The Daley Note: August 26, 2022

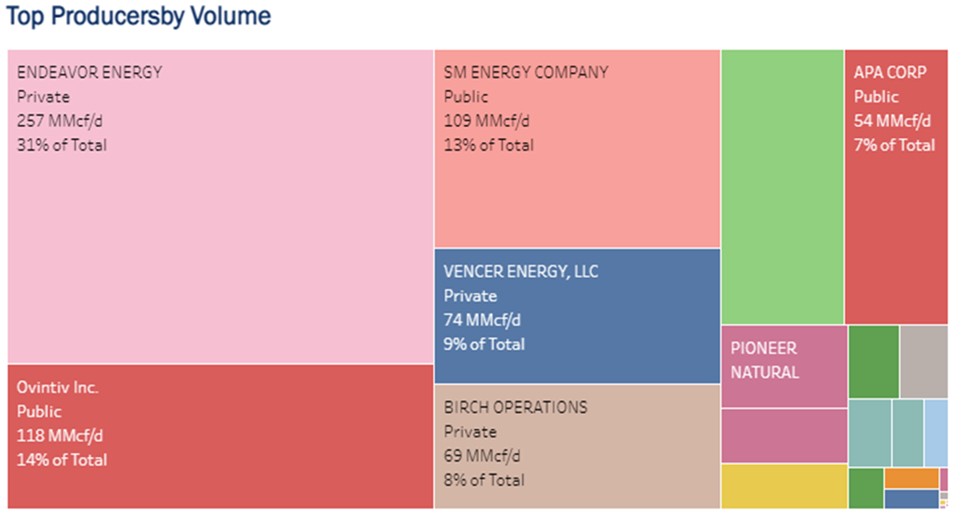

Northern Oil and Gas (NOG) has purchased a non-operated working interest position in the Midland Basin for $110 million. NOG acquired ~1,600 acres with 6 net producing wells located in Howard County, TX, the company said in a release last Wednesday (Aug. 17). The producing assets are located in Howard County, TX and are primarily operated by SM Energy (SM). The wells currently produce 1,600 Boe/d with a high oil cut (87% oil), NOG said.

NOG anticipates the bolt-on acquisition will produce around 1,800 Boe/d within a year of closing, with an additional eight net locations still undeveloped. East Daley’s G&P allocation model on Energy Data Studio shows most of SM’s operated assets in Howard County, TX are gathered on the Navitas system acquired by Enterprise Products (EPD) earlier this year. SM is a leading producer on EPD – Navitas, accounting for 13% of the total gas volumes processed by the system.

We allocate lesser SM volumes to West Texas Gas’ North Midland system and Targa’s (TRGP) Midland system. This analysis was first published for subscribers in our weekly Data Insights on Friday, August 19. Please log in to access the full Data Insights report or contact [email protected] for subscription information.

Natural Gas Watch: Offshore Sample Lower Despite Shell Ramp

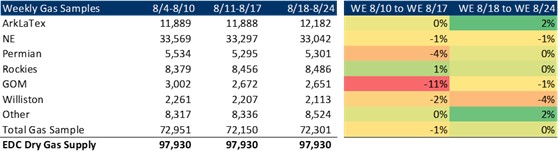

Production on Shell’s Mars, Ursa and Olympus platforms ramped back up, bringing the daily gas samples average for this week to 233 MMcf/d. However, the recovery was offset by a decrease in volumes on Discovery Gas Transmission (-12%) and Nautilus Pipeline (-18%). As a result, the Gulf of Mexico sample remains down over 11% since Aug. 10.

Freeport LNG has delayed the planned restart of the export terminal by ~1 month, which does not change our view that we will be structurally long gas by 1Q23.

Freeport LNG has delayed the planned restart of the export terminal by ~1 month, which does not change our view that we will be structurally long gas by 1Q23.

We have seen meaningful rig count additions in the Lower 48 over the last 5 months. There have been 10 rig adds in the Eagle Ford, 11 in the Rockies, and another 10 rigs in the Anadarko. We included the uptick in activity in our forecast, and this data emboldens our view of a bullish supply outlook for the rest of 2022 and 2023, relative to EIA data. We remain structurally bullish gas supply even after reducing rig activity in the back half of 2022 to account for backwardated WTI and HH price curves.

The Natural Gas Watch highlights East Daley’s high-level perspective on weekly natural gas market changes. Please click here to access a sign-up for this weekly email publication.

Dry production for the 8/18 – 8/24 week averaged 96.8 Bcf/d. We estimate August production to average 97.9 Bcf/d in our Macro Supply and Demand Forecast, with most growth coming from the Northeast, Haynesville, Permian, and Anadarko.

The Energy Information Administration (EIA) reports weekly storage +60 Bcf vs +58 Bcf consensus estimates. Inventories for the week ended August 19 total 2,579 Bcf, down 353 Bcf vs the 5-year avg. Storage is tracking with our forecast; we estimate inventories rise to 2,587 Bcf by end-August.

Subscribe to The Daley Note (TDN), “midstream insights delivered daily,” covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.

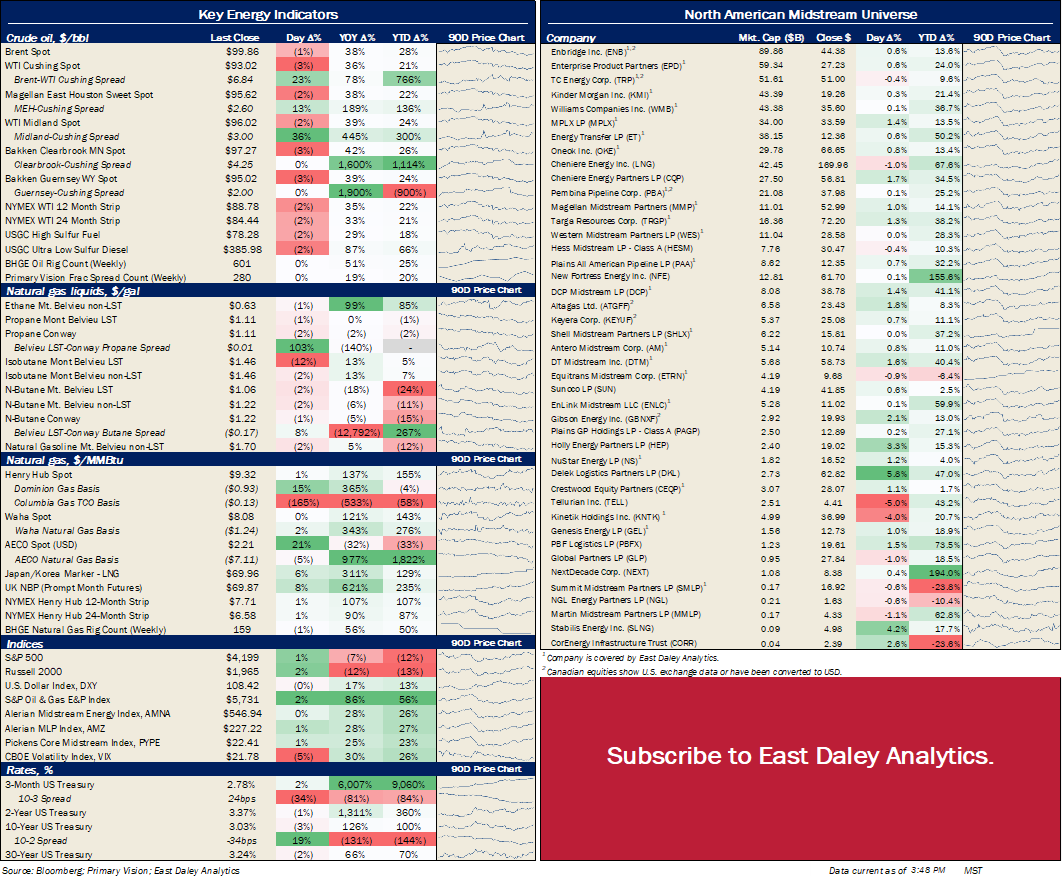

North American Energy Indicators and Equity Prices

Key Private Debt Metrics

North American Natural Gas Prices

North American Crude Oil Prices

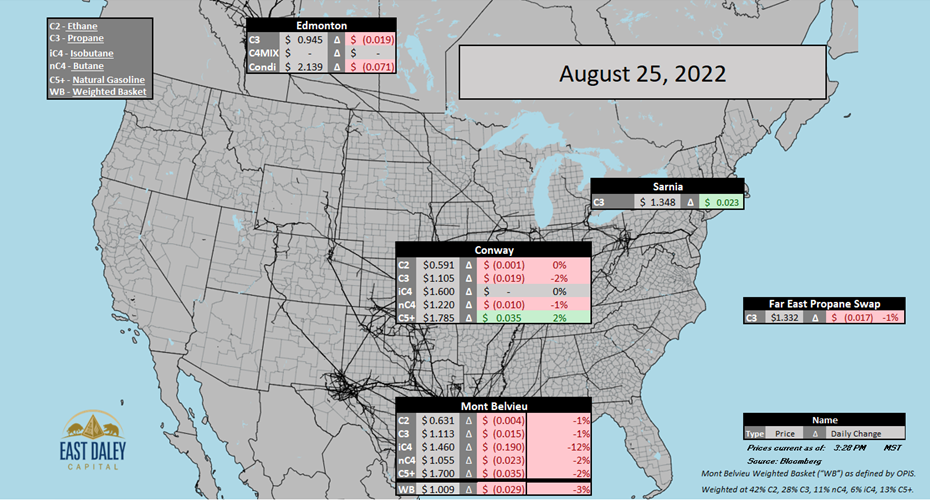

North American Natural Gas Liquids Prices

Subscribe to The Daley Note (TDN), “midstream insights delivered daily,” covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.