Exec Summary

Market Movers: As Delaware drilling tilts sour, the midstream moat is built on AGI wells and long-dated contracts.

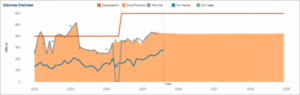

Estimated Quarterly Volumes: Continental’s growth guidance matches EDA’s forecast: modest but durable gains into 2026. ****NEW****

Calendar: The FERC Form 6 data deadline was Sep 8 so EDA has the latest volumetric & financial data for liquids pipelines.

Market Movers:

Managing sour gas is becoming a challenge for producers in the Delaware Basin. Development is shifting to the deeper Avalon and Bone Spring benches, where the associated gas has higher carbon dioxide and hydrogen sulfide content. The trend toward more sour gas production creates opportunities for midstream companies to expand their services and, in some cases, consolidate.

Handling sour gas requires specialized treating facilities to remove the CO2 and H2S streams prior to processing, plus acid gas injection (AGI) wells to dispose of the waste. While treating and cryogenic capacity can be added in a matter of quarters, AGI wells require 12–24+ months to permit, plus several months to drill and commission. The extended timeline makes AGI wells the main impediment to expansions for sour volumes. Systems that pair treating, AGI wells and takeaway nearest to sour gas benches are best positioned to capture throughput and maintain higher utilization.

Producers in the Permian remain focused on liquids, but East Daley anticipates the basin’s natural gas will grow in value as rising LNG and power demand calls on more supply. A second tailwind comes from Section 45Q carbon capture credits, which may apply to the CO₂ collected and stored from injected acid gas. Regulations and investor pressures also tilt the market toward sequestration over flaring, so we expect producers will increasingly shoulder the extra costs associated with lifting sour gas.

The moat for midstream is AGI disposal backed by long-dated dedications, which keeps upstream volumes sticky and midstream assets full. In the G&P System Analysis tool in Energy Data Studio, systems with filed or approved AGI wells are positioned to capture more pieces of the value chain, from gathering and treating through compression, disposal and processing. Gathering footprints without disposal wells or firm tolling contracts face constraints until they can secure access to AGI wells.

Midstream operators in the Delaware are converging on the same strategy. Targa Resources (TRGP), Enterprise Products (EPD), MPLX, Delek (DK) and Kinetik (KNTK) all highlight treating expansions and AGI well access to unlock sour volumes. Treating assets are also driving merger activity, from EPD’s acquisition of Piñon Midstream to KNTK’s purchase of Durango Midstream in 2024.

Which company could be the next target? East Daley’s Energy Data Studio shows that private Delaware systems owned by Salt Creek Midstream and Vaquero Midstream lack disclosed AGI wells and are running below full capacity (see the figure above for the Salt Creek G&P system). These assets offer immediate synergies when tied to a disposal node. Producers Midstream also owns a smaller sour-ready system and is advancing AGI wells alongside a processing expansion, enhancing its value as potential takeover candidate.

We expect continued AGI-focused consolidation and longer-dated sour take-or-pay contracts as midstream operators compete for control of choke points. As Delaware development tilts toward sour gas, the systems that combine treating with permitted AGI wells and reliable takeaway will set the pace for throughput and cash generation.

Estimated Quarterly Volumes:

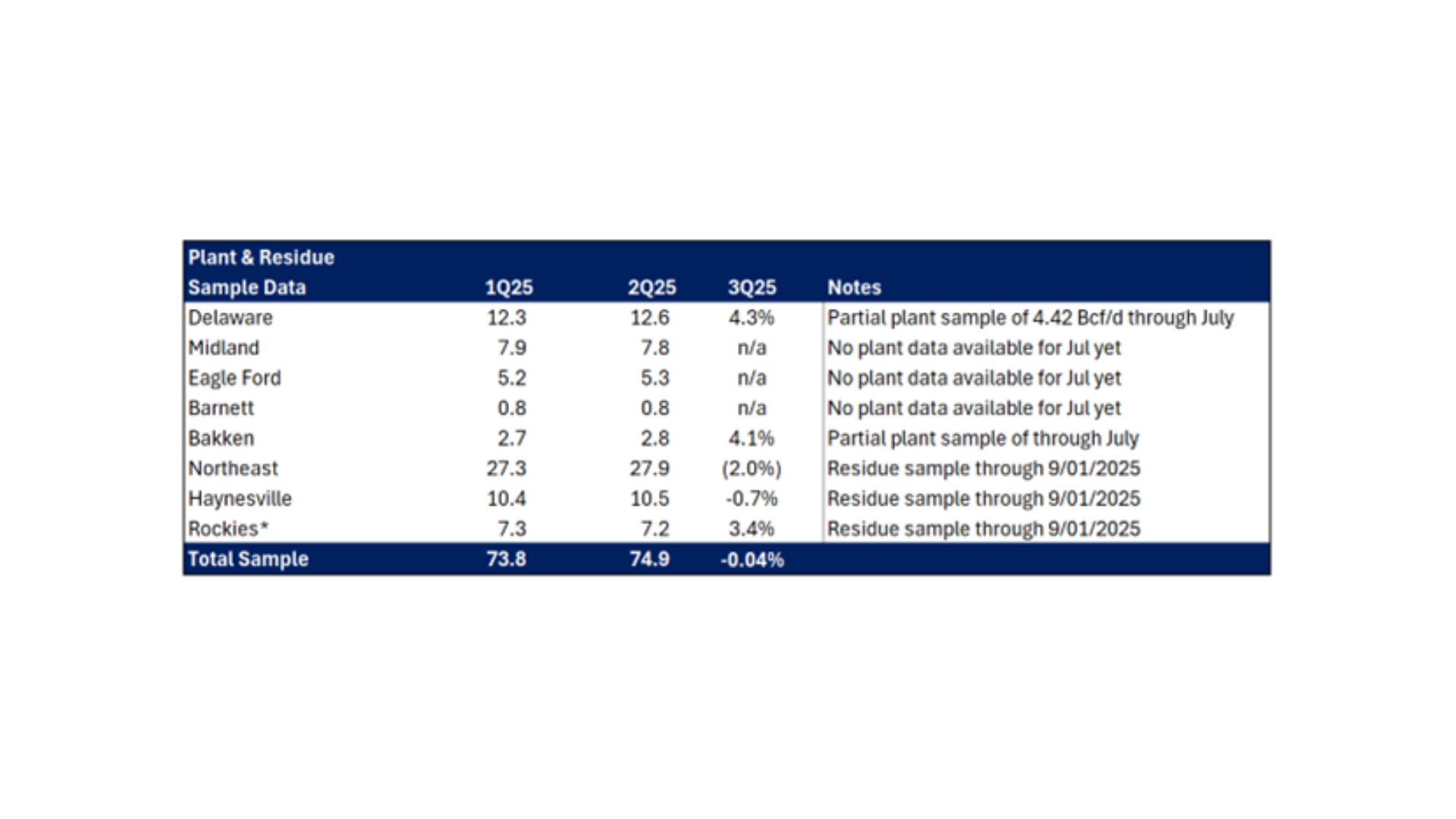

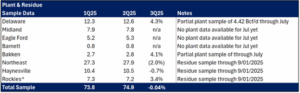

Notes: 3Q25 is expressed as Q-o-Q growth from 2Q25. Rockies is the sum of Big Horn, DJ, Green River, Piceance, Powder River, San Juan, Uinta, Wind River.

- Bakken has settled this week; plant inlets are up 4.1% Q-o-Q through July with 70% of plants reporting. The OKE – Bakken system is up 3.7% from 2Q25 and the Private – Palermo system is down 7.7% from 2Q25. The Bakken is forecast to grow 0.8% from 2Q to 3Q25. Continental Resources is one of the largest producers behind the OKE system and has guided growth of 3-6% from 2025-26.

- Haynesville meter point samples are down 0.7% Q-o-Q through September. We forecast 12% growth in Haynesville region volumes from 2Q to 3Q25. EDA does not believe that there has been a decrease in production in Haynesville rather it is LEG entering service diverting dry gas from interstate to intrastate pipelines.

Calendar: