Dirty Little Secrets 2022: Midstream’s Role in the Future of Energy

East Daley’s “Dirty Little Secrets” is our annual market report summarizing trends we expect to shape the U.S. midstream energy sector during the year ahead. We publish the report each December, highlighting our analysis of macro themes that give subscribers an edge in the energy market. “Dirty Little Secrets 2022: Midstream’s Role in the Future of Energy” was delivered in webinar form on Dec. 1, 2021. We published the report included below on Dec. 14, 2021, outlining major themes of the 2022 DLS. All information and analysis included in the report are published as of Dec. 2021 and have not been updated to reflect more recent forecasts.

Over the next few years, Midstream is in a unique position where it can invest in incremental growth projects, increase shareholder returns, reduce debt, invest in energy transition, and decrease its own emissions.

In Dirty Little Secrets 2022: Midstream’s Role in the Future of Energy, we share our macroeconomic outlook for U.S. Oil, Natural Gas, and NGLs review producer discipline scenario implications on midstream, highlight key infrastructure opportunities, as well as assess the Energy Transition opportunity and investment potential.

We forecast major midstream companies will generate staggeringly more in free cash flow during 2021-2025 than they will be able to spend on traditional infrastructure projects. We anticipate plenty of capital remaining that can be invested, and DLS 2022 explores options for this capital spending.

Midstream’s Role in the Future of Energy

Midstream can do it all in the next few years, according to East Daley research. The selective new infrastructure will be needed especially for gas and NGLs, and while we acknowledge that Energy Transition (and especially carbon) is a huge opportunity, there is a timing mismatch where large-scale projects are likely not immediately available.

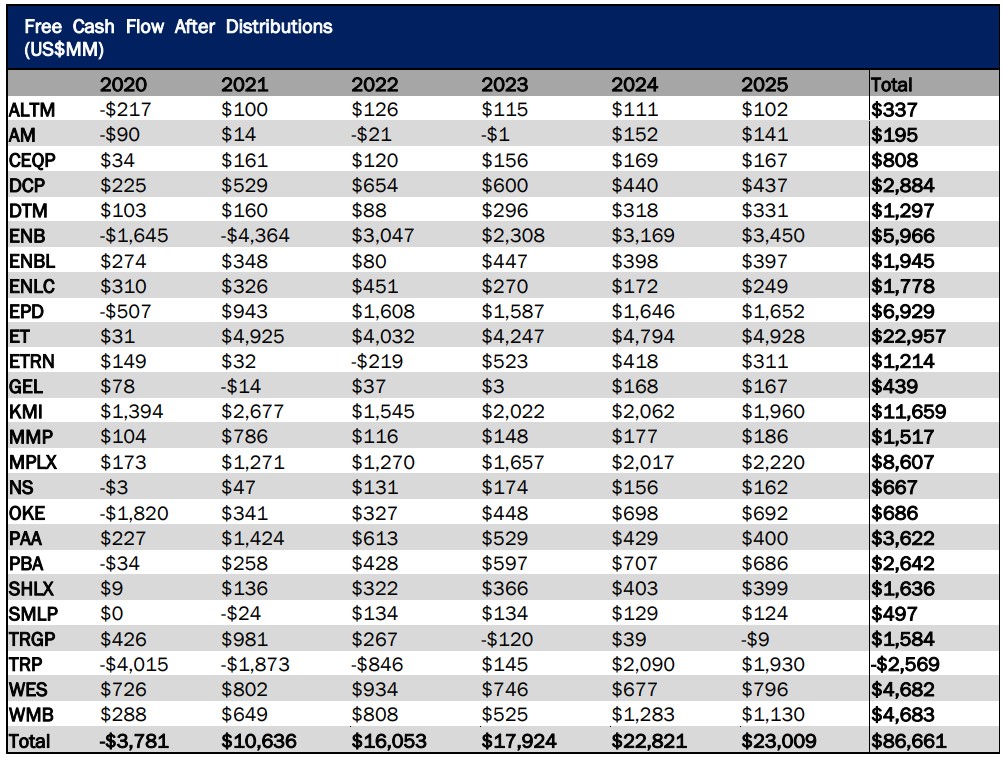

Infrastructure remains overbuilt in many basins after the previous wave of G&P projects, but Midstream is finally starting to see returns from those projects. Companies have latent capacity they are growing into, increasing EBITDA with limited current capex and fewer projects to chase. East Daley forecasts major midstream companies will generate $90 billion in FCFE After Distributions from 2021-2025. Outside of debt reduction, share buybacks, and additional dividend increases, we anticipate plenty of capital remaining that can be invested. This $90 billion in FCF remains after spending on current growth capex, debt reduction, and forecasted returns to shareholders. Production growth has slowed, so new infrastructure needs will be limited and primarily centered around natural gas and NGLs. Energy Transition has the potential to fuel the next wave of the energy infrastructure buildout, but the reality is that the technology is too new and the current opportunity is too small. Midstream will have $90 billion in the next few years, but Energy Transition projects may not be able to absorb significant capital until post-2025 or even 203+0.

Midstream is going to generate a lot of cash over the next four years, $90 billion for the 25 companies we actively follow. The industry is in a unique position where it can invest in incremental growth projects, increase shareholder returns, reduce debt, invest in energy transition, and decrease its own emissions. We still expect oil, gas, and NGL production to grow, and selective new infrastructure will be needed within the next few years to meet growing demand expectations, especially for natural gas and NGLs. Midstream is looking to invest in carbon, hydrogen, and other energy transition opportunities. But project sizes are small and returns unclear.

Natural Gas: Too Much of a Good Thing?

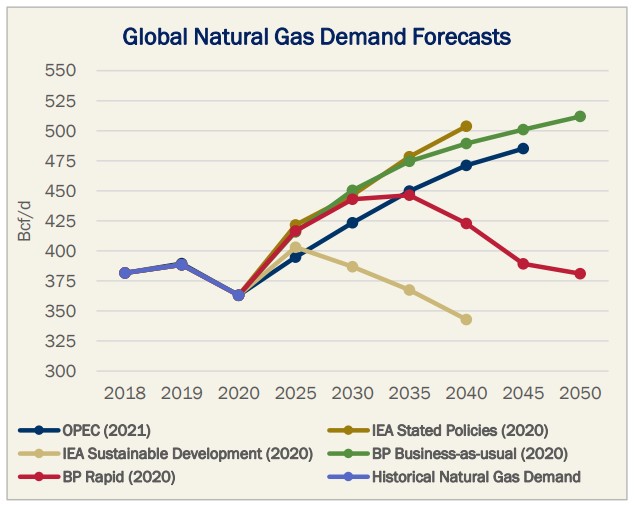

In our view, natural gas is cementing its role in the Energy Transition — the world will need gas to feed growing electricity demand (especially as transportation is electrified), and natural gas can reduce emissions by displacing coal. Natural gas demand projections from various organizations mainly indicate demand growth through 2040-2050 (see Figure 2). In netzero policies and technologies scenarios where gas demand peaks earlier, technologies would need to accelerate significantly in order to reduce gas demand in that time frame. Recent global energy shortages, including soaring natural gas prices in Europe and Asia, illustrate how a rapid transition away from fossil fuels would be painful, if not impossible. We expect natural gas to play a key

role in the global energy transition, and we expect downward pressure on prices in 2023. This pressure would present midstream M&A and investment opportunities that could bear fruit in 2024 and beyond when new LNG demand pushes our Adj. Henry Hub price above the current strip.

Growth in associated gas (especially the Permian) is the primary risk to natural gas prices. While operators have stuck to capital discipline, we still project associated gas will account for 68% of U.S. supply growth through 2025. We expect producers in gas basins, especially the Northeast, will need to decrease near-term rigs despite $5/MMBtu gas. Higher associated gas production will be able to meet demand at least until 2024 when new LNG demand ramps up. The ArkLaTex should still see growth due to the basin’s proximity to LNG export facilities, but rig additions may also be limited.

Natural gas provides plenty of traditional midstream opportunity, as strong supply growth will require additional processing and egress capacity in the Permian, and strong LNG demand growth will require more southbound residue gas pipelines in the ArkLaTex. Accelerated LNG export growth will further support expectations for high gas prices. Companies can take advantage of this growth, and hedge against lower oil prices, by investing in Tier 2 gas basins.

Crude Oil: Midstream Opportunities Ahead?

Despite slowing global demand growth for crude oil and lower spending by producers, East Daley still expects U.S. crude oil production to grow by ~2 MMb/d by 2025. Private producers are driving growth in rigs and supply, and they are key to tracking future U.S. production trends.

We expect U.S. supply growth to be driven by the Permian. Production should rebound to 5% above pre-pandemic levels by YE2025. We forecast Permian supply to grow to 6 MMb/d in 1H2023 and reach almost 7 MMb/d by YE2025. We also expect U.S. supply growth to remain restrained even if prices are higher, limiting the need for additional

crude infrastructure investments (see Figure 3).

Given current expectations for producer spending, infrastructure is sufficient to support near-term growth in oil basins, and thus opportunities are more limited for crude-directed capital. Like 2016, we expect increased competition for barrels will reduce earnings for the marketing arms of midstream companies. We see a scenario where more crude oil infrastructure is necessary if producers loosen spending and increase drilling activity. For example, in our High Case scenario, Gulf Coast capacity fills up in 2023 and total capacity fills by YE2025.

Natural Gas Liquids: From Black Sheep to Golden Child

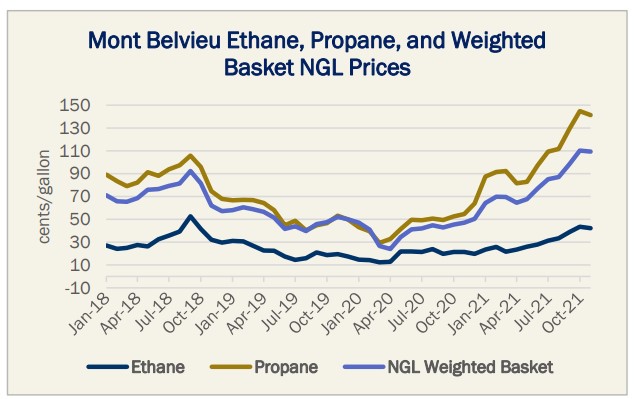

We see market dynamics in NGLs like the natural gas story, especially in ethane and propane, as robust Gulf Coast and international demand support prices. NGLs are often overlooked in the sector, but the “forgotten rally” of 2021 brought NGL prices higher than crude or natural gas, respectively, in the period since March 2020.

International demand for propane has boomed, but midstreamers were quick to develop LPG export capacity, which is now overbuilt. The incumbents (ET, EPD, TRGP) will benefit as volumes fill latent capacity. Ethane and propane are expected to supply most of the global feedstock volume for steam crackers. The IEA expects ethane demand could double to 6.7 MMb/d from 2020-2050.

NGL supply growth is strong on the back of Permian production, and long-term demand for U.S. NGLs is also strong. An incoming wave of ethane crackers in the U.S. and rising export demand should boost frac spreads, which will incentivize ethane recovery and boost NGL asset volumes. Despite this growing international demand, we still see limited ethane export capacity (held by ET and EPD) as an investment opportunity for other midstreamers.

Energy Transition: Opportunities and Realities

Midstream is looking to invest in carbon, hydrogen, and other Energy Transition opportunities, but project sizes are small and returns unclear. With ~$90 billion available to re-deploy, finding large-scale Energy Transition projects within the next

few years will be a challenge. Of the $90 billion in FCF generated by our midstream coverage over the next four years, FID’d or potential investments in Energy Transition total $5.7 billion (6.5% share). ENB’s offshore wind farm investments in Europe and TRP/PBA’s Alberta Carbon Grid project make up 87% of the $5.7 billion potential project costs.

More than 50% of Energy Transition projects we track focus on modifying existing assets for CO2, Hydrogen, RNG, and Biofuels. Many projects are early-stage partnerships to study the potential of new technologies and industries; capital costs

for these announced energy transition projects are not significant. Renewable power generation is further along as an industry, but midstream companies are mainly customers in this space. We anticipate development and acquisition of wind/solar generation assets is unlikely in the near term. A more tangible opportunity for midstreamers is CO2 transportation and utilization, but we see obstacles. Significant buildout is required to connect CO2 capture hubs to existing injection sites, and major regulatory changes are needed, including increased subsidies, and permitting reform to incentivize EOR.

Conclusion

East Daley presented our annual Dirty Little Secrets market report during a live webinar discussion with Bank of America on Dec. 1. In Dirty Little Secrets 2022: Midstream’s Role in the Future of Energy, we share our macroeconomic outlooks for U.S. Oil, Natural Gas, and NGLs, review producer discipline scenario implications on midstream, highlight key infrastructure opportunities, as well as assess the Energy Transition opportunity. We forecast major midstream companies will generate staggeringly more in free cash flow during 2021-2025 than they will be able to spend on traditional infrastructure projects. We anticipate plenty of capital remaining that can be invested, and DLS 2022 explores options for this capital spending.