Exec Summary

Market Movers: With most midstream earnings to be reported over the next two weeks, we take a look at some highlights from East Daley’s latest Earnings Previews.

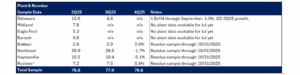

Estimated Quarterly Volumes: The Northeast meter point sample stepped down 2.6% from 3Q25.

Market Movers:

Kinder Morgan (KMI) kicked off 3Q25 earnings on Oct. 22, posting strong 9% Y-o-Y growth in gas gathering volumes that matched East Daley Analytics’ forecast. With the bulk of midstream earnings to be reported over the next two weeks, here are some of the highlights from our latest Earnings Previews.

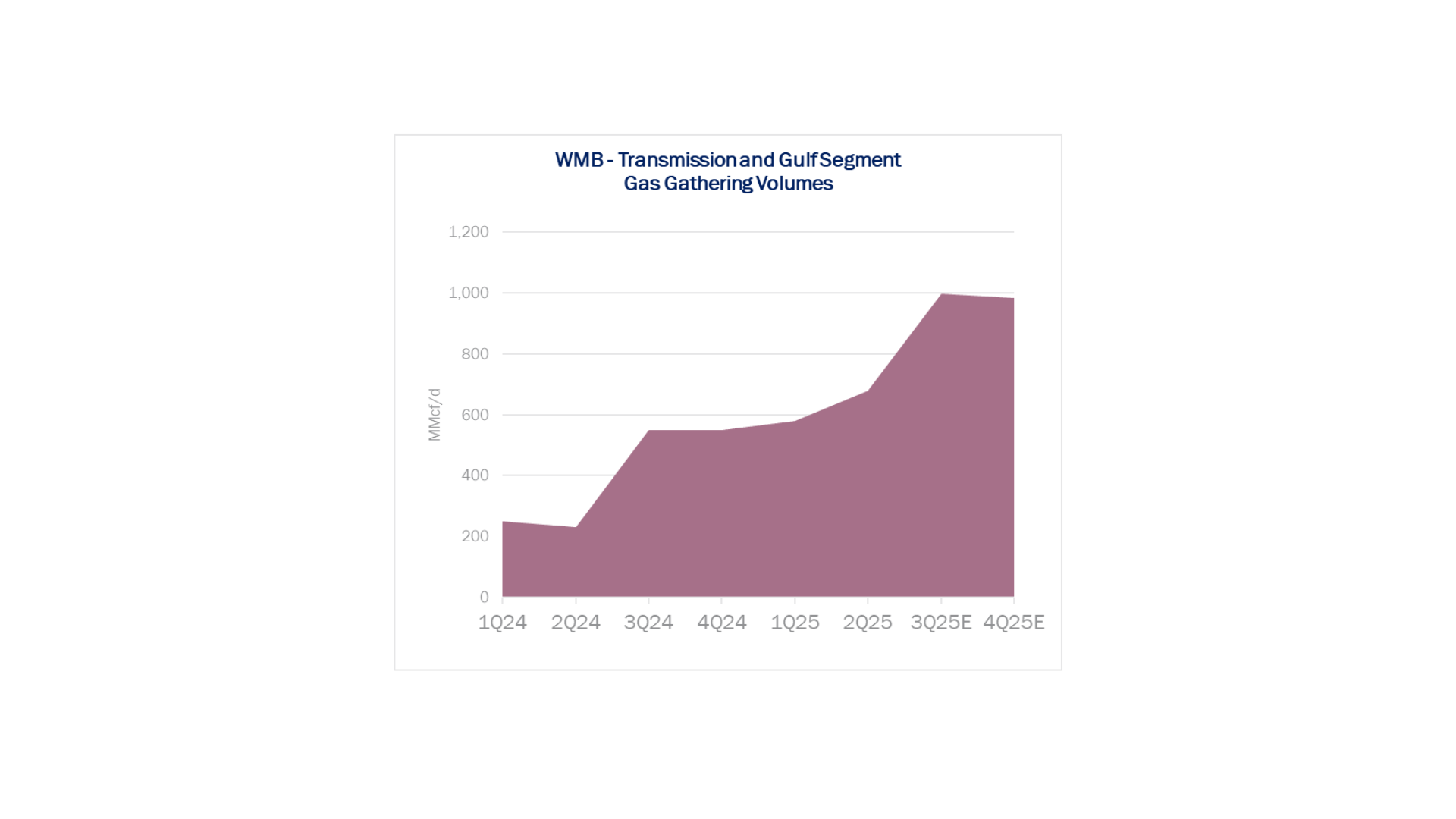

Williams (WMB): Williams entered 3Q25 with the wind at its back after lifting FY25 guidance in its 2Q update, specifically flagging the Saber Midstream acquisition in the Haynesville as fuel for the back half of the year. Saber adds 700 MMcf/d of gathering and dehydration capacity in the core Haynesville (Caddo Parish, LA / Harrison County, TX) at an attractive entry price.

We also expect big gains in the Transmission and Gulf segment as Shell’s Great White well ramps in the Mississippi Canyon area of the deepwater Gulf (see figure). Williams will also get a boost from the Salamanca well, which produced first oil Sept. 29. That well in the Keathley Canyon area will flow associated gas into WMB’s Discovery Pipeline. The Salamanca well brings a modest 3Q contribution but will keep volumes elevated in 4Q25.

DT Midstream (DTM): DTM reported 3Q25 Adj. EBITDA of $288MM vs East Daley’s estimate of $276MM in the Earnings Preview. We nailed DTM’s gas gathering volumes, predicting 17.6% Q-o-Q growth vs a print of 17.2% growth. The Blue Union and Haynesville New Producers expansions are online and contributing to the robust gains. East Daley’s Blue Union meter sample showed ~18% Q-o-Q volume growth. DTM also upsized its Guardian Pipeline expansion in Wisconsin to 540 MMcf/d (from ~210 MMcf/d) after a successful open season, reinforcing the theme of data center demand upside.

ONEOK (OKE): OKE reported Adj. EBITDA of $2,119MM vs our forecast for $2,044MM in the Earnings Preview. ONEOK experienced a fire on Oct. 6 at its MB-4 fractionator in Mont Belvieu, though it was a non-event for the quarter. The incident was confined to MB-4’s heater, no employees were injured, and the company doesn’t expect a material financial impact.

What matters for OKE’s setup: (1) Eiger Express reached FID, an ~2.5 Bcf/d Permian gas pipeline to Katy with WhiteWater, MPLX and Enbridge (ENB), and (2) the post-Magellan portfolio is taking shape with an open season for the Sun Belt Connector to Phoenix, creating growth opportunities in refined products. Taken together, we see a near-term uplift from NGLs and refined products, with Permian pipes extending growth in the out years.

Enterprise Products (EPD): A mid-August crude leak at EPD’s ECHO terminal temporarily dented Seaway flows; full operations resumed Aug. 15, limiting the crude/terminal headwind to a small slice of the quarter. Offsetting that, EPD’s Frac-14 at Mont Belvieu was scheduled to start in 3Q25 (150 Mb/d nameplate; ~195 Mb/d capability). The Bahia NGL pipeline is next up in 4Q25, creating more fee-based revenue for the midstream giant.

MPLX: Investors will be looking for color on the $2.38B Northwind Midstream deal, which closed on Sept. 2. Northwind adds ~150 MMcf/d of sour gas treating capacity and two acid gas injection (AGI) wells, with treating capacity slated to expand to ~440 MMcf/d by 2H26. The deal adds minimal 3Q EBITDA, but integration with MPLX’s Delaware system sets up a 4Q step-up and potential runway for growth in 2026.

Bottom line: 3Q25 earnings should showcase WMB’s West/Gulf momentum, DTM’s Haynesville growth, OKE’s NGL and refined products engine (with MB-4 a nonevent for 3Q), EPD’s fractionation tailwind vs a brief crude wobble, and MPLX’s Northwind-driven upside.

Estimated Quarterly Volumes:

Notes: 3Q25 is expressed as Q-o-Q growth from 2Q25. Rockies is the sum of Big Horn, DJ, Green River, Piceance, Powder River, San Juan, Uinta and Wind River.

- Northeast meter point samples are down 1.7% from 3Q25. The WMB – Susquehanna Supply Hub is down 6.1% and the DTM – Bluestone system is down 3.2% from 3Q25. Coterra is the largest producer behind the WMB system, accounting for 84% of its volumes. Expand Energy is the largest producer behind the DTM system and contributes 83% of the volumes, followed by 16% from Coterra.

- The Haynesville head-fake continues. Meter point samples are down 5.1% from 3Q25. EDA believes this is due to new volumes flowing on the LEG and NG3 pipelines with LEG already flowing more than 1 Bcf/d.

Calendar: