Exec Summary

Market Movers: Enterprise could realize upside by selling its Jonah system in the Rockies

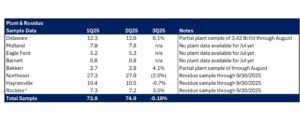

Estimated Quarterly Volumes:The Haynesville meter point sample ended the quarter down 0.7% from 2Q25.

Calendar:

Market Movers:

Enterprise Products (EPD) plans major investments in the Permian Basin, yet its assets in the Rockies are underused. EPD prioritizes scale in markets it leads, from NGLs and Permian G&P to Gulf Coast exports. We see an opportunity for the company to prune its portfolio in a region outside its core focus.

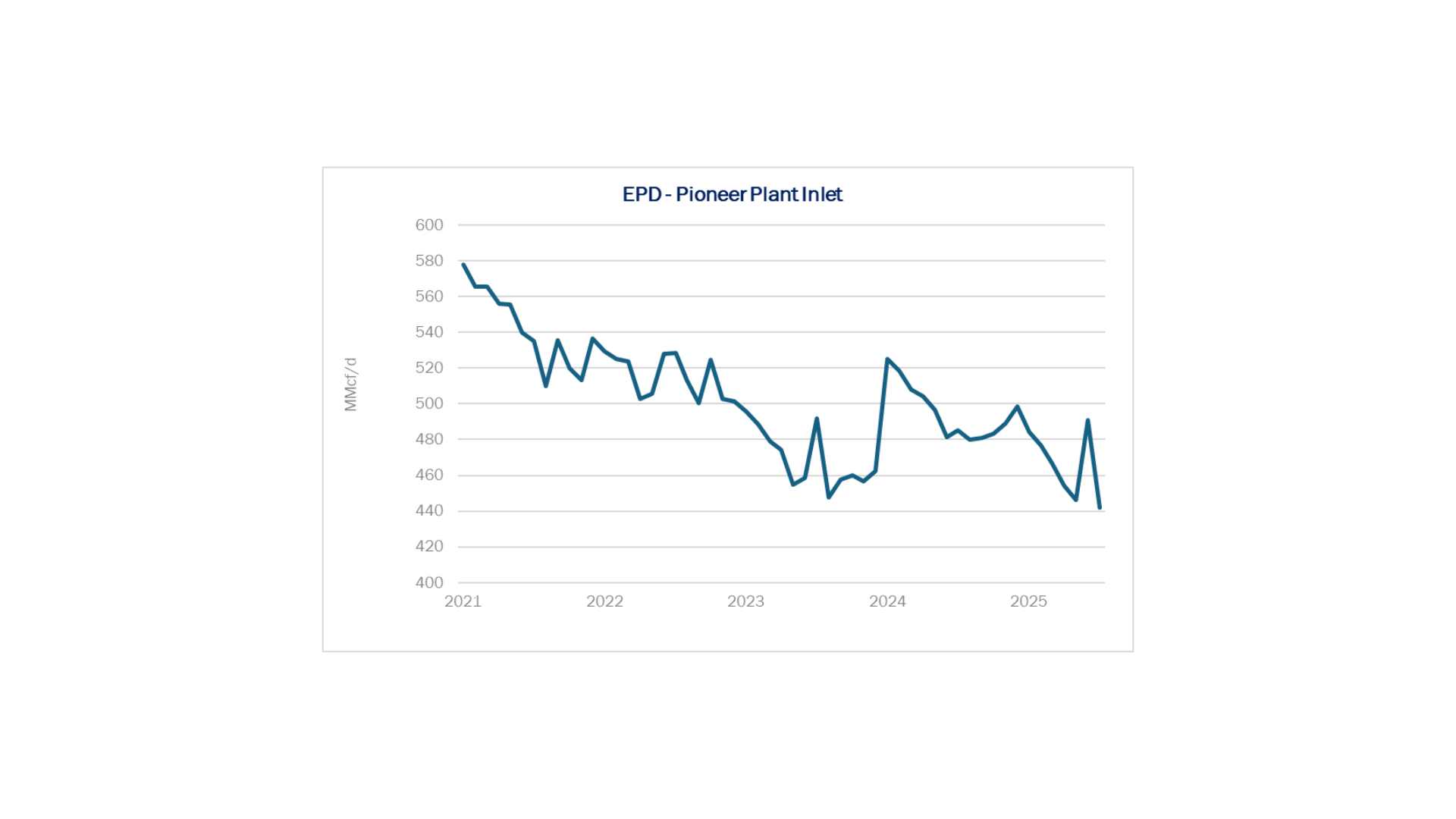

The Jonah gathering system collects gas from the Jonah–Pinedale formation in the Green River Basin and feeds EPD’s Pioneer plant near Opal, WY. The system also delivers gas to Williams’ (WMB) Opal plant. East Daley Analytics expects modest growth from the Green River Basin as West Coast demand expands. WMB is also adding westbound capacity into Opal via the Overthrust Westbound Compression expansion, creating more demand pull to the hub.

Pioneer plant inlets have declined from 578 MMcf/d in Jan ’21 to 442 MMcf/d in July ’25, according to plant data in East Daley’s Energy Data Studio (see figure below). Residue volumes have also trended lower over this period (from 541 MMcf/d to 343 MMcf/d), and we model EBITDA for the Jonah system to hold flat at ~$14–15MM/quarter. Given these trends, EPD could maximize the value of the Jonah and Pioneer assets by selling them as a combined Opal-area package.

In our view, the Jonah/Pioneer assets no longer fit in EPD’s core playbook. 1) The company is investing heavily in Permian G&P, including the Leonidas, Orion and Athena plants in the Midland, plus NGL assets. The Rockies are not an area of focus. 2) The assets’ EBITDA contribution is small relative to Enterprise’s dominant NGL platform. 3) NGLs are relevant to EPD’s full-chain NGL strategy, but volumes from Opal primarily move over the Overland Pass Pipeline owned by WMB and ONEOK (OKE). EPD could still maintain control of NGL barrels through marketing and fractionation contracts, or backfill volumes on its Gulf Coast system with faster-growing Permian throughput.

From a buyer’s perspective, a Jonah/Pioneer package would have more value for Williams. WMB also controls Opal processing and Green River G&P assets, and has made a commitment to the region through the Overthrust expansion and its $1.5B MountainWest acquisition in 2023. Acquiring a Jonah/Pioneer package would enable Williams to capture gathering margin now paid to a third party and optimize plant loadings across Opal/Pioneer. WMB could also streamline residue and NGL routing under one commercial umbrella, with NGLs moving over Overland Pass.

MPLX, which is pursuing a similar NGL wellhead-to-water strategy as Enterprise, recently provided an example of how a divestment could be structured. MPLX sold its non-core Rockies assets to Harvest Midstream for $1B, yet will retain control of the NGL volumes from the properties. EPD could pursue a similar deal to free up capital and right-size its portfolio.

Investor Takeaway: Rockies G&P is outside EPD’s focus and delivers flattish EBITDA; a sale to WMB would create more synergies and unlock asset value. That said, Enterprise is disciplined, and a divestment must beat returns from its focus on the Permian and NGL value chain.

Estimated Quarterly Volumes:

Notes: 3Q25 is expressed as Q-o-Q growth from 2Q25. Rockies is the sum of Big Horn, DJ, Green River, Piceance, Powder River, San Juan, Uinta and Wind River.

- The Haynesville meter point sample ended the quarter down 0.7% from 2Q25. The sample is down from new volumes flowing on the LEG and NG3 pipelines. The DTM – Blue Union system is up 19.4% and the KMI – KinderHawk system is up 21.2% from 2Q25.

- The Rockies meter point sample ended the quarter up 3.5% from 2Q25. The PSX – DCP Denver Julesburg system is up 2.4% from 2Q25.

Calendar: