Market Movers: Growth is slowing in the Permian Basin, and creeping uncomfortably close to the “danger zone” of declines.

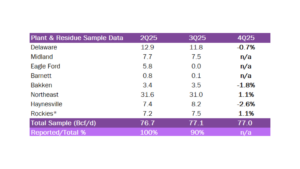

Estimated Quarterly Volumes: The Haynesville (-2.6%), Bakken (-1.8%) and Delaware (-0.7%) are trending down while the Northeast (1.1%) and Rockies (1.1%) are trending up Q-o-Q.

Calendar: EDA will be in NYC Feb. 9–12 and in Houston Feb. 25-27. Updated models will be released Feb. 13. Earnings Previews/Reviews will be released for AM, WMB, ENB, DTM, KNTK and OKE.

Market Movers:

Growth is slowing in the Permian Basin, and creeping uncomfortably close to the “danger zone” of declines.

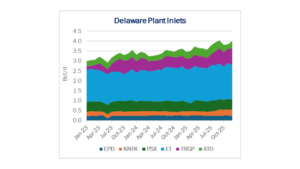

Plant inlet data and residue samples in Energy Data Studio don’t point to a collapse, but they do show a clear loss of momentum from 3Q to 4Q25. Moreover, the data reflects a rotation among G&P systems as new outperformers emerge.

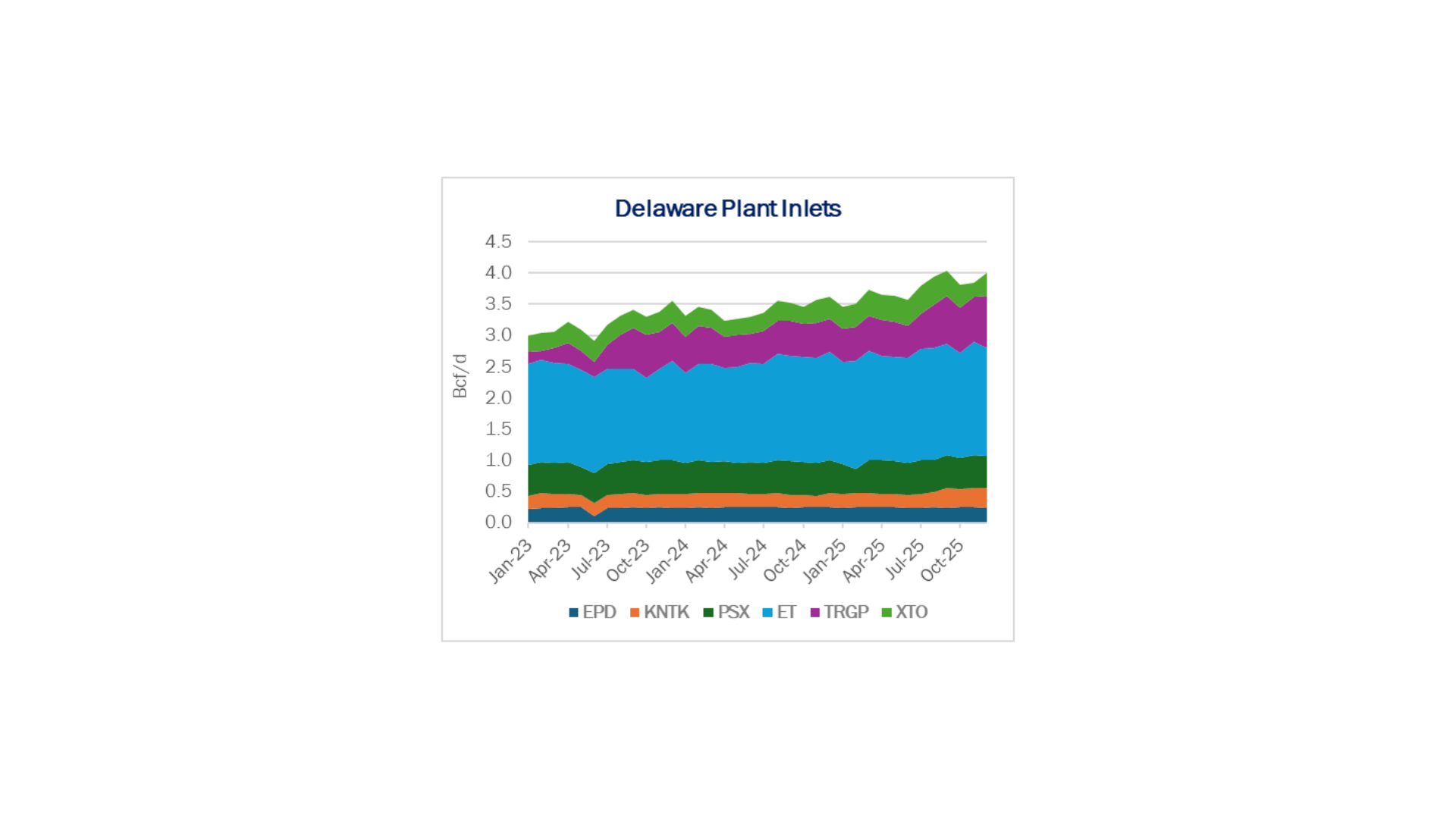

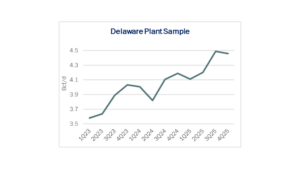

East Daley Analytics’ preliminary sample of processing plants in the Delaware Basin show inlet volumes slipped from ~4.50 Bcf/d in 3Q to ~4.47 Bcf/d in 4Q25, a 0.7% Q-o-Q decline (see figure). The decline matters because the equity debate doesn’t require a volume cliff; a slope change is enough to reset expectations, especially with a softer WTI forward curve forcing more disciplined behavior among operators.

Data continues to trickle in for Permian plants, so our sample is only an early view of 4Q25 results. And while volumes overall have been relatively flat, it hasn’t been a uniform basin move. Our survey so far shows sequential softness among several market leaders, including Energy Transfer (ET) and Targa Resources (TRGP). The plant data shows pockets of downside risk emerging in some corridors, a red flag that investors haven’t had to consider for a long time in the Permian.

Meanwhile, some assets are thriving. Kinetik’s (KNTK) Kings Landing and Durango systems, and the XTO Cowboy plant stand out. For midstream, earning will rise with increased volumes on those systems. The data also adds value as a read-through on producers: Activity is concentrating in the best rock and for the best-connected systems, and those gains can persist even while drilling cools in the basin.

Why 4Q25 matters: Lower oil prices appear at last to be filtering through to production. The WTI curve fell materially in the spring toward $60/bbl, and producers have responded by trimming Capex, dropping rigs, and leaning harder into returns and balance-sheet discipline.

Despite these efforts, it takes time for softer prices to impact supply. Initially, producers slow or defer completions, but they also draw down inventory of drilled but uncompleted wells (DUCs) and prioritize their best drilling prospects. This high-grading of operations makes supply more resilient in the near term.

Eventually, the investment slowdown catches up to production and growth starts to slow. The 4Q25 plant survey provides a view of the next phase in the Permian. Production flattens, and output could begin to slide if the WTI strip stays soft.

Where risk is building: ET and TRGP. Slowing growth at Targa doesn’t automatically equal a bad outcome, but it does shift the market’s focus. As inlet volumes cool, investors will pay closer attention to how effectively TRGP utilizes its assets and maintains margins through its integrated operations, from processing and pipelines to fractionation and export.

For Energy Transfer, flatter volumes amplify variability across its plants and corridors. In that setup, the key question becomes, “Where do volumes hold, and where do they leak?”

Outperformers: KNTK and XTO Cowboy

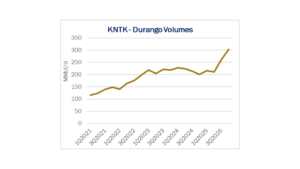

Kinetik is a name that’s bucking the “integration wins” theme in midstream. The Durango system posted a meaningful step-change in volumes beginning in 3Q25, lining up with the September startup of the Kings Landing complex. The ramp has been big: +24% from 2Q to 3Q25, followed by another 16% gain from 3Q to 4Q25. Volumes on the Durango system surged past 300 MMcf/d from 261 MMcf/d in 3Q25 (see figure below).

The key question for KNTK is whether the recent growth is durable. The gains could reflect underlying producer momentum, or commissioning/ramp effects from previously drilled wells waiting on new infrastructure. Kinetik will also have to defend its volumes on Durango from more integrated competitors as the basin flattens.

The Cowboy plant is another standout, with inlet volumes climbing from ~665 MMcf/d in 3Q25 to ~757 MMcf/d in 4Q25 (+13.8% Q-o-Q). The growth is good news both for midstream and confirm ExxonMobil’s (XOM) strong results reported Friday (Jan. 30), reinforcing that the major is outperforming its peers in the Permian.

Bottom line: The early 4Q25 data is evidence that the Permian is transitioning from rapid growth to a more measured grind. The equity narrative is also shifting, as a slowdown is sufficient to alter market perceptions. In this evolving environment, investors are likely to favor systems that can actively defend utilization rates and margin quality, particularly those with integrated operations, and continue to attract volumes despite the sector headwinds. This dynamic will define winners in the next stage of the cycle.

East Daley will continued to update 4Q samples as new data comes in. Updated readings will be available ahead of earnings as Energy Data Studio refreshes.

Estimated Quarterly Volumes:

The Total Sample represents the flow sample and plant data accessible to EDA. The latest Q-o-Q percentage change is estimated by comparing either flow sample data Q-o-Q or plants within a basin that have continuously reported inlet volumes from the prior quarter to the current quarter. 4Q25 is expressed as Q-o-Q growth from 3Q25.

Rockies represents the aggregate of Big Horn, DJ, Green River, Piceance, Powder River, San Juan, Uinta and Wind River basins.

Haynesville: Haynesville flow sample is down 2.6% Q-o-Q. Clearfork’s Holly system is down 22.9% and William’s Louisiana Magnolia system is down 15.4% Q-o-Q. Top producers on Magnolia include Expand Energy (537 MMcf/d), GEP Haynesville II (476 MMcf/d) and Apex (262 MMcf/d).

Delaware: Delaware plant inlet data is down 0.7% Q-o-Q. XTO’s Delaware system is up 13.8% while Energy Transfers’ CEQP Sendero system is down 24.7% Q-o-Q. Top producers on Sendero include Mewbourne Oil (98 MMcf/d), Permian Resources (65 MMcf/d) and ConocoPhillips (37 MMcf/d).

Calendar: