There is materially more propane supply hitting the market than most participants are pricing in. The latest monthly Energy Information Administration (EIA) data shows US propane production from gas plants rebounded 111 Mb/d in February after January freeze-offs temporarily curtailed output.

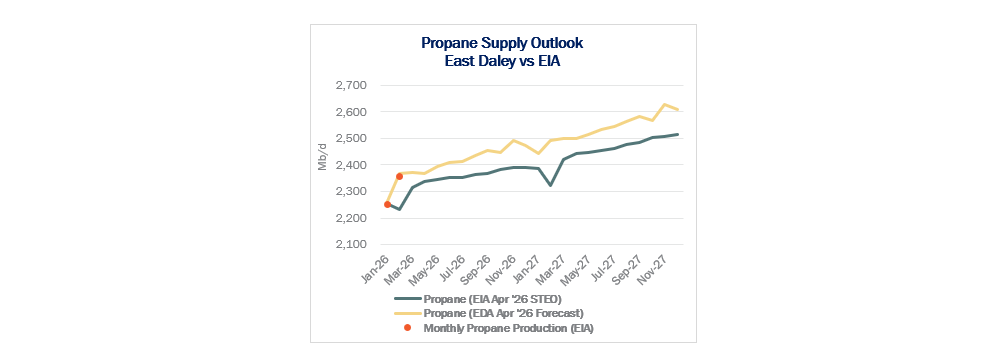

East Daley Analytics had anticipated this recovery in our April ’26 Purity Product Forecast, based on the production rebound in prior storms and real-time gas pipeline flows we monitor. The realized February number trailed our forecast by just 12 Mb/d but exceeded EIA’s forecast in the April ’26 Short-Term Energy Outlook (STEO) by a sizable 123 Mb/d.

East Daley Analytics had anticipated this recovery in our April ’26 Purity Product Forecast, based on the production rebound in prior storms and real-time gas pipeline flows we monitor. The realized February number trailed our forecast by just 12 Mb/d but exceeded EIA’s forecast in the April ’26 Short-Term Energy Outlook (STEO) by a sizable 123 Mb/d.

The recovery was overwhelmingly driven by the Permian Basin. The February data showed record propane production out of EIA’s Texas Inland subregion, which includes the Permian. That matters because the underlying drivers, associated gas growth and rising NGL yields (measured as gallons per Mcf), remain firmly intact. This is structural supply growth.

We continue to see sustained propane production growth through 2027, led by expanding Permian gas production and the basin’s increasingly liquids-rich production profile. Our April forecast averages 66 Mb/d above EIA’s in 2026 and is 87 Mb/d higher in 2027, based on the agency’s April ’26 STEO (see figure).

The market implication is straightforward: The US propane market will need to clear significantly more barrels than consensus currently expects. That raises the stakes for export demand growth, dock utilization, and export economics for global propane dehydration (PDH) units.

See East Daley’s NGL Hub Model and Purity Product Forecast for more information. Market participants should prepare for a longer-duration supply push and continued pressure to expand exports, rather than expecting the domestic market alone to absorb incremental barrels. – Julian Renton.

Join East Daley’s May Production Stream Webinar

East Daley Analytics will host our monthly Production Stream webinar on Wednesday, May 27. Midstream infrastructure is becoming the defining bottleneck in North American energy markets — and the value of infrastructure is poised to rise significantly in the years ahead:

- US natural gas pipelines are operating at high utilization rates, making firm transportation increasingly strategic and valuable.

- Emerging demand like data centers and LNG export facilities require reliable baseload supply.

- Combined, we expect these sectors to drive more than 20 Bcf/d of long-term natural gas demand by 2030.

- Crude pipeline systems are facing similar constraints as producers push utilization limits to move oil to the coast.

- Fractionation bottlenecks in the Permian continue to tighten NGL logistics, raising critical questions about how the industry will respond.

Our analysts will break down emerging infrastructure constraints, and their implications for the future of midstream energy and new investment opportunities. Join our Production Stream webinar on Wednesday, May 27.

Our analysts will break down emerging infrastructure constraints, and their implications for the future of midstream energy and new investment opportunities. Join our Production Stream webinar on Wednesday, May 27.

Download Part II of East Daley’s Permian Basin White Paper Series

The Permian Basin’s next big buildout is already taking shape, but this time the driver isn’t crude oil. In The Permian Basin at a Crossroads: Why This Pipeline Boom is Different, East Daley Analytics’ latest white paper reveals how gas demand from AI data centers, utilities and LNG exports is rewriting the midstream playbook in the leading US basin. Over 10 Bcf/d of new capacity and $12 billion in investments are reshaping flows, turning the Permian into a gas powerhouse even as rigs decline. Read Part II: Why This Pipeline Boom is Different

The Daley Note

Subscribe to The Daley Note for energy insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices and EDA research likely to affect markets in the short term.

[/vc_column_text][/vc_column][/vc_row]