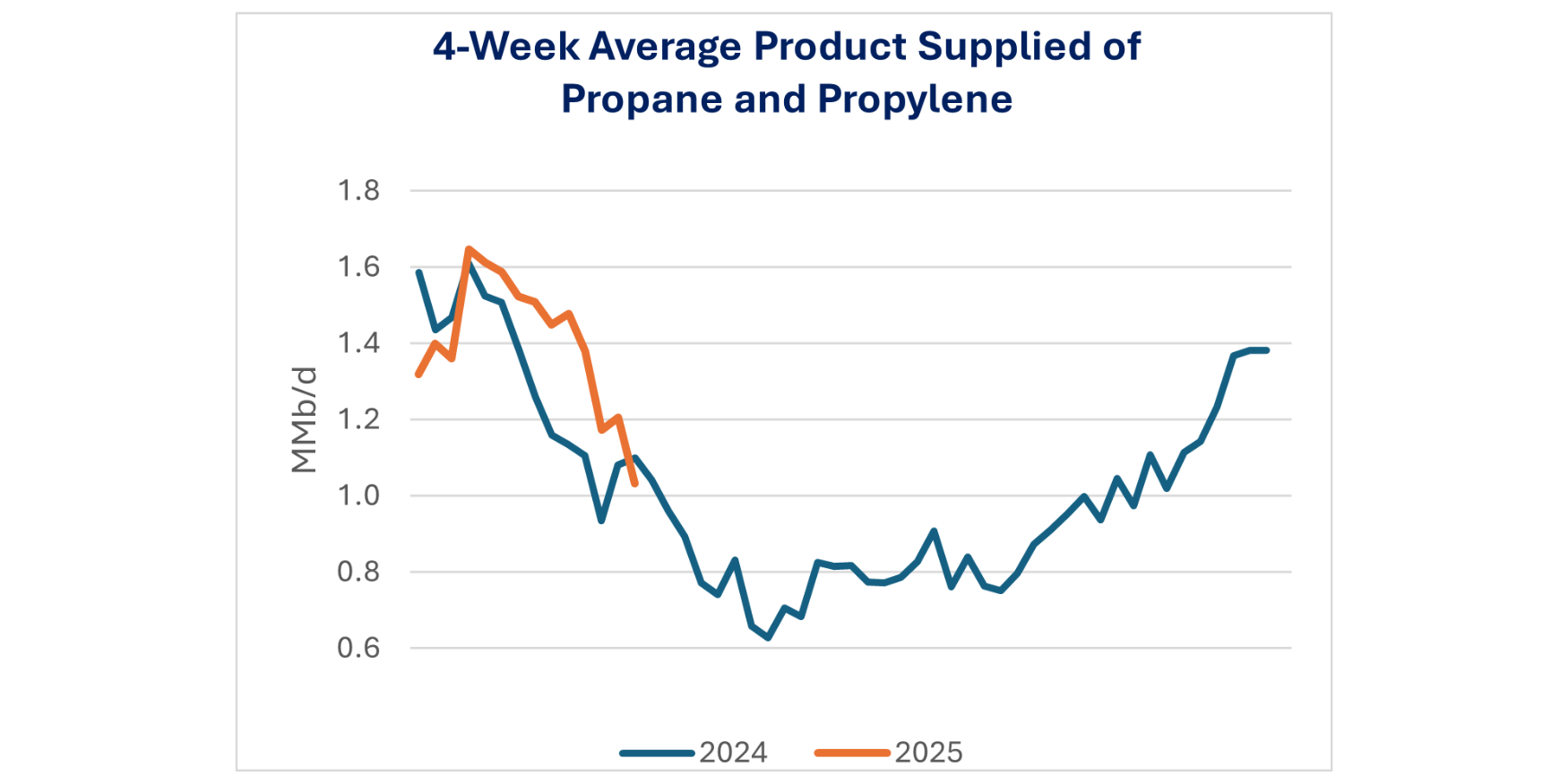

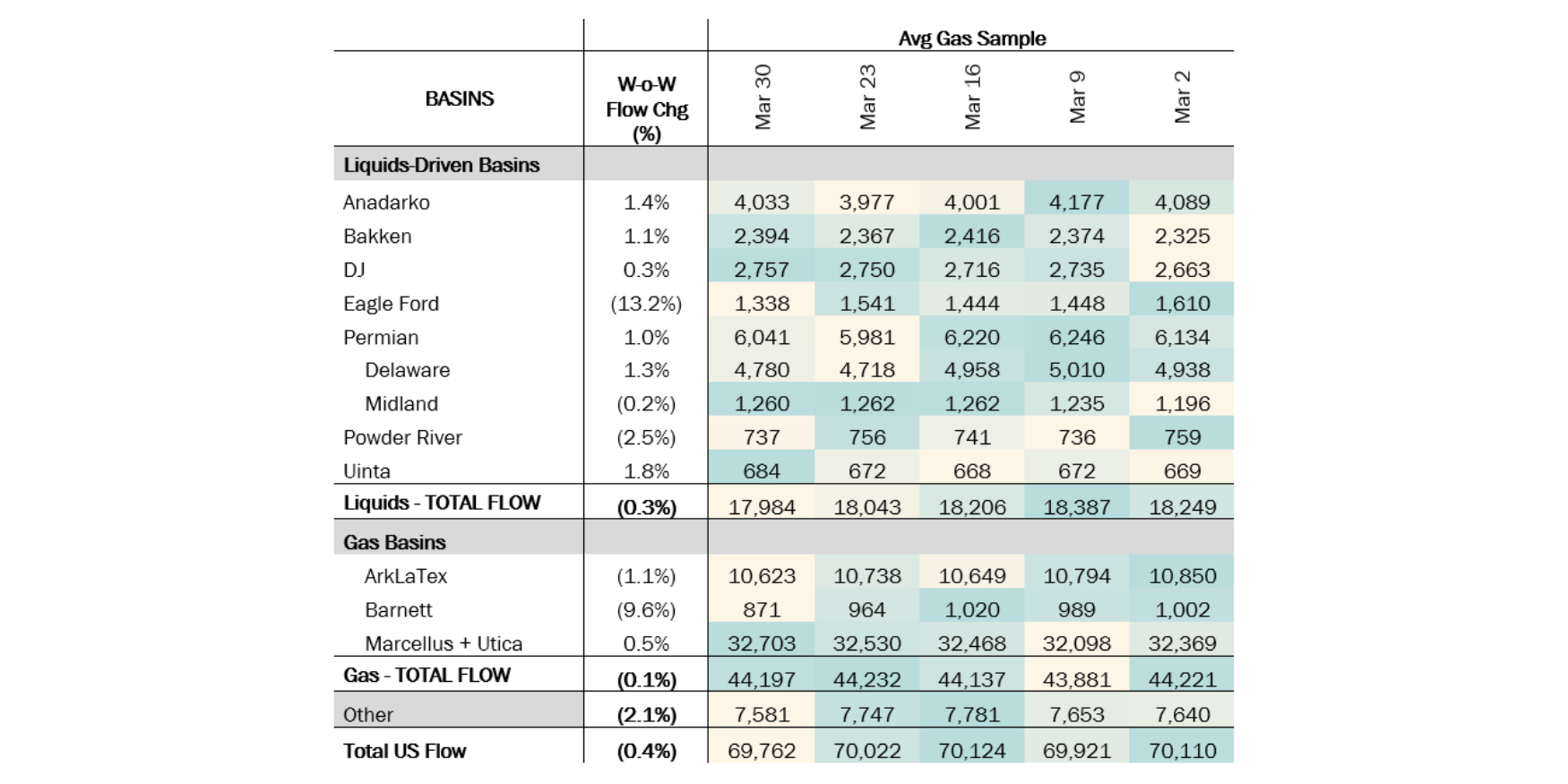

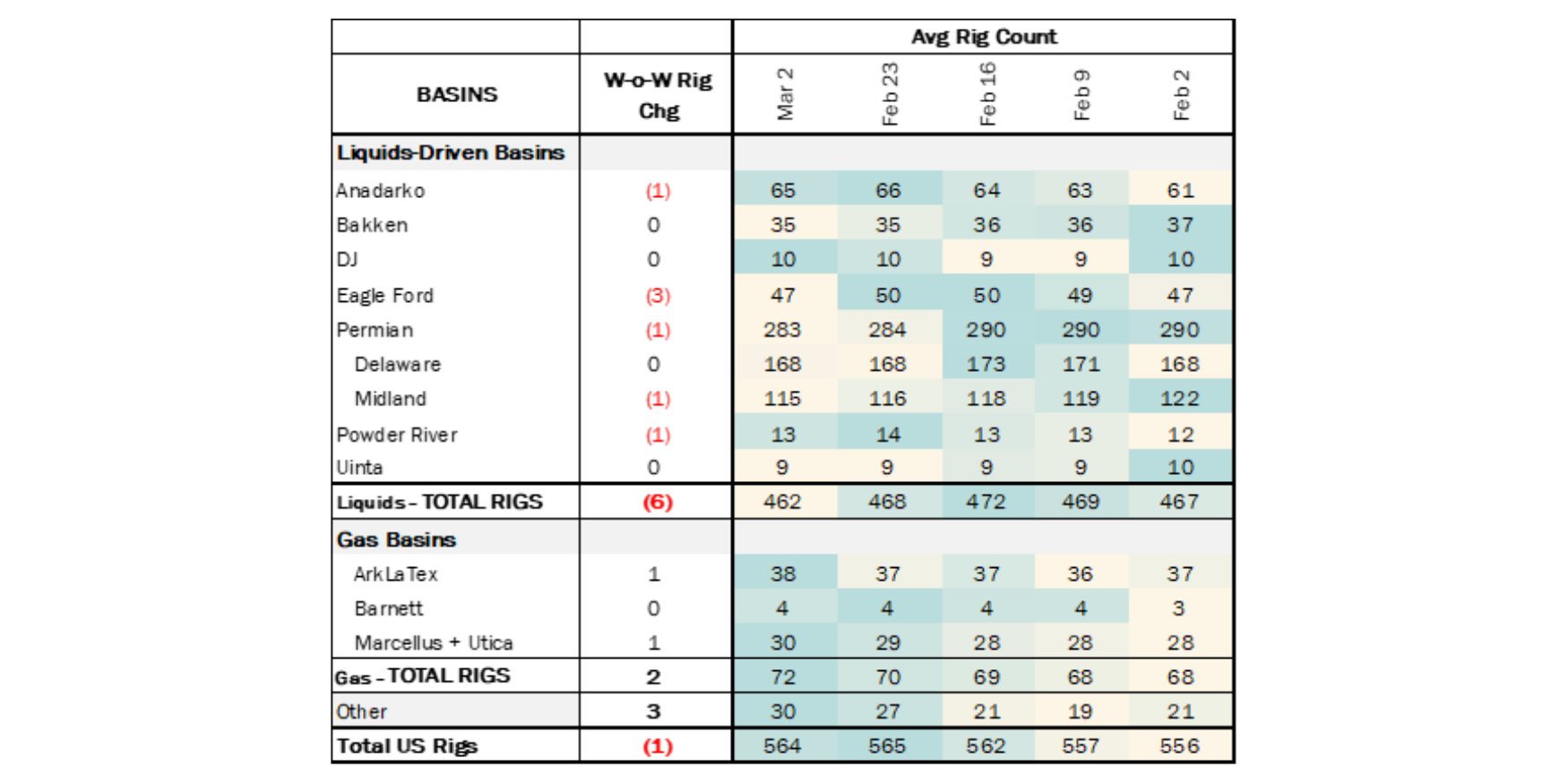

Executive Summary: Rigs: The total rig count decreased by 2 for the October 6 week, down to 568 from 570. Flows: Bakken samples rebounded by 6% (+129 MMcf/d), averaging 2.44 Bcf/d for the week as operators restarted some production following wildfires in western North Dakota. Infrastructure: NGL production in the Marcellus and Utica (Northeast) hit record levels in 2Q24 and, reading the tea leaves, we expect to see a new supply record in 3Q24. Purity Product: In its 3Q24 earnings call, Range Resources (RRC) also pointed out that NGLs it sells are priced at a premium to Mont Belvieu (refer to the chart below as illustrated on the right Y-axis).

Rigs:

The total rig count decreased by 2 for the October 6 week, down to 568 from 570. Liquids-driven basins declined by 3 rigs W-o-W.

- Permian Delaware (-2): Mewbourne Oil and EOG Resources each removed 1 rig.

- Uinta (-1): Anschutz Corporation removed 1 rig.

Flows:

Bakken samples rebounded by 6% (+129 MMcf/d), averaging 2.44 Bcf/d for the week as operators restarted some production following wildfires in western North Dakota. Fires in the Ray-Tioga, Elkhorn, and Bear Den areas caused several operators to halt production earlier in October. Bakken samples are still ~95 MMcf/d below gas receipts at the end of September.

Permian pipeline samples decreased by an average of 6.7%, due in part to maintenance on El Paso Natural Gas (EPNG) pipeline. The work at the Plains station, a key exit point for Permian gas flows, has put pressure on Waha prices, driving prices into negative territory earlier in the month.

*W-o-W change is for the two most recent weeks.

Infrastructure:

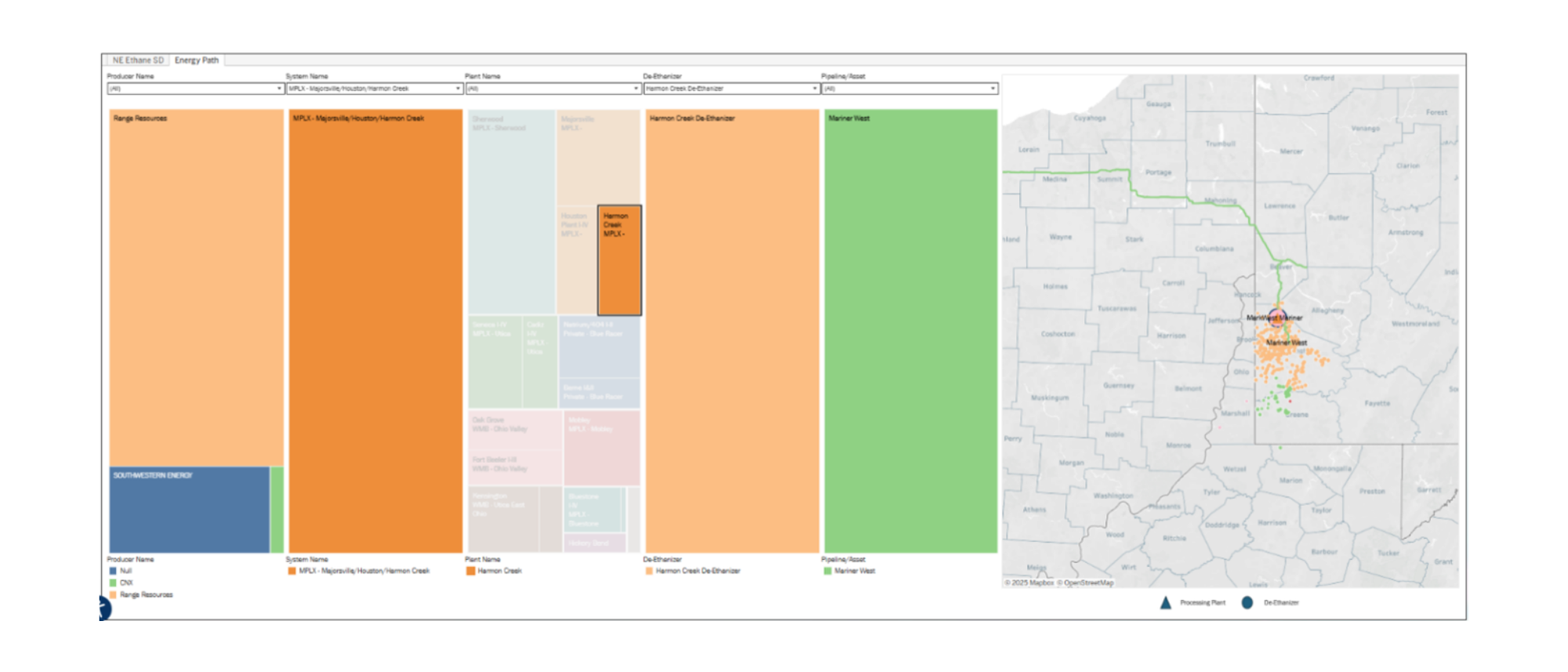

NGL production in the Marcellus and Utica (Northeast) hit record levels in 2Q24 and, reading the tea leaves, we expect to see a new supply record in 3Q24. Range Resources (RRC) just posted NGL production growth of 8.2% from 2Q24 to 3Q24 (from 103.0 to 111.5 Mb/d net NGL production).

Some of the increase in NGL production has fulfilled higher ethane demand at the Shell Monaco steam cracker in Pennsylvania, as East Daley has covered.

Most Northeast c3+ demand is exported to international buyers in the UK (SABIC), Norway (INEOS) and Sweden (Borealis) via Energy Transfer’s (ET) Mariner East NGL pipeline and Marcus Hook storage and export facility in Pennsylvania.

As shown in East Daley’s Energy Data Studio, there’s not an indefinite runway from the Northeast to Europe without more investment in LPG export capacity. Marcus Hook has about 400 Mb/d of combined ethane and LPG export capacity, ET has disclosed in prior company presentations (refer to the graph below). With an estimated 2Q24 throughput of 366 Mb/d and an early read-through from RRC of 8% Q-o-Q volume growth, we are likely soon pushing on Northeast export limits.

Gulf Coast operators including Enterprise Products (EPD), ET and Targa Resources (TRGP) have announced several expansion projects to alleviate what will be a constrained market this winter. It’s all quiet on the eastern front, however, when it comes to dock expansion details. ET has been mum of late on a previously discussed Marcus Hook expansion (see 4Q22 and 1Q23 earnings calls), making it less clear when the next project will occur. With more than 1.3 Bcf/d of natural gas supply growth forecast in our Northeast Supply & Demand product, we believe the need for a dock expansion at Marcus Hook is necessary to support Northeast production growth – both for gas and NGLs.

Purity Product Spotlight:

In its 3Q24 earnings call, Range Resources (RRC) also pointed out that NGLs it sells are priced at a premium to Mont Belvieu (refer to the chart below as illustrated on the right Y-axis). The premium has widened in 3Q24 as Mont Belvieu prices have been pressured in part by tight dock capacity. As explained above, the Northeast NGL producers may soon face a similar pricing dynamic if an expansion project is not announced soon. As East Daley’s NGL Hub Model shows, most c3+ supply is met by international, not local demand.

Data Points & Product Release Calendar:

-1.png)

-1.png)

-3.png)