Market Movers: Permian gas constraints and capital discipline could blunt the traditional supply response from the spike in WTI prices.

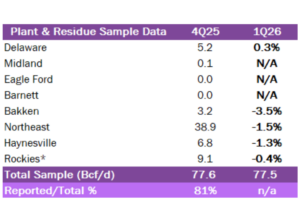

Estimated Quarterly Volumes:

4Q25 to 1Q26: The Delaware (0.3%) is up, while the Bakken (-3.5%), Northeast (-1.5%), Haynesville (-1.3%) and Rockies (-0.4%) are down Q-o-Q.

Calendar: EDA will be in Tulsa March 23-26. The next financial model updates will occur on March 27 and April 17.

Market Movers:

Permian Basin gas constraints and capital discipline could blunt the traditional supply response from the spike in WTI prices.

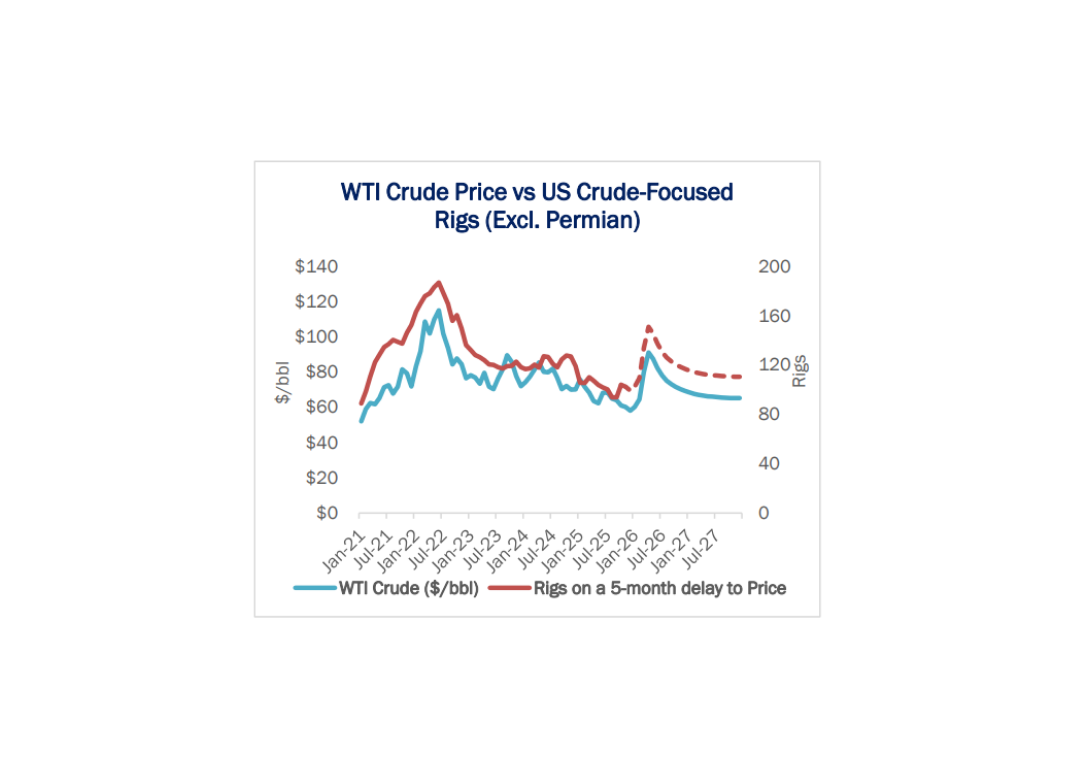

WTI crude prices have been volatile, jumping to over $110/bbl on March 9 in response to shipping restrictions in the Strait of Hormuz. However, the spike is unlikely to drive incremental supply from the Permian Basin in 2026.

The constraint is not economics but infrastructure: Limited natural gas takeaway restricts producers’ ability to increase drilling activity. Until new pipelines such as Blackcomb and Hugh Brinson add a combined 4.7 Bcf/d of capacity by YE26, producers will struggle to move associated gas – and therefore crude – out of the basin.

This dynamic matters because the Permian is the largest oil-producing region in the US. In previous cycles, higher oil prices typically trigger increased drilling activity and supply growth from the basin. However, producers today face a structural bottleneck that limits their ability to respond to price signals.

If the Permian cannot respond, the market will naturally look to other liquids-rich basins to provide incremental supply. The Bakken, Rockies, Anadarko and Eagle Ford plays have historically increased drilling activity when oil prices rise. Data from East Daley Analytics’ Energy Data Studio shows that rig activity in these basins typically responds to WTI price movements with roughly a five-month lag (refer to the graph).

At first glance, the connection suggests that higher prices could encourage operators in these basins to increase drilling and bring additional supply to market. However, two structural factors are likely to blunt the customary price response.

The first is the signal coming from the oil forward curve. WTI futures are steeply backwardated. While the Apr ‘26 contract traded near $98/bbl Friday (March 20), the average WTI price for 4Q26 is closer to $77. Producers are unlikely to materially increase capital budgets based on a price spike that the market expects to be temporary.

The second constraint is capital allocation flexibility. Several producers with exposure to the Bakken, Rockies and Anadarko also maintain significant positions in the Permian. Operators like Devon Energy (DVN) can shift capital across basins. With new gas takeaway capacity expected to come online in the Permian by late 2026, these operators may be reluctant to redirect capital toward other regions for what could prove to be a short-lived opportunity.

As a result, the pool of producers positioned to capitalize on a short-term oil price spike is relatively small. The companies most likely to benefit are those with limited hedge exposure and existing operational capacity, including available drilling contracts and pipeline takeaway in basins outside the Permian.

A handful of operators fit this profile. Companies such as EOG Resources (EOG), Chord Energy (CHRD) and Civitas Resources (CIVI) have the scale and flexibility to opportunistically capture higher prices without committing to large, long-term increases in capital spending.

In the near term, Permian infrastructure constraints, backwardated oil prices and capital discipline could limit the typical supply response to higher crude prices. While a price spike would still improve cash flows for producers, it may not translate into the rapid production growth the market has come to expect from US shale.

Estimated Quarterly Volumes

The Total Sample represents the flow sample and plant data accessible to East Daley Analytics. The latest Q-o-Q percentage change is estimated by comparing either flow sample data Q-o-Q or plants within a basin that have continuously reported inlet volumes from the prior quarter to the current quarter. 4Q25 is expressed as Q-o-Q growth from 3Q25 and 1Q26 is expressed as Q-o-Q growth from 4Q25.

The Rockies represents the aggregate of Big Horn, DJ, Green River, Piceance, Powder River, San Juan, Uinta and Wind River basins.

Delaware: Delaware plant inlet data is up 0.3% from 4Q25 to 1Q26. Kinetik’s Durango Midstream system is up 1.7% Q-o-Q and Matador Resources’ San Mateo Black River system is up 0.7% Q-o-Q. Top producers on San Mateo include Matador (335 MMcf/d), Occidental Petroleum ( 70 MMcf/d) and Devon Energy (44 MMcf/d)

Appalachia: The Appalachia flow sample is down -1.5% from 4Q25 to 1Q26. The MPLX – Bluestone system is up 3.9% Q-o-Q while the Williams – Utica East Ohio system is down 6.2% Q-o-Q. The top producer on Bluestone is PennEnergy Resources (338 MMcf/d).

Calendar: