Market Movers:

Enterprise Products has laid out an ambitious path to expand earnings over the next two years. East Daley reviews whether this path is realistic.

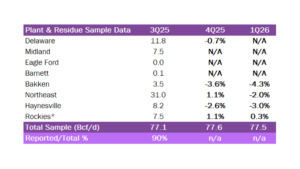

Estimated Quarterly Volumes:

3Q25 to 4Q25: The Bakken (-3.6%), Haynesville (-2.6%) and Delaware (-0.7%) are down while the Northeast (1.1%) and Rockies (1.1%) are up Q-o-Q.

4Q25 to 1Q26: The Bakken (-4.3%), Haynesville (-3.0%) and Northeast (-2.0%) are trending down while the Rockies (0.3%) is trending up Q-o-Q.

Calendar: EDA will be in Houston Feb. 25-27, Los Angeles Mar. 17-19 and Tulsa Mar. 23-26. The next financial model updates will occur Mar. 13. Earnings reviews for OKE and KNTK, along with an earnings previews for SMC will be published by Feb. 27.

Market Movers:

Enterprise Products (EPD) has laid out an ambitious path to expand earnings the next two years, backed by its extensive gathering and NGL asset footprint from the Permian Basin to the Gulf Coast. But how realistic is the story? East Daley Analytics reviews the case for rapid growth at Enterprise.

On EPD’s 4Q25 earnings call, management guided to a positive two-year outlook: modest EBITDA growth in 2026 (executives implied 3%), followed by 10% growth in 2027.

Management pointed to the Permian as the main driver behind the growth. Enterprise is building two processing plants, Mentone West 2 in the Delaware and Athena in the Midland, totaling 600 MMcf/d of capacity over 2026-27. The company is also integrating its Piñon Midstream acquisition in the Delaware Basin to boost access to growing sour gas production. To that end, EPD plans to build a fourth treating unit at Piñon’s Dark Horse facility, plus a third acid gas injection well.

NGL volumes from these plants will feed into EPD’s pipelines out of the Permian, including Seminole, Shin Oak and the new Bahia pipeline, which came online in December. Barrels will flow to the Gulf Coast and be fractionated, and the purity products then sent to end-users downstream.

Enterprise expects the export market to pick up a large share of the volumes. On the call, the company highlighted the fully contracted status of its ethane export terminals and its highly contracted LPG export docks. EPD expects to export 1,500 Mb/d of NGLs in 2027 vs ~975 Mb/d in 2025, a ~24% CAGR in the exports outlook. East Daley currently estimates this would amount to ~80% of EPD’s NGL fractionated volumes directed to exports in 2027, vs a 57% share in 2025.

The EPD growth story highlights the general macro trend we are seeing across the midstream sector: full integration from wellhead to water, with midstream companies controlling the molecule and collecting incremental fees along the value chain.

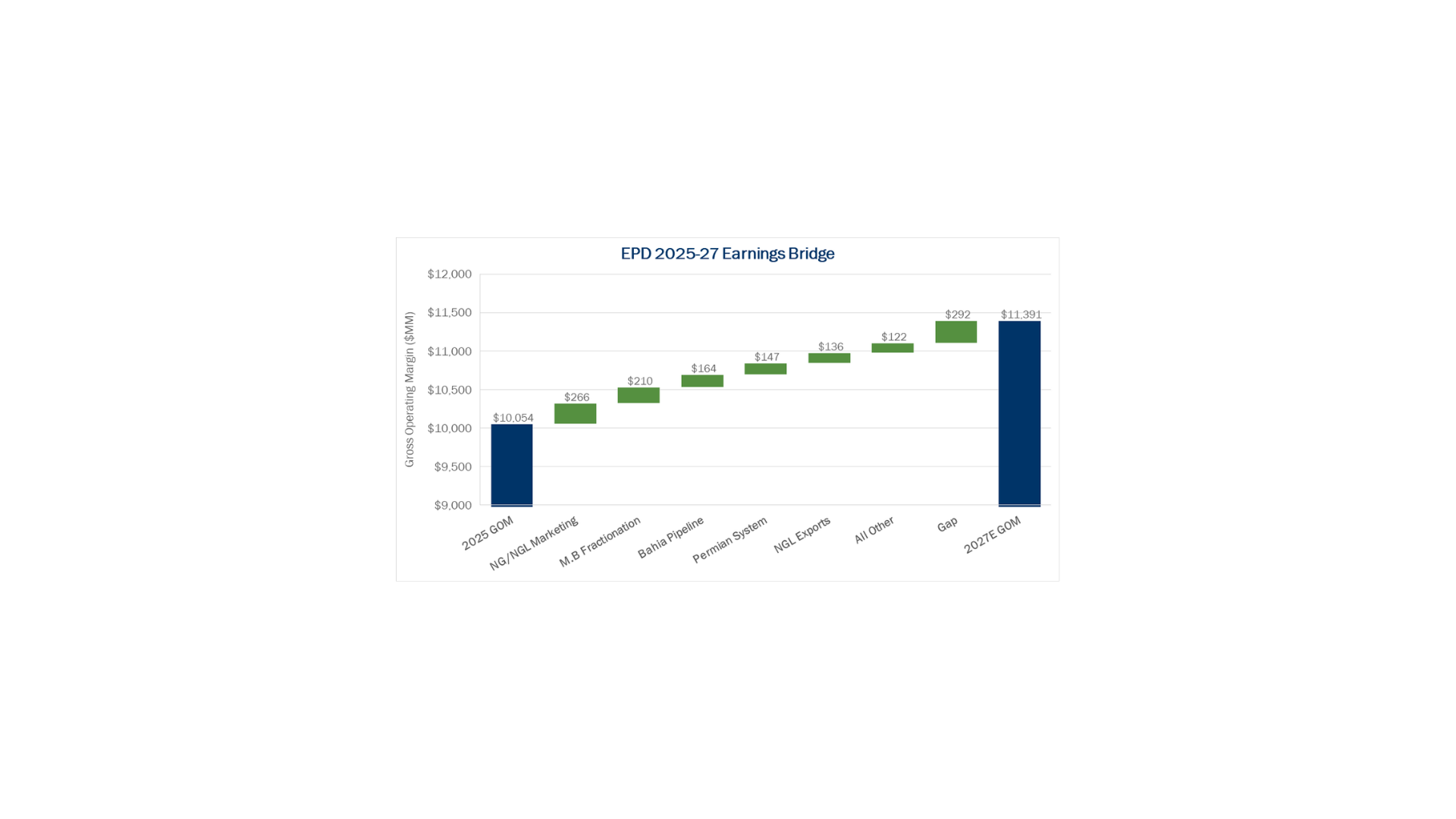

For a company the size of Enterprise, it’s an ambitious target. Can EPD really expect to grow EBITDA by 13.3% from 2025 to 2027? Based on East Daley’s latest EPD Financial Blueprint model, we believe the growth trajectory is achievable. The earnings bridge in the figure on page 1 shows the path East Daley expects EPD to follow to achieve the growth target.

The top 5 assets contributing to Enterprise’s growth showcase the Permian NGL value chain: Permian G&P systems feed Bahia, which feeds EPD’s Mont Belvieu fractionation units, which then feed NGL exports. In the latest EPD Blueprint, East Daley projects only a $292MM (~2.5%) gap between our current estimate of 2027 gross operating margin (GOM) and where EPD’s growth guidance would put the company (see figure).

There are several opportunities to close this gap. EPD could ramp volumes faster than we model on the Permian pipelines, and expansion projects could exceed our estimates. The company could also post a stronger performance from its marketing segments, or demand for NGL exports could be higher than we expect. For a deeper look into the producers backing EPD’s Permian systems, take a look in Energy Data Studio.

East Daley will fully update the financial model available for EPD within two weeks of the latest 10-K release. These updates will provide a clearer picture of the opportunities and risks to EPD’s growth story.

Estimated Quarterly Volumes:

Haynesville: Haynesville flow sample data is down 3.0% from 4Q25 to 1Q26. DT Midstream’s Blue Union system is down 1.8% and Energy Transfer’s ENBL Haynesville system is down 3.5% Q-o-Q. The top producer on ENBL Haynesville is Expand Energy (890 MMcf/d).

Northeast: Northeast flow sample data is down 2.0% from 4Q25 to 1Q26. CNX’s dry gathering system is down 1.4% Q-o-Q and Williams’ Susquehanna Supply Hub is down 1.9%. Top producers on Susquehanna Supply Hub include Coterra Energy (1.8 Bcf/d), Expand Energy (324 MMcf/d) and BKV Corp. (25 MMcf/d).

Calendar: