Executive Summary: Rigs: The total rig count decreased by 5 for the week ending December 22, down to 530 from 535. Flows: The pipeline sample from Dec 29 to Jan 5 was relatively flat – the real question is how much of an impact the winter weather will have on Jan’25 supply. Infrastructure: PSX’s $2.2B EPIC acquisition continues a race among large midstream companies for Permian NGL barrels. Calendar: With 4Q24 earnings right around the corner we will be updating the calendar with company-reported earnings release dates as they are announced.

Infrastructure:

Phillips 66 (PSX) has struck a $2.2B deal to acquire EPIC NGL pipeline and fractionation assets in the Permian and South Texas. The acquisition confirms a key structural factor East Daley sees pushing ethane supply higher: the race for Permian NGL barrels by large midstream companies.

Ethane was the quiet star of the Permian Basin in 2024, hitting multiple monthly records despite oil and gas production struggling to reach prior highs. Growth from the Permian propelled Lower 48 ethane to new production records in March, April, May and October ’24, as highlighted in our monthly Ethane Supply & Demand Report. The magnitude of ethane growth has been surprising and has influenced EDA’s 2025 forecast. Our new outlook suggests a market that is long supply, short of a price adjustment in 2H25.

There are several factors that support the robust supply outlook. First, new and expanded NGL pipelines debottlenecked Permian NGL supply in 2024 (e.g. Targa’s Daytona pipeline) and will continue to add more capacity in 2025, based on projects from ONEOK (OKE), Enterprise Products (EPD), Energy Transfer (ET), MPLX, and EPIC Midstream. We have already accounted for the additional infrastructure and impact to supply growth in our NGL Hub Model.

Second, and unique to ethane, is the race for big strategic midstream companies to acquire the NGL barrel (refer to the graph). The callouts in the figure show these acquisitions since 2022, which have resulted in more rich gas processed under integrated midstream ownership. In 2022, about 50% of rich gas in the Permian was processed by large integrated midstream owners (refer to the blue line in the figure). That number is now higher than 75%. The $2.2B EPIC acquisition by PSX this week continues this trend.

The growing ownership by integrated midstream matters because these companies are more incentivized to extract ethane from their processing plants. A molecule of ethane is more valuable to an integrated company than a molecule of gas because of the fee-based earnings potential to transport, store, fractionate and export.

Now, a much smaller portion of ethane is left in the hands of owners that consider the opportunity cost of selling gas before cooling cryogenic gas plants for ethane extraction. Structurally, there is very little ethane that will be left in the gas stream in the Permian Basin. Price-sensitive ethane is now dependent on swing basins like the Bakken and Rockies to balance the market.

East Daley covered the latest $2.2B PSX-EPIC deal in a First Take for clients. We plan to host a client-only webinar next week to explore implications for the Permian and NGL markets.

Rigs:

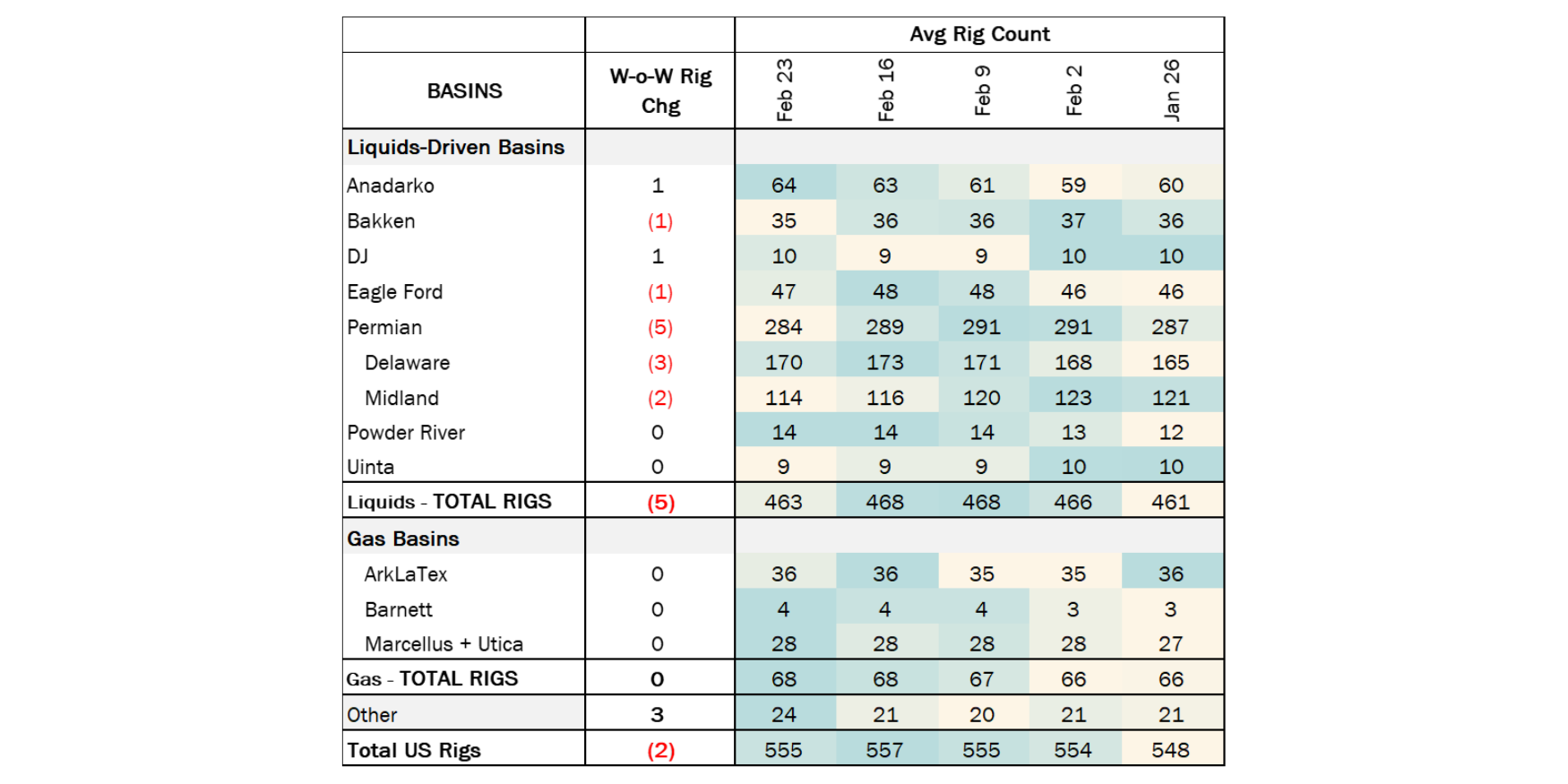

The total rig count decreased by 5 for the December 22 week, down to 530 from 535. Liquids-driven basins declined by 6 rigs W-o-W.

- Permian (-6):

- Delaware (-6): Occidental Petroleum (-2), Conoco Phillips (-3), Continental (-1)

- Eagle Ford (-1): EOG Resources (-1)

- Powder River (+1): Occidental Petroleum (+1)

Flows:

- The pipeline sample from Dec 29 to Jan 5 was relatively flat, increasing by 160 MMcf/d and ending at 69.9 Bcf/d. The Midland sample rose W-o-W by 4%, while the Delaware sample declined 2%. Overall Permian flows have been impacted by El Paso Pipeline maintenance, and the decrease could extend until mid-January if expected winter storms disrupt operations.

- Freezing weather and snowstorms across the US are starting to curtail production in several basins. US pipelines samples for Monday and Tuesday (January 6-7) were ~2.8 Bcf/d lower than the December monthly average. The Northeast (-1.5 Bcf/d), Anadarko (-0.6 Bcf/d) and Permian (-0.3 Bcf/d) samples show signs of freeze-offs from frigid temperatures this week, and will be reflected in the next weekly averages for Jan 6 - 12.

*W-o-W change is for the two most recent weeks.

- The latest winter storm is already having an impact on Jan’25 production. Our initial estimate is Jan’25 production could see a 5% decrease in production.

- From an NGL perspective, this would knock off about 360 Mb/d of total NGLs from the market in January. Initial thoughts are the impact for this storm will be shorter in duration and less severe, therefore the 5% impact to supply vs some of the larger impacts from prior storms noted below.

*****

- #1 below was Winter Storm Uri

- Days of production impacted ~ 7-11 days (2/10/21-2/20/21).

- NGL M-o-M decline was 970 Mb/d (19% decrease).

- #2 below was Winter Storm Elliott

- Days of production impacted ~6 days from (12/21/22-12/26/22)

- NGL M-o-M decline was 539 Mb/d (9% decrease).

- #3 below was Winter Storm Heather

- Days of production impacted ~10 days (1/13/24-1/23/24).

- Propane M-o-M decline was 591 Mb/d (9% decrease).

Data Points & Product Release Calendar:

-1.png)

-1.png)