Exec Summary

Market Movers: Kinetik’s sale of its 27.5% equity interest in the EPIC Crude Pipeline could open the door to more divestitures.

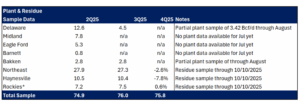

Estimated Quarterly Volumes: The Northeast meter point sample stepped down 2.6% from 3Q25.

Calendar:

Market Movers:

Kinetik’s (KNTK) recent sale of its 27.5% equity interest in the EPIC Crude Pipeline could open the door to more divestitures. The company’s two crude oil gathering systems are more attractive candidates following the $500MM EPIC deal with Plains All American (PAA).

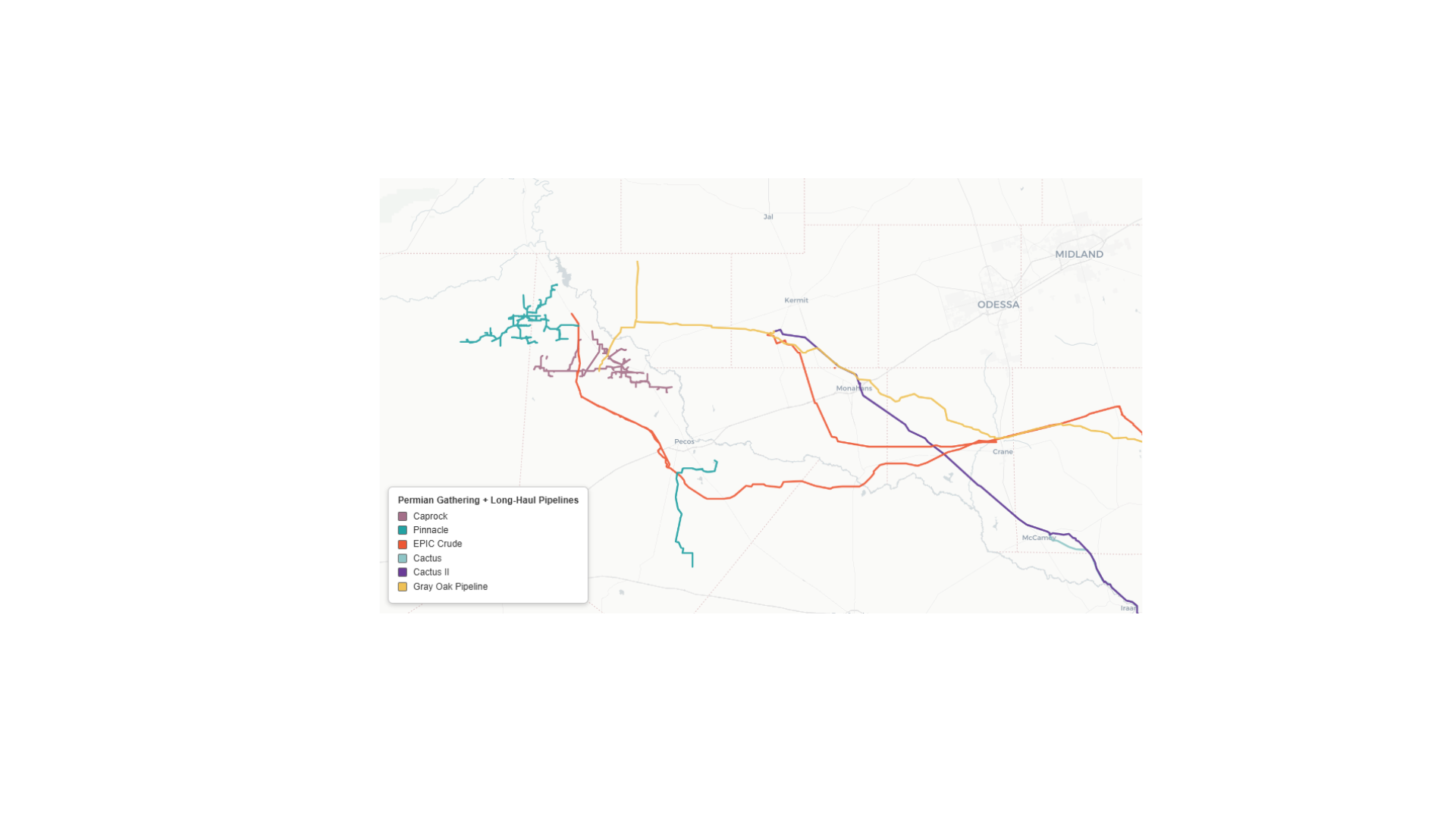

Kinetik owns the Caprock and Pinnacle crude gathering systems in the Delaware Basin, primarily based in Reeves County, TX. The assets together comprise ~220 miles of gathering pipeline and ~90 Mb of storage at the Stampede (Caprock) and Sierra Grande (Pinnacle) terminals.

The Caprock and Pinnacle systems provide upstream connectivity into EPIC and several key long-haul crude oil pipes, including Gray Oak and Cactus I/II (see map below). In the KNTK Financial Blueprint, East Daley Analytics estimates total 2025 EBITDA of ~$26MM for the two systems (~$14MM from Caprock and ~$12MM from Pinnacle). We forecast flat asset earnings over the next few years.

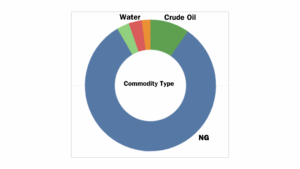

The “Peer Comparison Tool” in Energy Data Studio highlights that KNTK’s portfolio is overwhelmingly weighted toward natural gas, representing ~86% of total EBITDA (see figure below). The Caprock and Pinnacle systems account for just ~2% of Kinetik’s total EBITDA. Moreover, the EPIC sale ends KNTK’s control of downstream oil assets, making the two systems less compelling components of its portfolio.

Management suggested this strategy in the EPIC announcement, emphasizing the redeployment of proceeds from non-core asset sales into growth projects and shareholder returns. KNTK is heavily invested in its Permian gas strategy, including the impending start of the Kings Landing processing complex and construction of the ECCC Pipeline.

Given their location and tie-ins, Caprock and Pinnacle should see solid buyer interest. Western Midstream (WES), Plains Oryx (PAA JV with Oryx Midstream) and Energy Transfer (ET) are other large operators in the Delaware/Reeves County area who could benefit from annexing the assets.

Plains in particular may have interest. PAA has been active in M&A recently, including the purchase of the EPIC equity stake, and the assets align with its broader “wellhead-to-water” strategy. Plains also has a track record of acquiring gathering systems, most recently purchasing Ironwood Midstream Energy. Acquiring Pinnacle and Caprock would further this vertical integration, complementing Plains’ ownership stakes in the Cactus (100%), Cactus II (70%), Eagle Ford JV (50%) and EPIC (55%) pipelines.

Bottom Line: A Caprock and Pinnacle sale would further Kinetik’s pivot toward natural gas while providing strategic buyers with valuable crude gathering infrastructure in the Delaware Basin.

Estimated Quarterly Volumes:

Notes: 3Q25 is expressed as Q-o-Q growth from 2Q25. Rockies is the sum of Big Horn, DJ, Green River, Piceance, Powder River, San Juan, Uinta and Wind River.

- The Northeast meter point sample stepped down 2.6% from 3Q25. The WMB – Bradford Supply Hub is down 1% and the MPLX – Sherwood system is down 3.6%. Expand Energy is the largest producer behind the WMB system, while Antero Resources is the top producer on the Sherwood system from 3Q25.

- The Haynesville sample is down 7.8% from 3Q25. Given that we currently have just 10 days of data, we anticipate that the results will stabilize as additional data is collected. The KMI – KinderHawk system is up 23% Q-o-Q, with Comstock the largest producer behind the system.

Calendar: