pipeline samples declined 1.3% W-o-W, averaging 81.7 Bcf/d for the week ending March 1.

Flows in gas basins declined 1.2% to 51.2 Bcf/d. The Marcellus+Utica sample decreased 1.3% to 38.7 Bcf/d, while the Haynesville sample was flat at 11.6 Bcf/d.

Samples in liquids basins declined 0.4% W-o-W to 22.8 Bcf/d. The Permian sample declined 2.7%, while the Anadarko sample increased 2.3%.

Calendar: