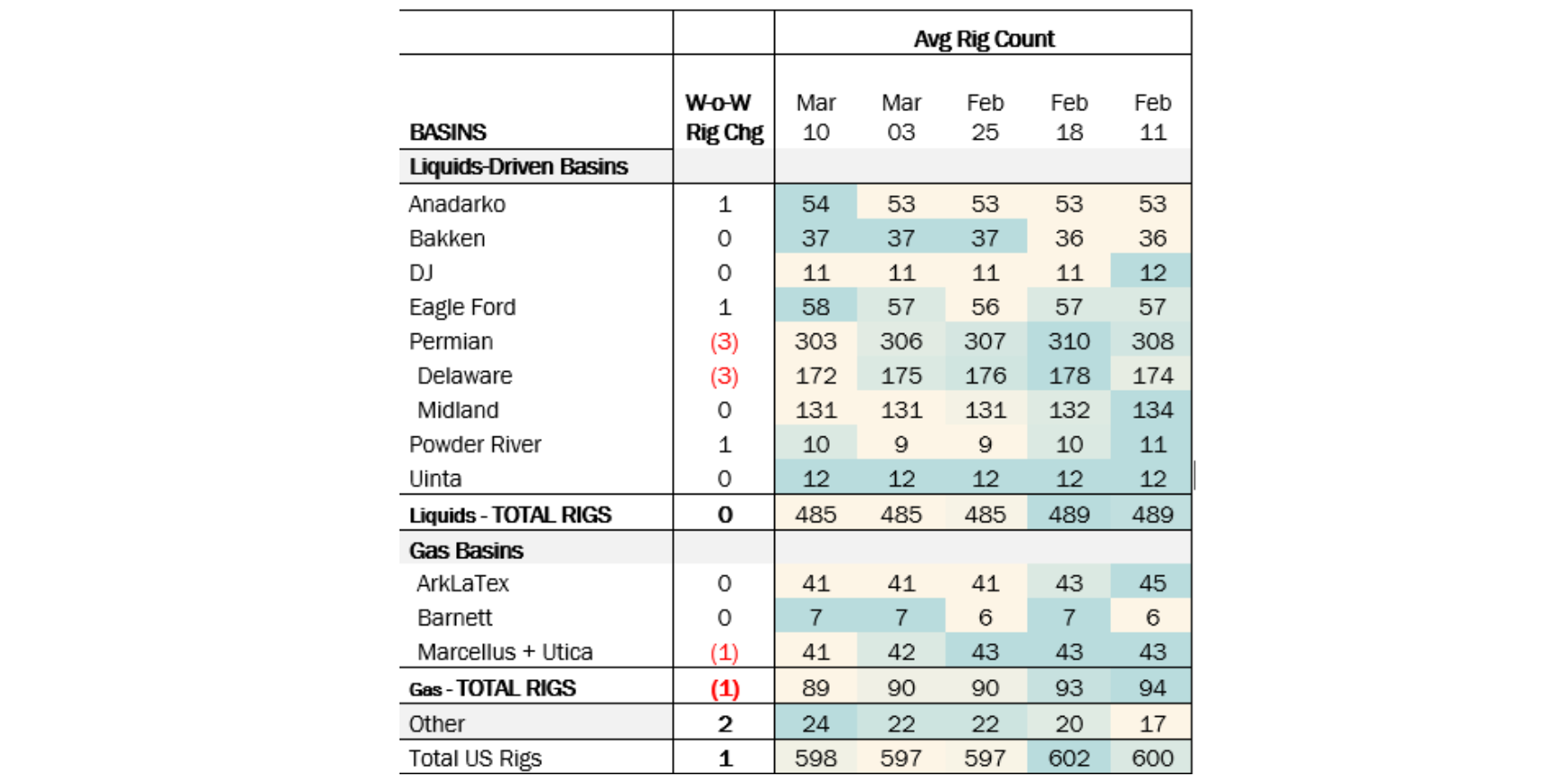

Executive Summary: Rigs: The total US rig count increased by 1 rig W-o-W from 597 to 598 rigs for the week of March 10. Infrastructure: The Permian growth story is set to continue in 2024. Storage: East Daley expects a withdrawal of 1.435 MMbbl in commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending March 22.

Rigs:

The total US rig count increased by 1 rig W-o-W from 597 to 598 rigs for the week of March 10. The Anadarko, Powder River and Eagle Ford basins each gained 1 rig, whereas the Permian lost 3 rigs and the Marcellus + Utica lost 1 rig.

In the Delaware Basin, Vital, Oxy and ConocoPhillips each dropped a rig. Blackstone Minerals and Endeavor added rigs in the Uinta and Eagle Ford.

Infrastructure:

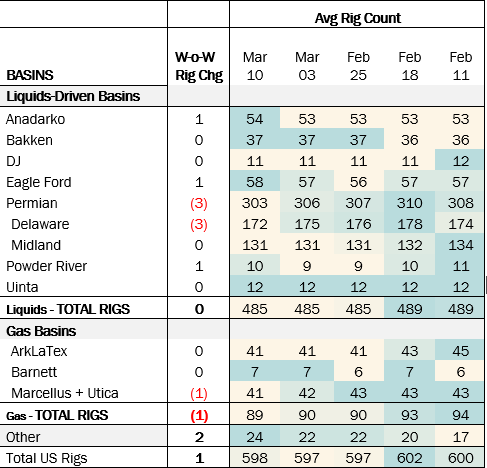

The Permian growth story is set to continue in 2024. East Daley’s Crude Hub Model shows liquids production grew ~536 Mb/d on average in 2023, and predicts Permian growth of 368 Mb/d in 2024 vs ‘23. Our forecast considers freeze-offs in January 2024 and current natural gas constraints.

EDA expects Permian crude growth will be weighted towards the back half of the year, tied to start-up of the Matterhorn gas pipeline scheduled in 2H24. Matterhorn will provide further takeaway capacity from the Permian to allow crude drilling to continue, resulting in additional supply growth.

The table above shows estimated production growth for both public and private producers. Public companies provide guidance on their expected production, which is accounted for in East Daley’s Permian Basin forecast. EDA forecasts 6.3% growth in 2024. We estimate private operators will increase their production by ~6.6% for the year.

Storage:

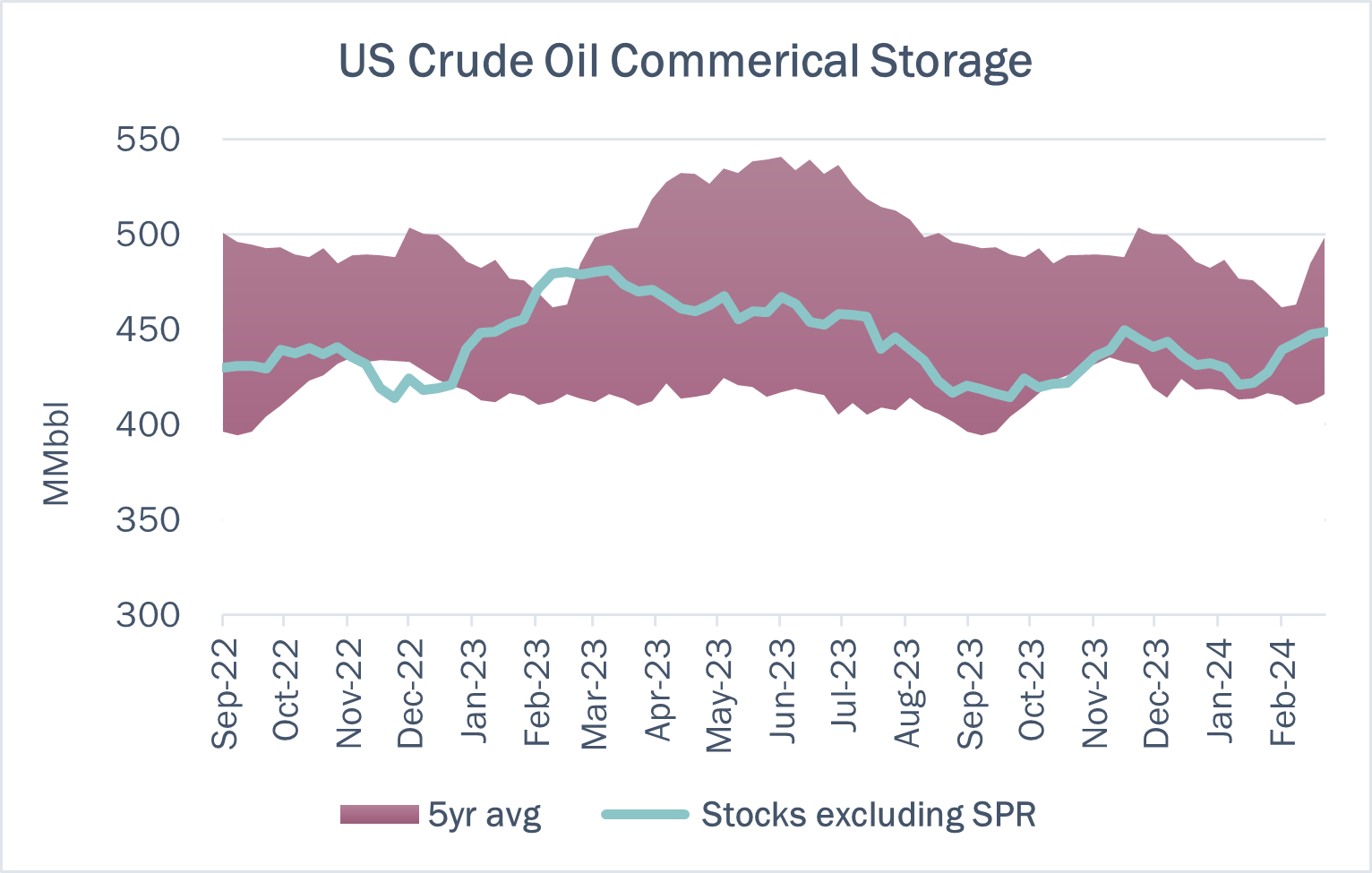

East Daley expects a withdrawal of 1.435 MMbbl in commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending March 22. We expect total US stocks, including the SPR, will close at 805.913 MMbbl.

The US natural gas pipeline sample, a proxy for change in oil production, fell by ~0.26% in aggregate across all liquids-focused basins, falling by 2.6% and 2.9% in the Gulf of Mexico and Anadarko, offset by ~3.7% increases in the Barnett and Eagle Ford. We expect US crude production to remain flat at 13.1 MMb/d.

According to US bill of lading data, US crude imports increased by 422 Mb/d W-o-W to 6.7 MMb/d. More than 60% of the supply originated from Canadian pipelines into the US, with the remainder largely coming from ships carrying crude from Mexico, Brazil and Venezuela.

As of March 22, there was ~1054 Mb/d of refining capacity offline, including downtime for planned and unplanned maintenance. EDA expects gross crude inputs into refineries to increase by ~595 Mb/d W-o-W, coming in at 16.38 MMb/d.

Vessel traffic monitored by EDA along the Gulf Coast decreased W-o-W. There were 23 vessels loaded for the week ending March 23 and 31 the prior week. EDA expects US exports to be 4.5 MMb/d.

The SPR awarded contracts for 2.99 MMbbl to be delivered in March 2024. The SPR has 362.306 MMbbl in storage as of March 19, 2024.

Regulatory and Tariffs

Presented by ARBO

Tariffs:

TransCanada Keystone Pipeline, LP The temporary discounted rates have been extended through April 30, 2024. (FERC No 6.96.0 IS24- 203, filed February 26, 2024)

Tallgrass Pony Express Pipeline, LLC All currently effective non-contract temporary volume incentive programs have been modified to extend each program’s expiration date from March 31, 2024 to June 30, 2024. The rates are unchanged. (FERC No 2.59.0 IS24- 213, filed February 29, 2024

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at [email protected] or phone at 202-505-5296. https://www.goarbo.com