Natural Gas Weekly: July 11, 2024

Demand – Hurricane Beryl barreled ashore early Monday morning (July 8) southwest of Houston, causing widespread power outages in southeastern Texas and wiping out a large share of natural gas demand for LNG and power generation.

Beryl made landfall as a Category 1 hurricane with winds of 80 miles per hour, toppling trees and power lines and leaving 2.7 million people without power on Monday in the greater Houston area. Centerpoint Energy and Texas officials said Beryl knocked down 10 transmission lines and many more local power lines across the region. Fortunately flooding from the storm surge was not significant.

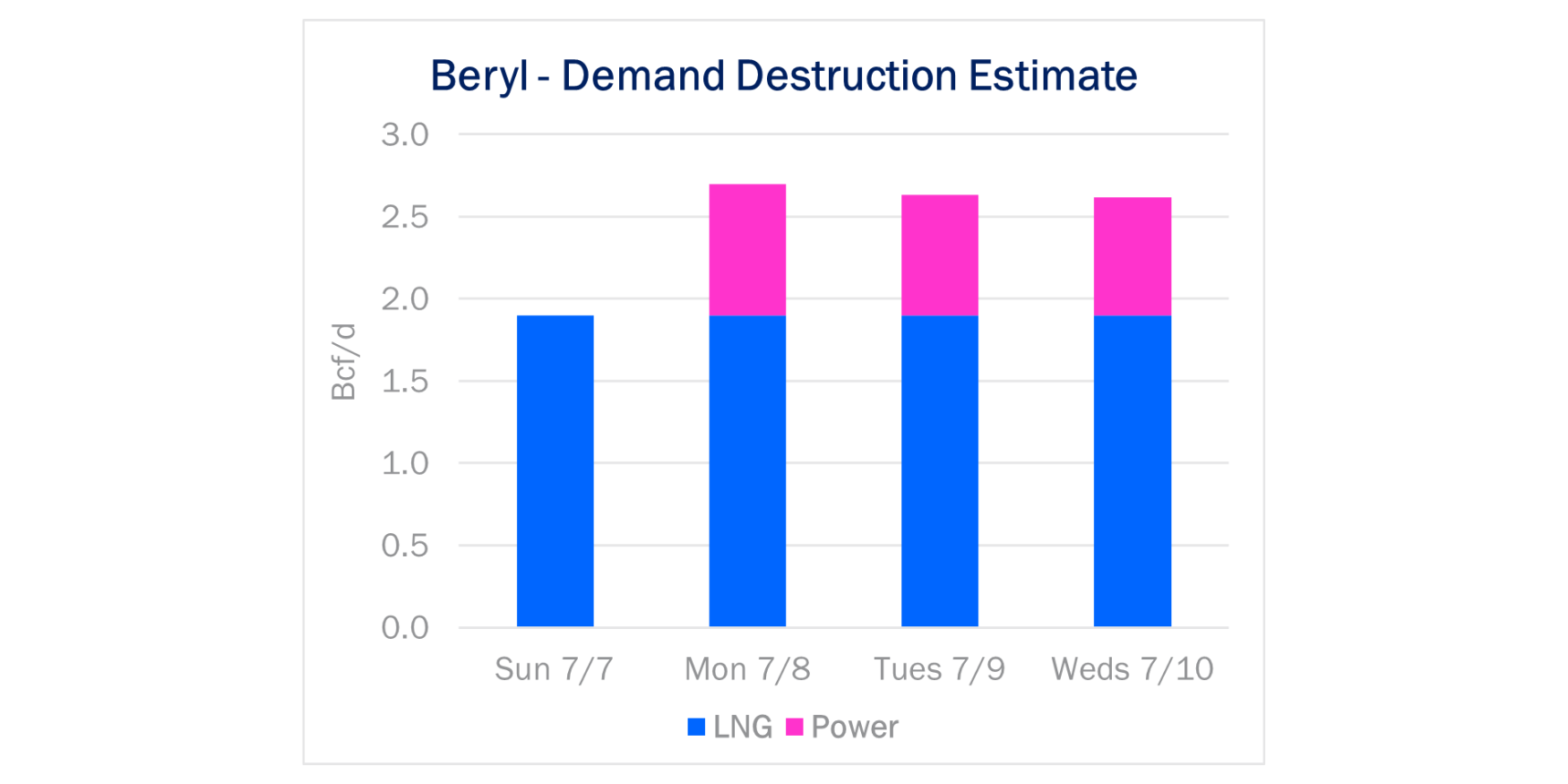

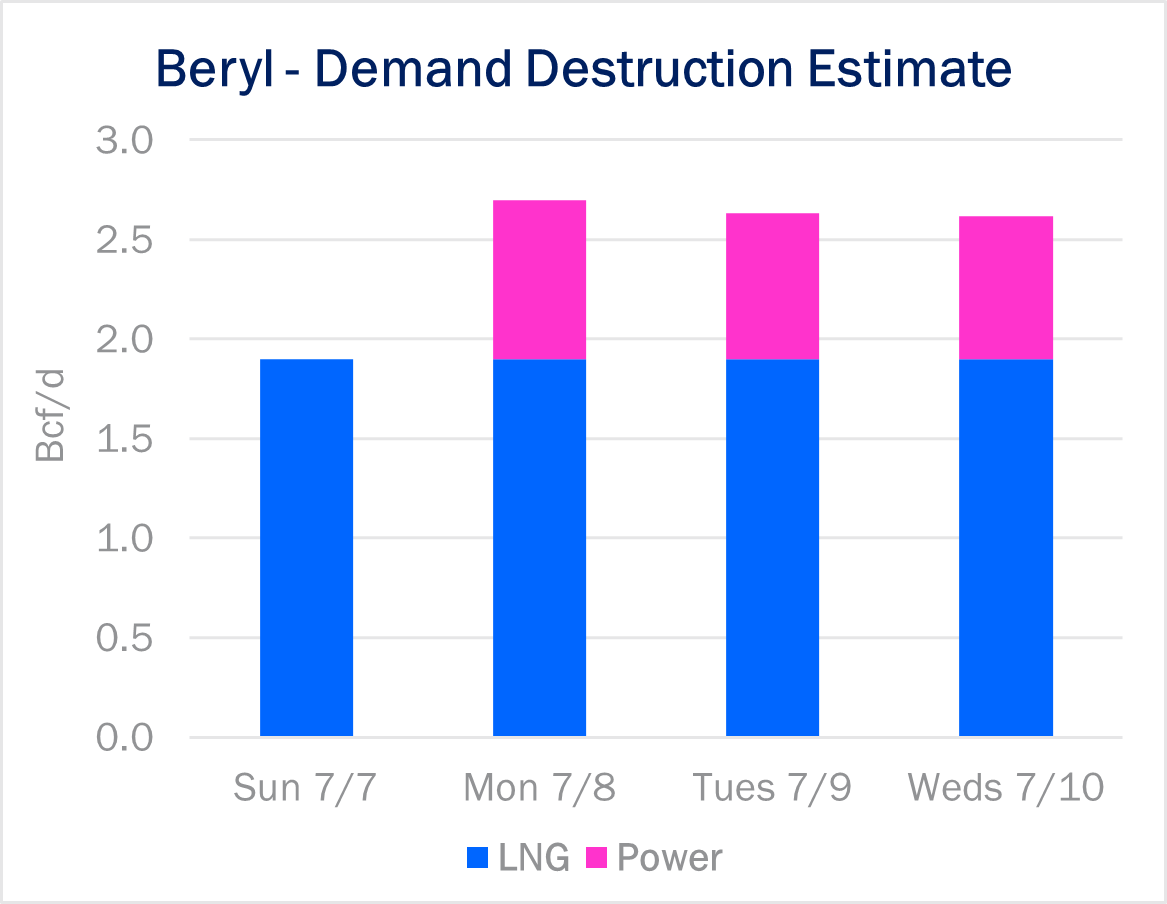

East Daley estimates Beryl, now a tropical storm, has cut natural gas demand by a total of ~9.8 Bcf through Wednesday (see figure). Freeport LNG shut down its facility on Sunday ahead of the storm, and nominations have remained at zero since then. The facility normally receives about 1.9 Bcf/d of natural gas.

Lost gas-fired power burn also has been significant, with 2.3 million people without power on Tuesday and 1.7 million residents still without power on Wednesday (July 10). The Electric Reliability Council of Texas (ERCOT) reported 19.5 GW of outages on Monday, 18 GW of outages on Tuesday, and ~17.5 GW of outages as of Wednesday. System-wide demand was well below day-ahead forecasts for all three days.

About 50% of the generation fleet in Texas is fired by gas. Assuming the outages uniformly impaired power facilities of all generator types, we see about 0.8 Bcf/d of lost demand starting Monday.

Infrastructure – Whitewater Midstream’s Matterhorn Express Pipeline could begin service as early as this month. East Daley forecasts ~500 MMcf/d of linefill volumes in July, ramping to the full 2.5 Bcf/d in September ‘24.

Permian flows have saturated the South Texas market in recent years, a dynamic we break down in the Houston Ship Channel Supply & Demand Report. Pipeline capacity from the Permian Basin to South Texas increases to 12 Bcf/d in 3Q24 after Matterhorn comes online, more than triple capacity of just 3.4 Bcf/d in early 2019.

As this new Permian supply floods into South Texas, East Daley expects to see downward pressure on Houston Ship Channel basis. Limited demand growth is set to come online in 2024, so we expect additional inbound flows from the Permian to displace inbound supply from the Carthage market.

In the Houston Ship Channel Supply & Demand Report, we reduce Carthage-to-Houston flows by 2-3 Bcf/d in 2024-28 to balance the South Texas market, indicating Houston will trade at a discount to Henry Hub. Later, we expect Carthage to provide swing supply in 2029-30 as LNG demand in South Texas comes online and additional pipeline capacity from Texas to Louisiana is available to support LNG projects at the TX/LA border.

See our Houston Ship Channel Supply & Demand Report for more information. An interactive dashboard is coming soon on Energy Data Studio – see the figure for an early peek.

Storage – Traders and analysts expect the Energy Information Administration (EIA) to report a net injection of 55 Bcf into working gas for the week ending July 5. For the same week last year, the EIA reported a 57 Bcf injection. Inventories would rise to 3,189 Bcf, in line with East Daley’s outlook in the monthly Macro Supply & Demand Forecast.

The surplus to the 5-year average would fall by just 2 Bcf to 494 Bcf based on market estimates, while the Y-o-Y surplus would also slip by 2 Bcf to 273 Bcf. Both measures have fallen by over 30 Bcf the past two weeks.

Through the end of July, we expect the injection rate to slow as heat returns in the 6- to 15-day forecast (predominantly on the East and West coasts) and production remains relatively flat. We expect production to average just 100 Bcf/d in July before showing any significant uptick in 4Q24.

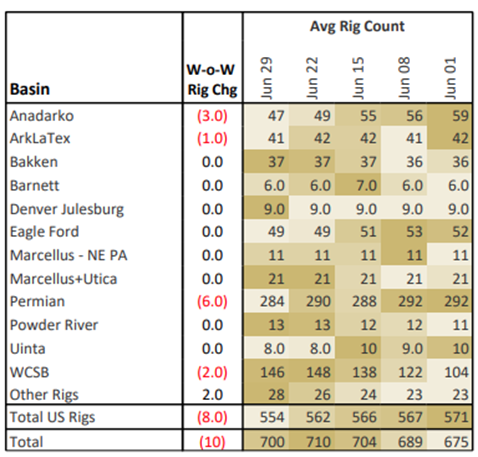

Rigs – US rigs are down 8 W-o-W to bring the total count to 554. The Anadarko Basin is down 3 rigs while the ArkLaTex is down 1 rig for the June 29 week. The Permian Basin is showing a decline of 6 rigs, but this is likely due to rig moves and should recover next week.

On the midstream side, Enterprise Products (EPD) is down 4 rigs total with reductions on its Navitas and Delaware systems. Targa Resources (TRGP) is down 2 rigs net with losses on its West Texas system. Energy Transfer (ET) is up 2 rigs total with additions on its Midland and Delaware systems.

East Daley’s weekly Midstream Activity Tracker monitors rig activity by basin and by gathering and processing (G&P) system to better understand midstream impacts. We allocate rigs and monitor flows through 150+ public and privately owned G&P systems in every North American basin. Reach out for more information on the Midstream Activity Tracker.