Executive Summary: Infrastructure: INEOS has borrowed almost €1.6B following its permit approval, which will bring online ethane demand north of 80 Mb/d. INEOS is likely the anchor customer at EPD’s Neches River ethane dock expansion project. Rigs: The total rig count increased by 3 for the December 1 week, up to 572 from 569. Flows: Gas production as measured by the interstate gas meter sample was up slightly W-o-W by almost 1%, driven by a seasonable ramp in Northeast demand (and supply) and Anadarko flows returning to normal after maintenance work impacting MEP volumes. Calendar: As a reminder, FERC 3Q24 Filings were due to FERC on Dec 11 so FERC-filed NGL pipe data is now available through 3Q24.

Infrastructure:

The US is producing a record supply of ethane, hitting a new high in September ’24 for the fourth time this year (March, April and May ’24 were also records). International petrochemicals are preparing to source more of the abundant and cheap feedstock. EDA already covered how Braskem will import more US ethane by the middle of 2025.

INEOS is likely preparing to do the same with Project One, its ethane cracker under construction in the Port of Antwerp in the Netherlands. Project One is designed to make up to 1.45MM tons of ethylene per year. A facility of that scale will require more than 80 Mb/d of ethane to run at capacity.

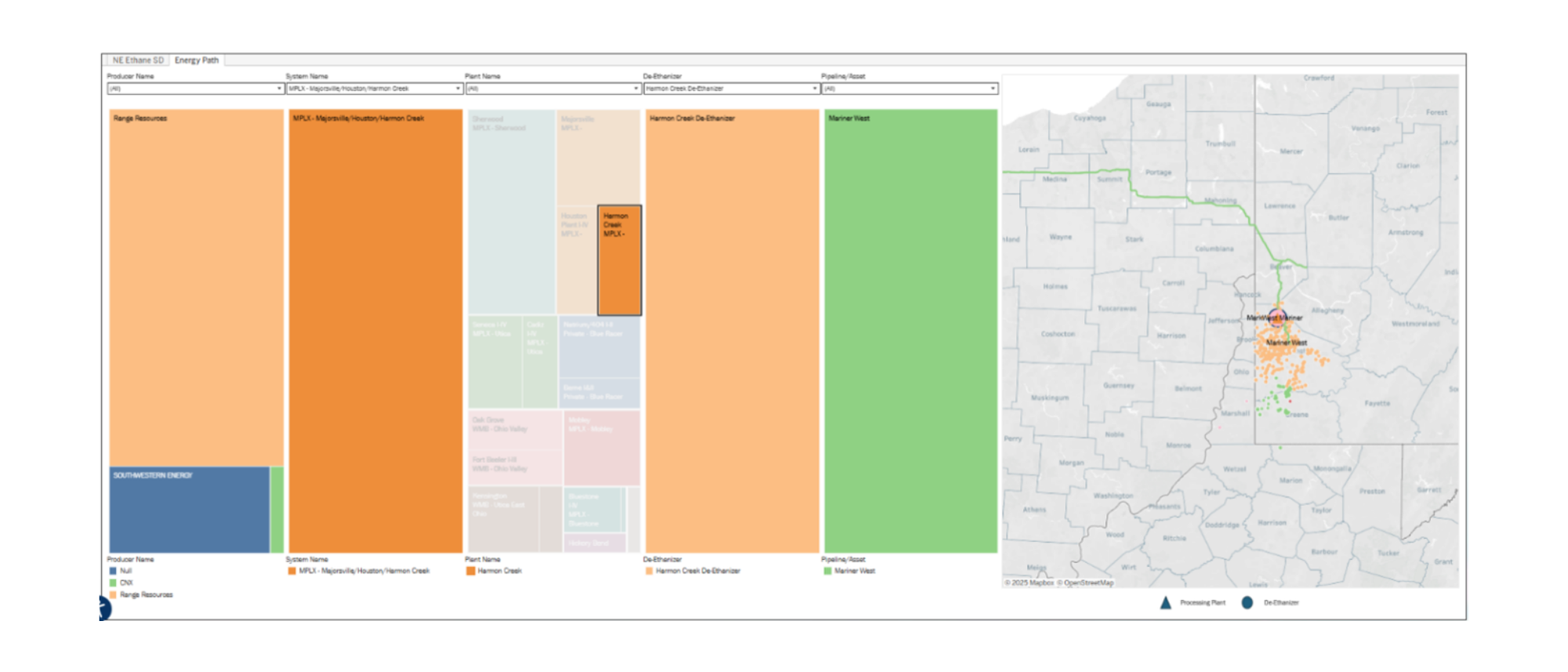

EDA has not seen public disclosure of where INEOS will source ethane to supply Project One, but we speculate the company is an anchor customer of Enterprise Products’ (EPD) new ethane export facility, Neches River. EPD plans to begin operations at the Texas facility in two phases. Phase I would start in 3Q25 and includes a 120 Mb/d ethane refrigeration train, new loading dock, and a 900 Mbbl refrigeration tank. In Phase II, EPD is building a flex refrigeration train of 180 Mb/d ethane, 360 Mb/d propane, or a combination of both. Phase II has an in-service target of 1H26.

This would not be INEOS’ first foray into sourcing US ethane. The JS INEOS Intrepid and JS INEOS Insight were the first vessels loaded from Energy Transfer’s (ET) Marcus Hook dock in March ’16 and EPD’s Morgan’s Point dock in September ’16 for use in its Rafnes, Norway ethylene cracker. As shown in East Daley’s Energy Data Studio, both export facilities are operating at or near capacity (only Marcus Hook is shown below). In the figure, the green-shaded area shows ethane exports. The green line is export capacity, including potential upside on an expansion project EDA has written about here. The pink line represents capacity if the expansion does not occur.

Project One has hit some snags. In July ’23, the Council of Permit Disputes annulled a permit needed to continue construction. The dip in financing drawn on the €4B capital project is evident in 3Q23 (see figure below). Construction resumed in January ’24 when the Flemish Minister for Justice & Enforcement re-issued a new permit. Total financing used so far for construction totals €1.6B. INEOS expects construction to finish by YE26. By then, EPD’s Neches River and EHT facilities will be operational, allowing Neches River to be used exclusively for ethane exports.

Rigs:

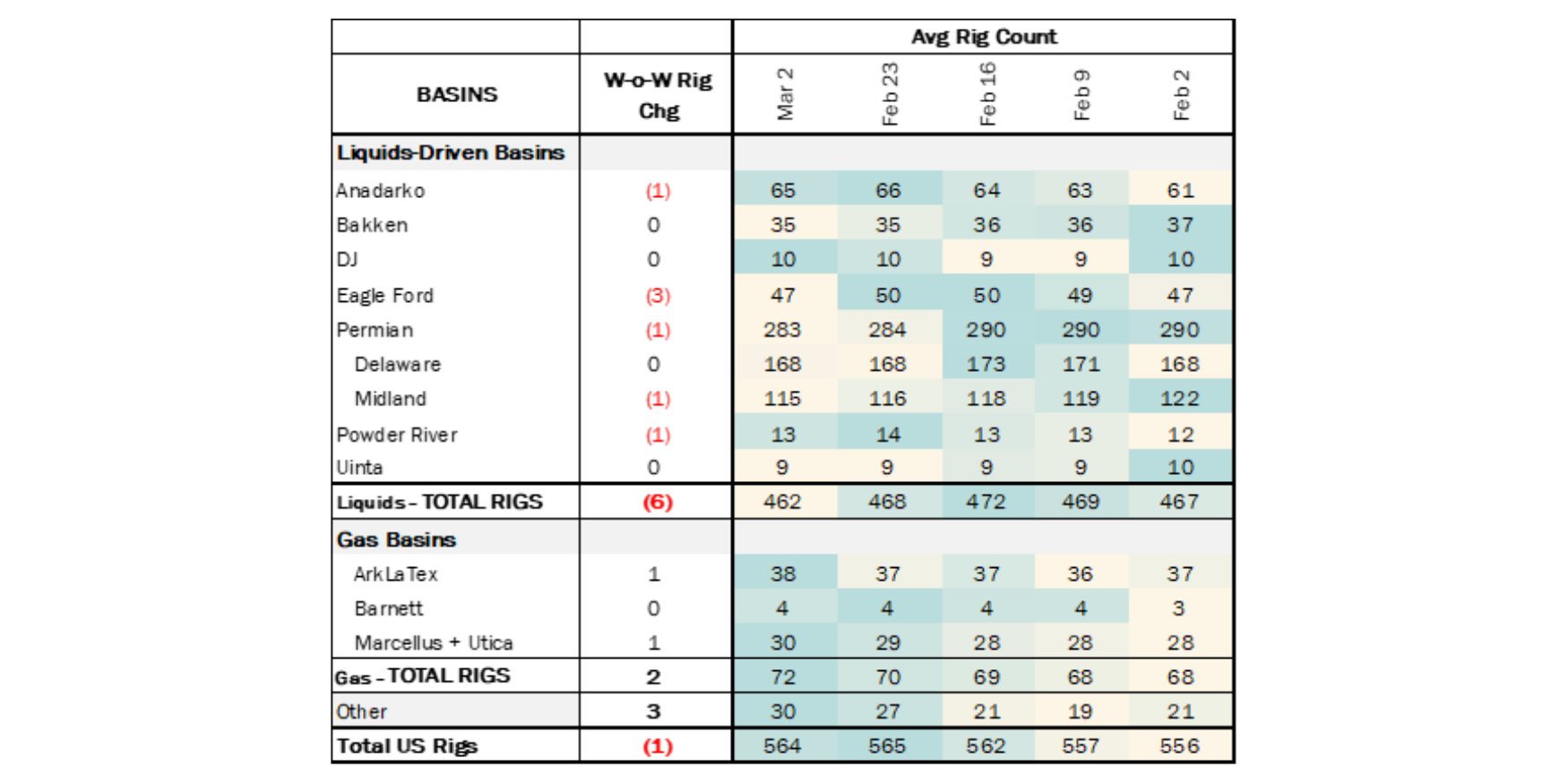

The total rig count increased by 3 for the December 1 week, up to 572 from 569. Liquids-driven basins increased by 2 rigs W-o-W.

- Anadarko (+1): Marathon Oil

- Permian – Midland (+1): Diamondback Energy

Flows:

- Gas production as measured by the interstate gas meter sample was flat W-o-W, with some minor puts and takes.

- In liquids basins, the biggest W-o-W change was in the Anadarko where the flow sample was up by 165 MMcf/d (+4.4%). The increase in Anadarko gas volumes is driven by MEP flows. EOIT, which delivers into MEP, has been under maintenance from November 1 - December 5 and returned to normal throughput on December 11.

- In gas-targeted basins, the Marcellus and Utica was up by 264 MMcf/d (1%). The Northeast has begun the anticipated seasonal ramp in heating demand, met by an increase in gas production. The seasonal production ramp started later than usual this year but is now contributing to growth. Heighted winter demand (and supply to meet it) usually peaks in January.

Data Points & Product Release Calendar:

-1.png)

-1.png)

-3.png)