Executive Summary:

Infrastructure: Energy Transfer reached FID on an expansion of its Transwestern Pipeline to serve growing demand in the Southwest.

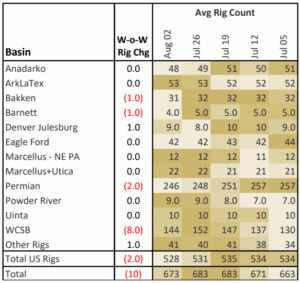

Rigs: The US rig count dropped by 3 from 531 to 528 for the week of Aug. 2.

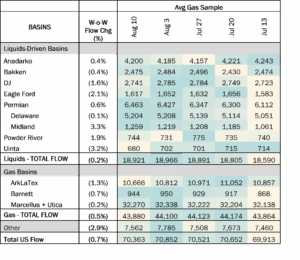

Flows: US natural gas volumes averaged 70.9 Bcf/d in pipeline samples for the week ending August 3, up 0.5% W-o-W.

Storage: Traders expect the EIA to report a 52 Bcf injection for the week ending Aug. 8.

Infrastructure:

Energy Transfer (ET) reached a final investment decision (FID) on an expansion of its Transwestern Pipeline to serve growing natural gas demand in the Southwest region. The project will boost market access for Permian Basin supply and could sideline a competing pipeline proposal by Kinder Morgan (KMI).

ET announced the decision last Wednesday (Aug. 6). The $5.3B project, called the Desert Southwest expansion, will add 516 miles of 42-inch pipe from Texas to central Arizona and have a capacity of 1.5 Bcf/d. ET expects to bring the project into service by 4Q29.

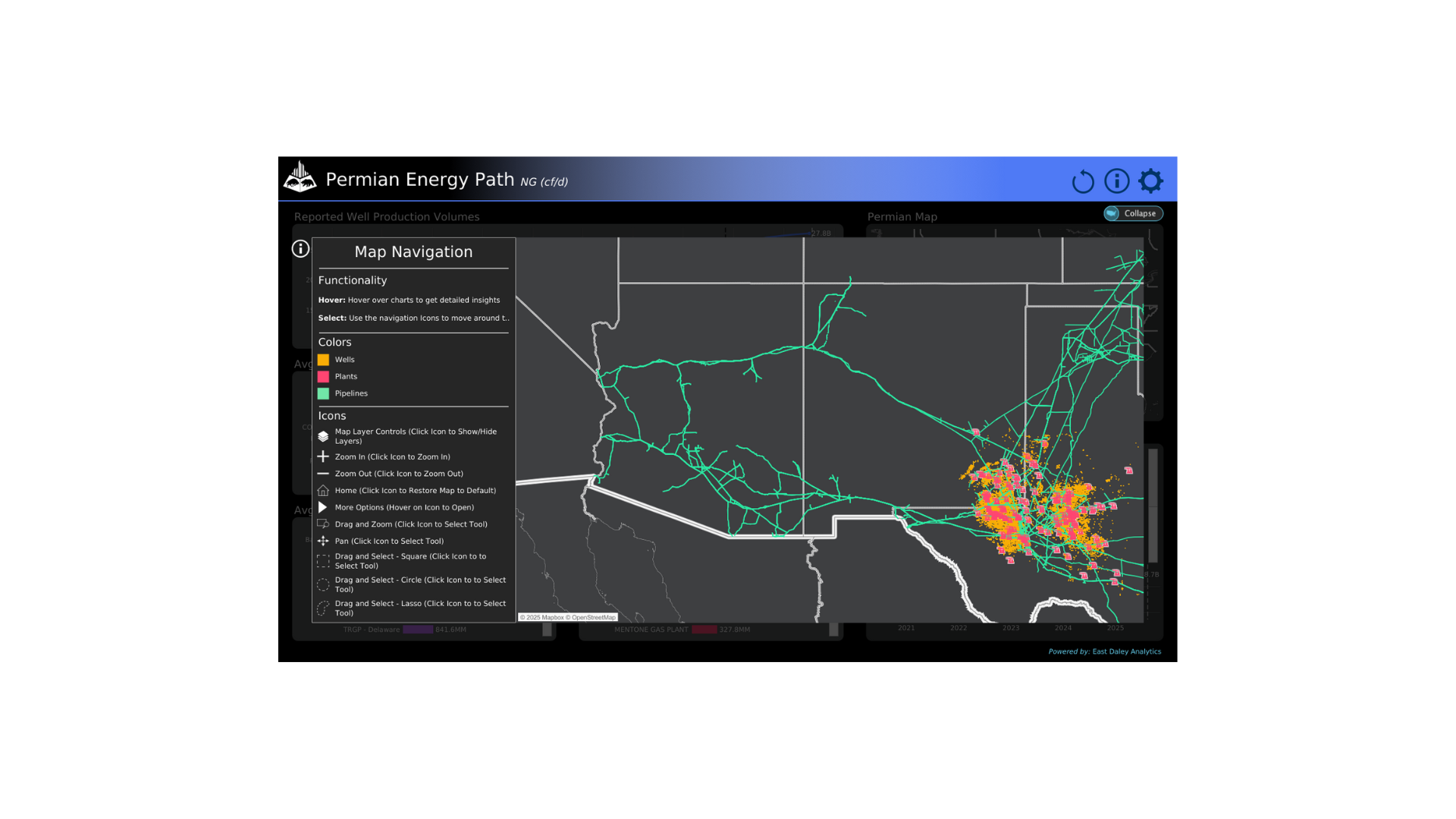

Transwestern currently extends from the Permian through northern New Mexico and Arizona and terminates at the Southern California border (see map from East Daley Analytics’ new Permian Energy Path dashboard in Energy Data Studio). The pipeline receives gas from the Permian and San Juan basins and delivers most of its volumes to central Arizona and into Sempra Energy’s (SRE) SoCal intrastate system. Though not explicitly stated, the project appears to be a new lateral that would serve as a southern mainline for Transwestern that directly connects the Permian to the Tucson/Phoenix area, bypassing San Juan production.

ET took FID despite holding no open season for Desert Southwest. In its press release, ET said an open season would be conducted later in 3Q25, and left open the possibility that the pipeline could be expanded to accommodate demand beyond the 1.5 Bcf/d already declared.

Desert Southwest will help address a supply shortage East Daley Analytics has flagged in the Southwest. The West Coast Supply & Demand Report sees growing demand for data center development and the expected startup of ECA LNG on Mexico’s Pacific coast driving a regional imbalance of over 1.6 Bcf/d by YE2030.

The expansion would also add egress for Permian shippers, providing additional capacity that could increase competition for molecules and support higher Waha prices. East Daley has predicted changes ahead for the Permian as the gas market leans more heavily on the basin’s supply, and the ET project will support this transition.

Producers in the San Juan could also benefit. Additional capacity could pull Permian flows off the existing Transwestern mainline, alleviating constraints that would open more capacity for San Juan molecules to move on the pipeline. Stronger Waha prices would also improve San Juan spreads, allowing producers in the San Juan more opportunity to compete. However, if Permian production builds into the additional capacity quickly, the San Juan could lose any edge it had when the project enters service.

Desert Southwest could prove a missed opportunity for KMI. The company has previously proposed its Bullet pipeline, which would follow a similar route to supply gas from the Permian to central Arizona, but has released little information on the project. A deck from KMI’s June customer meeting shows a similar greenfield pipeline called Copper State, but there is no mention of whether that pipeline is the same as Bullet or indeed is even one of KMI’s prospective projects.

For a closer look at the Southwest market, see East Daley’s West Coast Supply & Demand Report.

Rigs:

Total US rigs dropped by 3 from 531 to 528 for the week of Aug. 2. The Bakken lost 1 rig, the Barnett lost 1 rig, and the Permian lost 2 rigs W-o-W. This was partially offset by a 1 rig gain in the Denver-Julesburg. The WCSB lost 8 rigs W-o-W.

At the company level, Targa gained 5 rigs and Energy Transfer gained 2 rigs on their G&P systems. MPLX lost 2 rigs, KNTK lost 2 rigs, and PBA lost 4 rigs W-o-W. Notable system-level changes include PSX–DCP Delaware’s gain of 4 rigs, TRGP–West Texas’s gain of 3 rigs, KNTK–Raptor’s loss of 2 rigs, and PBA – Cutbank’s loss of 2 rigs W-o-W.

See East Daley’s weekly Rig Activity Tracker for more information on rigs by basin and company.

Flows:

US natural gas volumes averaged 70.4 Bcf/d in pipeline samples for the week ending August 10, down 0.7% W-o-W from 70.8 Bcf/d.

Gas basin samples declined 0.5% W-o-W to 43.9 Bcf/d. The Haynesville sample declined 1.3% to 10.7 Bcf/d, and the Marcellus+Utica slid 0.2% to 32.3 Bcf/d.

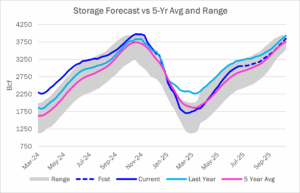

Storage:

Traders and analysts expect the Energy Information Administration (EIA) to report a 52 Bcf injection for the week ending Aug. 8. A 52 Bcf injection would increase the surplus to the five-year average by 19 Bcf to 192 Bcf. The storage deficit to last year would drop 54 Bcf to 83 Bcf.

Storage inventories could pass 3.2 Tcf by the end of August. Last year the market hit that milestone early on July 11, owing to a significant overhang exiting the mild winter. The five-year average is for storage to reach 3.2 Tcf during the week ending September 12, so the injection pace this year is about two weeks ahead of schedule but not nearly as outrageous as 2024.

Prices reflect this reality, with cash waffling around $3.00/MMBtu for most of the month. The prompt-month contract has taken some hits however, as traders worry that oversupply conditions will persist through the fall shoulder season. Prompt fell below $2.80 on Tuesday (Aug. 12), marking a 10% decline since the beginning of the month. There is still some time for futures to reconcile with cash before the end of the month. However, outside of a short squeeze, the fundamentals point to a finish slightly below $3.00.

See East Daley Analytics’ latest Macro Supply & Demand Report for more analysis on the storage outlook.

Calendar:

Subscribe to East Daley’s The Daley Note (TDN) for midstream insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.