Market Movers:

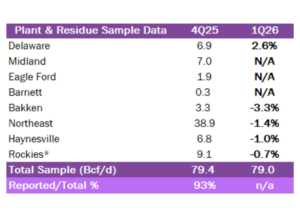

Estimated Quarterly Volumes 4Q25 to 1Q26:The Delaware (2.6%) is trending up while the Bakken (-3.3%), Northeast (-1.4%), Haynesville (-1.0%) and Rockies (-0.7%) are trending down Q-o-Q.

Calendar: The next financial model update will occur on April 17.

Market Movers:

The closure of the Strait of Hormuz is driving sharp volatility in crude oil and has pushed markets to trade off a binary headline: open or closed. Yet the physical crude market doesn’t clear that way. Even after the strait reopens, oil markets will normalize through a phased restart, not an immediate reset.

Resuming transit is only the first step. A multi-stage process will then follow: clearing anchored vessels, resuming loadings, completing voyages, discharging cargoes and rebalancing refinery runs. Each stage introduces lag. As a result, the physical market can remain tight well after the waterway is operational.

Restart Sequence Drives Market Tightness

Reopening the Strait of Hormuz does not immediately release trapped supply into the global system. Instead, the market will work through a backlog:

- Strait transit resumes.

- Anchored tanker queues begin clearing.

- Export terminals restart loadings.

- Cargoes complete voyages (a multi-week lag).

- Refinery runs rebalance as feedstock arrives.

Even in a best case, normalization will be measured in weeks, not days. Vessel congestion, port sequencing and voyage times all extend the timeline between “open” and when the market is fully supplied.

A Quality Problem, Not Just a Volume Problem

Moreover, the disruption is not simply about missing barrels. It is also about missing specific barrels.

The Middle East predominantly exports medium and heavy sour crude. Many global refining systems – particularly in Asia and on the US Gulf Coast — are configured to run these grades. Replacing them is not straightforward.

Light sweet substitutes like US shale oil are more abundant, but they are imperfect replacements. Running lighter crude slates can reduce yields and compress margins at complex refiners. As a result, even if headline supply appears adequate, refinery-compatible supply remains constrained.

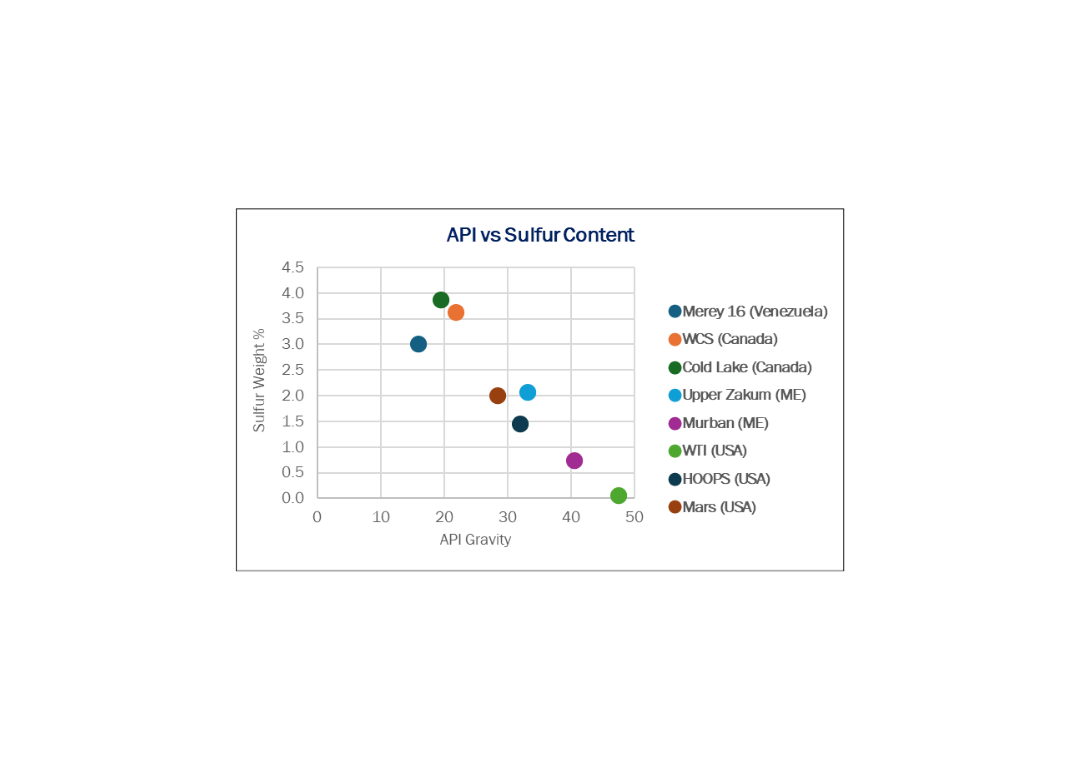

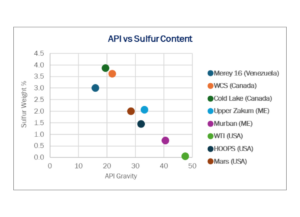

For the US market, the impact shows up in regional price and quality differentials rather than outright shortages.

- WTI vs Brent: Dislocations can widen as seaborne crude remains constrained relative to inland supply.

- Cushing: Inventory draws may accelerate if inland barrels are pulled toward the Gulf Coast.

- Gulf Coast refining: Facilities optimized for heavier slates face tighter feedstock conditions.

- Crude differentials: Medium and heavy grades (e.g. Mars, Canadian heavy) should outperform light sweet benchmarks.

In short, the disruption spreads through relative pricing, including regional spreads and different crude qualities.

The path to normalization will be visible through physical signals:

- Tanker congestion and freight rates

- Export terminal throughput

- Timing of Middle East cargo arrivals

- Refinery utilization rates

- Medium/heavy crude differentials

These indicators will turn before the broader narrative does.

Bottom Line: Reopening the Strait of Hormuz is essential to normalizing the crude market – but is only a first step. The crude market will clear through a staged process driven by logistics and crude quality that extends beyond the headline event. Until tanker queues unwind, cargoes arrive and refineries rebalance, the market remains structurally tight.

Estimated Quarterly Volumes

The Total Sample represents the flow sample and plant data accessible to East Daley. The latest Q-o-Q percentage change is estimated by comparing either flow sample data Q-o-Q or plants within a basin that have continuously reported inlet volumes from the prior quarter to the current quarter. 1Q26 is expressed as growth from 4Q25 to 1Q26.

Rockies represents the aggregate of Big Horn, DJ, Green River, Piceance, Powder River, San Juan, Uinta and Wind River basins.

Bakken: The Bakken’s flow sample is down 3.3% 4Q25 to 1Q26. Silver Hill’s system is down 5.0% and Pembina’s Palermo system is down 5.9% Q-o-Q. The top producers on Palermo include ConocoPhillips (13 MMcf/d), Chevron (9 MMcf/d) and Chord Energy (6 MMcf/d).

Rockies: The Rockies’s flow sample is down 0.7% 4Q25 to 1Q26. Williams’s Opal system is down 1.7% while Western Midstream’s Chipeta system is up 6.0% Q-o-Q. The top producers on Chipeta include Koda Resources (191 MMcf/d), Urban Oil & Gas (35 MMcf/d) and Greylock Energy (16 MMcf/d).

Calendar: