Executive Summary:

Infrastructure: Enterprise Products reported robust flows on the new Bahia pipeline, raising the ante in the fight for Permian NGL barrels.

Exports: US NGL exports saw a solid lift for the week ending Feb. 6, posting a 15.9% W-o-W gain.

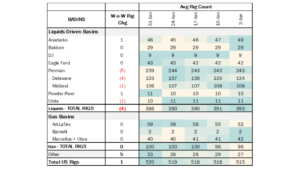

Rigs: The total US rig count increased during the week of Jan. 31 from 519 to 520. Liquids-driven basins lost 4 rigs W-o-W, from 390 to 386.

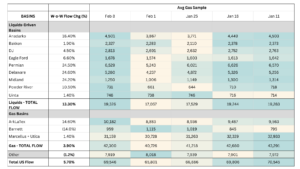

Flows: US natural gas volumes in pipeline samples bounced back for the week ending Feb. 8, up 5.7% to 69.5 Bcf/d.

Calendar:

Infrastructure:

Enterprise Products (EPD) wasted no time putting its new Bahia pipeline to use, reporting robust flows in its 4Q25 earnings. Early Bahia utilization meaningfully increases confidence in EPD’s 2026–27 growth outlook while raising competitive risk across the Permian NGL network.

Enterprise disclosed that Bahia and Shin Oak are running at ~80% utilization out of the Permian Basin, or roughly 960 Mb/d, shortly after Bahia entered service in December. In a competitive takeaway environment, this early fill materially de-risks EPD’s near-term EBITDA growth and supports the larger step-change expected in 2026–27 as downstream assets scale.

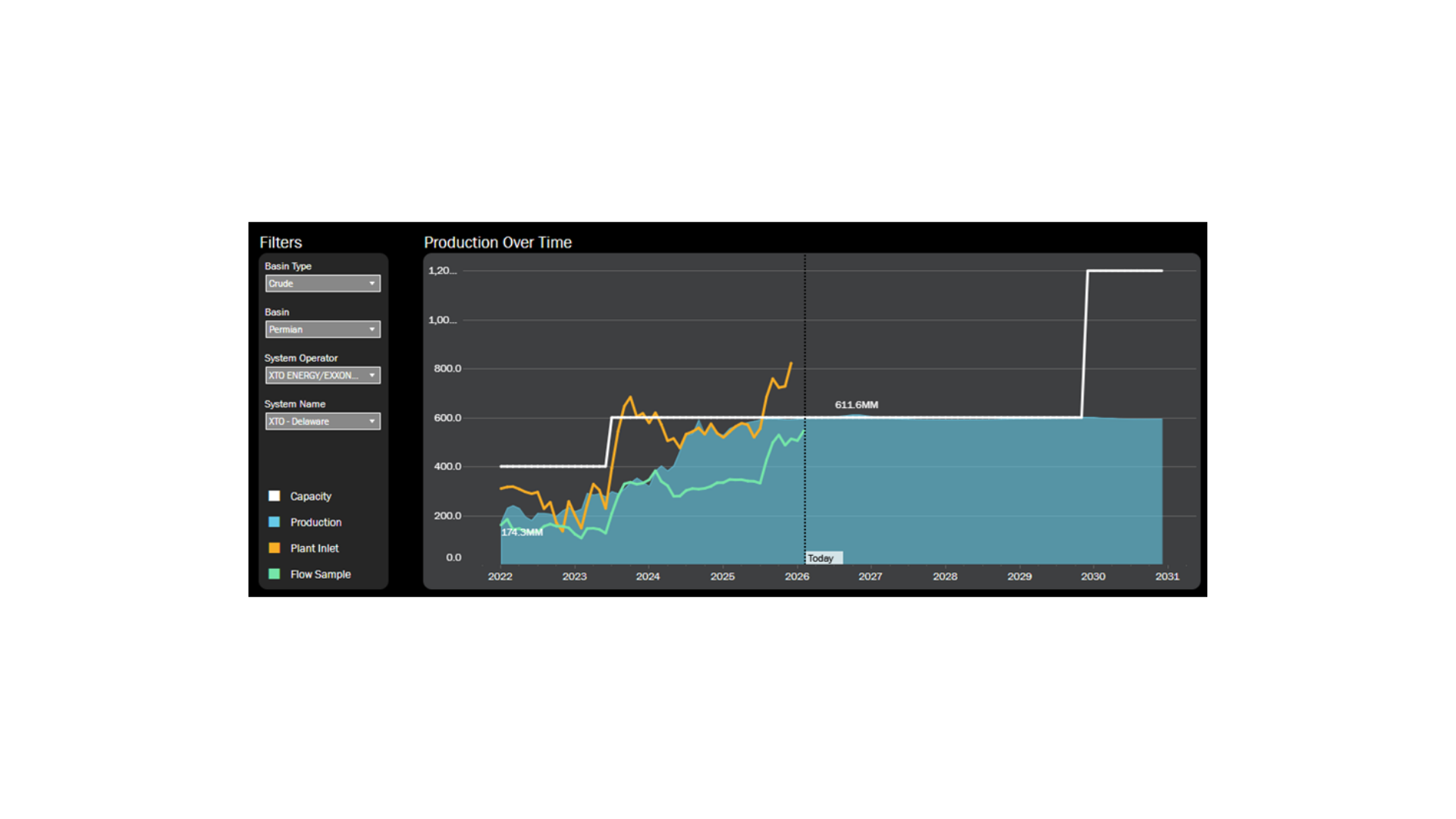

The composition of those volumes matters. ExxonMobil (XOM) provides long-cycle durability following its joint interest acquisition in Bahia, adding exposure to one of the fastest-growing producers in the Delaware Basin. The figure below, taken from the “G&P Tools” dashboard in East Daley Analytics’ Energy Data Studio, shows plant inlet and flow sample volumes on Exxon’s Delaware G&P system. East Daley’s G&P tools indicate Occidental (OXY) is most likely the other anchor shipper. Together, XOM and OXY pair balance-sheet stability with growth velocity, an advantaged mix for early utilization.

Rising gas-to-oil ratios from Permian wells continue to provide a structural supply tailwind, but 4Q25 results show that commercial alignment is determining which systems capture incremental volumes first.

Importantly, higher-than-expected utilization on Enterprise’s NGL pipes implies displacement elsewhere. East Daley sees heightened downside risk to NGL pipeline volumes for Targa Resources (TRGP) and Energy Transfer (ET), as Exxon and Occidental are meaningful producers behind competing routes. To the extent those volumes are preferentially aligned with Enterprise’s integrated system, TRGP’s and ET’s pipes face incremental volume risk at the margin.

We also see elevated risk for Phillips 66’s (PSX) Delaware system, where Exxon accounts for roughly 17% of operated rigs. As Exxon consolidates NGL egress through Bahia and downstream Enterprise infrastructure, competing Delaware takeaway systems become more exposed to underutilization risk.

Bottom line: Bahia’s early success is not just additive for Enterprise, it is redistributive. Stronger alignment with Exxon and likely Occidental increases confidence in EPD’s growth targets while heightening volume risk for competing Permian and Delaware NGL systems. In the jockeying for Permian NGL volumes, EPD seems to have captured an early mover advantage that solidifies their NGL strategy soaking up crucial barrels.

Exports:

Rigs:

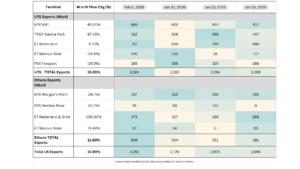

US NGL exports saw a solid lift for the week ending Feb. 6, posting a 15.9% W-o-W gain.

Modest declines at ET’s Marcus Hook and PSX’s Freeport terminals were more than offset by robust increases at other terminals, lifting total LPG exports 16.8%.

Ethane exports declined at EPD – Morgan’s Point and EPD – Neches River but were more than offset by a 100% W-o-W surge at ET’s Nederland and Orbit terminals, with additional support from ET – Marcus Hook, lifting total exports 12.8%.

Flows:

The total US rig count increased during the week of Jan. 31 from 519 to 520. Liquids-driven basins decreased by 4 rigs W-o-W, from 390 to 386.

- Permian:

- Midland (-1): BTA Oil Producers

- Delaware (-4): SM Energy, Matador Resources, Greenlake Energy

- Anadarko (+1): Continental Resources

- Powder River (+1): WRC Energy

- Uinta (-1): Koda Resources

Calendar: