Executive Summary: Rigs: The total rig count decreased by 7 for the September 29 week, down to 565 from 572. Flows: Pipeline samples rose W-o-W to ~68.5 Bcf/d for the October 13 week. Infrastructure: Four months ago, East Daley was bearish ethane price. Purity Product Spotlight: Weekly propane and propylene exports fell off a cliff in October ’24.

Rigs:

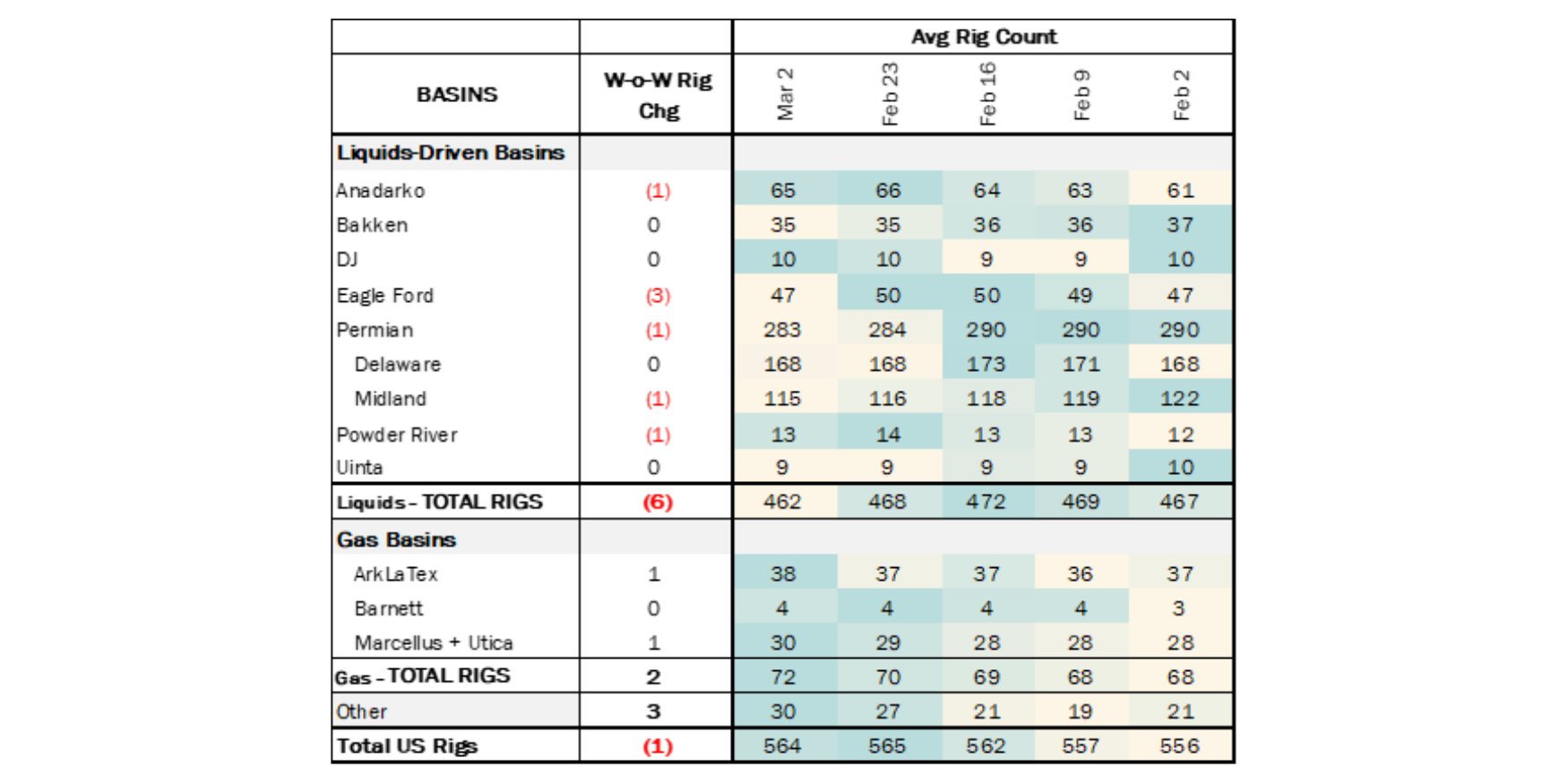

The total rig count decreased by 7 for the September 29 week, down to 565 from 572. Liquid-driven basins declined by 1 rig W-o-W.

- Anadarko (+1): Camino Natural Resources.

- Bakken (+1): Grayson Mill Operating.

- Permian (-5):

- Delaware (-3): Chevron, Devon Energy, Exxon.

- Midland (-2): Exxon, Occidental Petroleum.

- Uinta (+2): Ovintiv, Finley Resources.

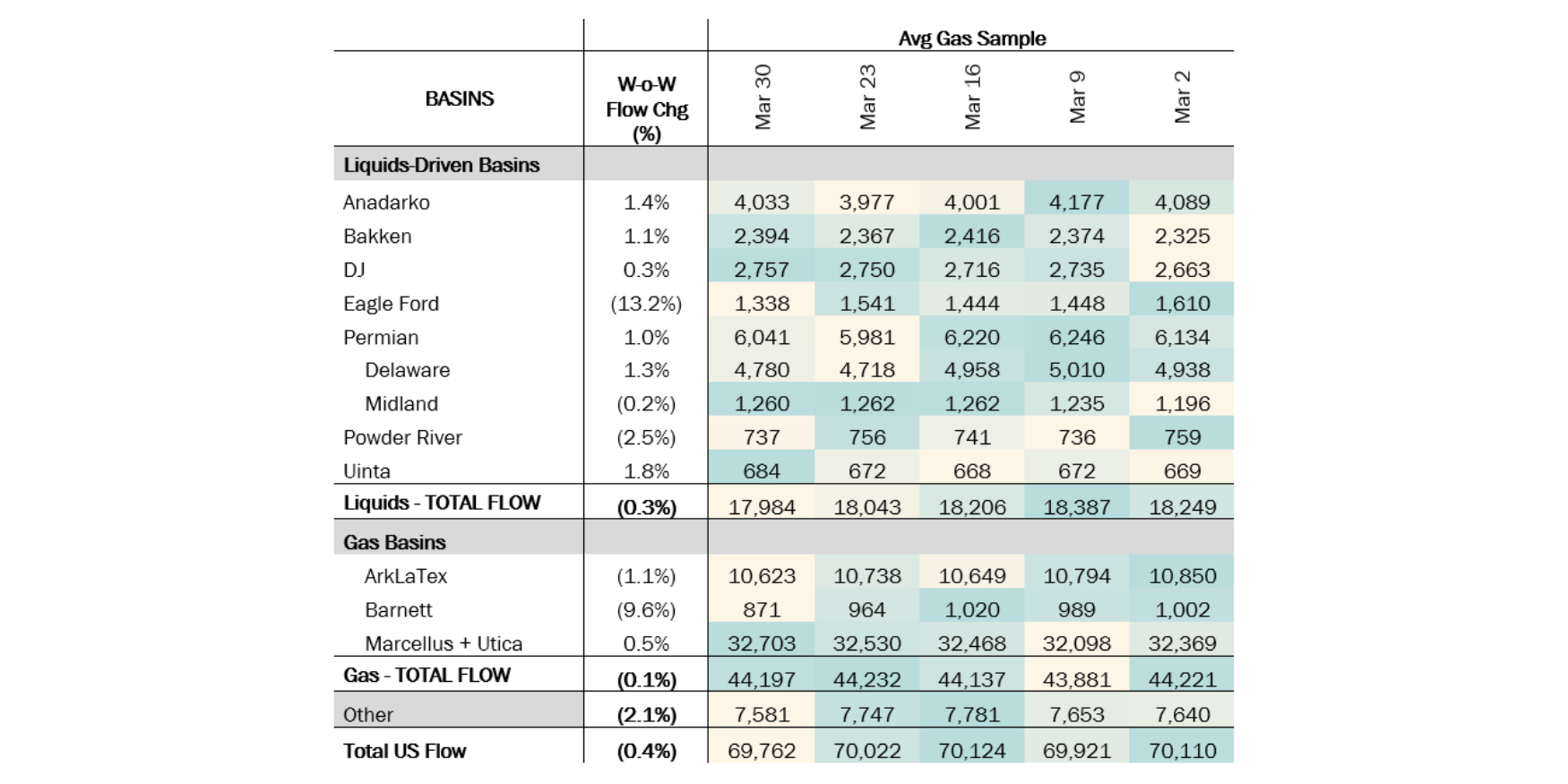

Flows:

Pipeline samples rose W-o-W to ~68.5 Bcf/d for the October 13 week. Wildfires in North Dakota's Bakken region impacted oil and gas production, down 5% (123 MMcf/d) W-o-W. Fires in the Ray-Tioga, Elkhorn, and Bear Den areas caused several operators to halt production temporarily to protect infrastructure. East Daley expects the fires will lead to only short-term production shut-ins.

Hurricane Milton caused significant disruptions to oil and gas production when it passed through the Gulf of Mexico. Chevron evacuated its Blind Faith platform, which produces 65 Mb/d, and shut down operations in preparation for the storm. Based on Bureau of Safety and Environmental Enforcement data, nearly 49% of offshore gas production was shut-in as operators evacuated staff and implemented safety protocols during the last two hurricanes. For the week of October 6, GOM pipe samples fell ~400 MMcf/d, reflecting the reduced operations, but samples showed signs of returning to normal, up 3% in the latest week.

Infrastructure:

Four months ago, East Daley was bearish ethane price. In our early June ’24 Ethane Supply & Demand Report, we predicted robust ethane supply coming out of the Permian would put downward pressure on the forward curve through October ’25, given there is no meaningful incremental demand coming online until mid-‘25.

Four months ago, East Daley was bearish ethane price. In our early June ’24 Ethane Supply & Demand Report, we predicted robust ethane supply coming out of the Permian would put downward pressure on the forward curve through October ’25, given there is no meaningful incremental demand coming online until mid-‘25.

Over the past four months, the Mont Belvieu forward curve has declined by an average of 7% from November ’24-October ’25 (refer to the graph below). The ethane supply glut of course wasn’t driven by high ethane prices, but rather low (often negative) Permian Waha gas prices, which incentivized ethane recovery to the max. A low ethane price is better than a negative price – the lesser of two evils.

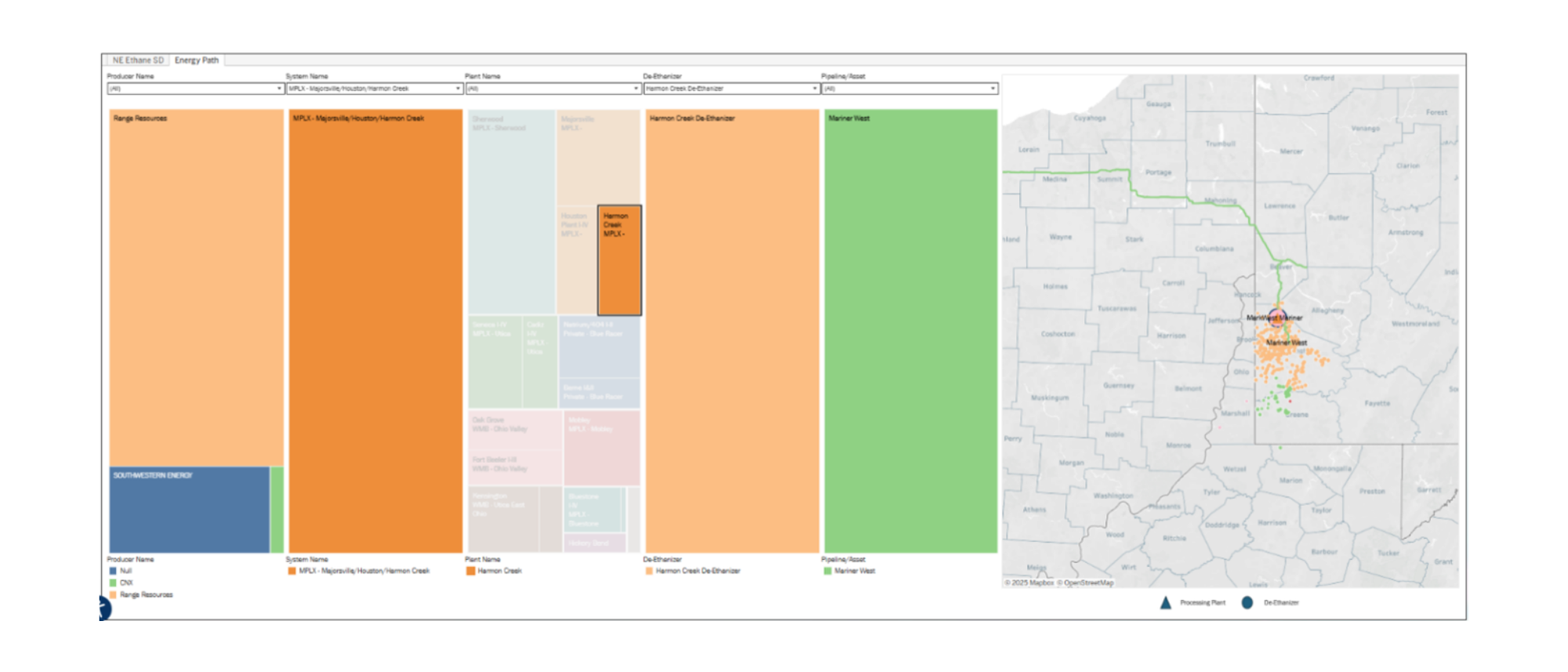

Fast-forward to today, and the dynamic has shifted. The 2.5 Bcf/d Matterhorn Express Pipeline is operational and ramping up throughput. There is now room to reject ethane into the gas stream, and operators long ethane are incentivized to send more on the new gas egress pointed toward Houston and Gulf Coast markets.

ramping up throughput. There is now room to reject ethane into the gas stream, and operators long ethane are incentivized to send more on the new gas egress pointed toward Houston and Gulf Coast markets.

In fact, data available in Energy Data Studio suggests gas plant operators began increasing ethane rejection in August ‘24. The bar chart above shows M-o-M ethane growth from Energy Information Administration (EIA) data. The green bars show M-o-M ethane growth based on plant data in Texas and New Mexico. The state data leads the EIA-reported data by a month, with a strong positive correlation.

With more than 25% of plant data for August ’24, it appears likely we will see a decline in ethane supply that month, a necessary adjustment to ethane stocks well in excess of the norm dating back to 2019. The next update of plant data in EDA's Energy Data Studio is scheduled for October 28.

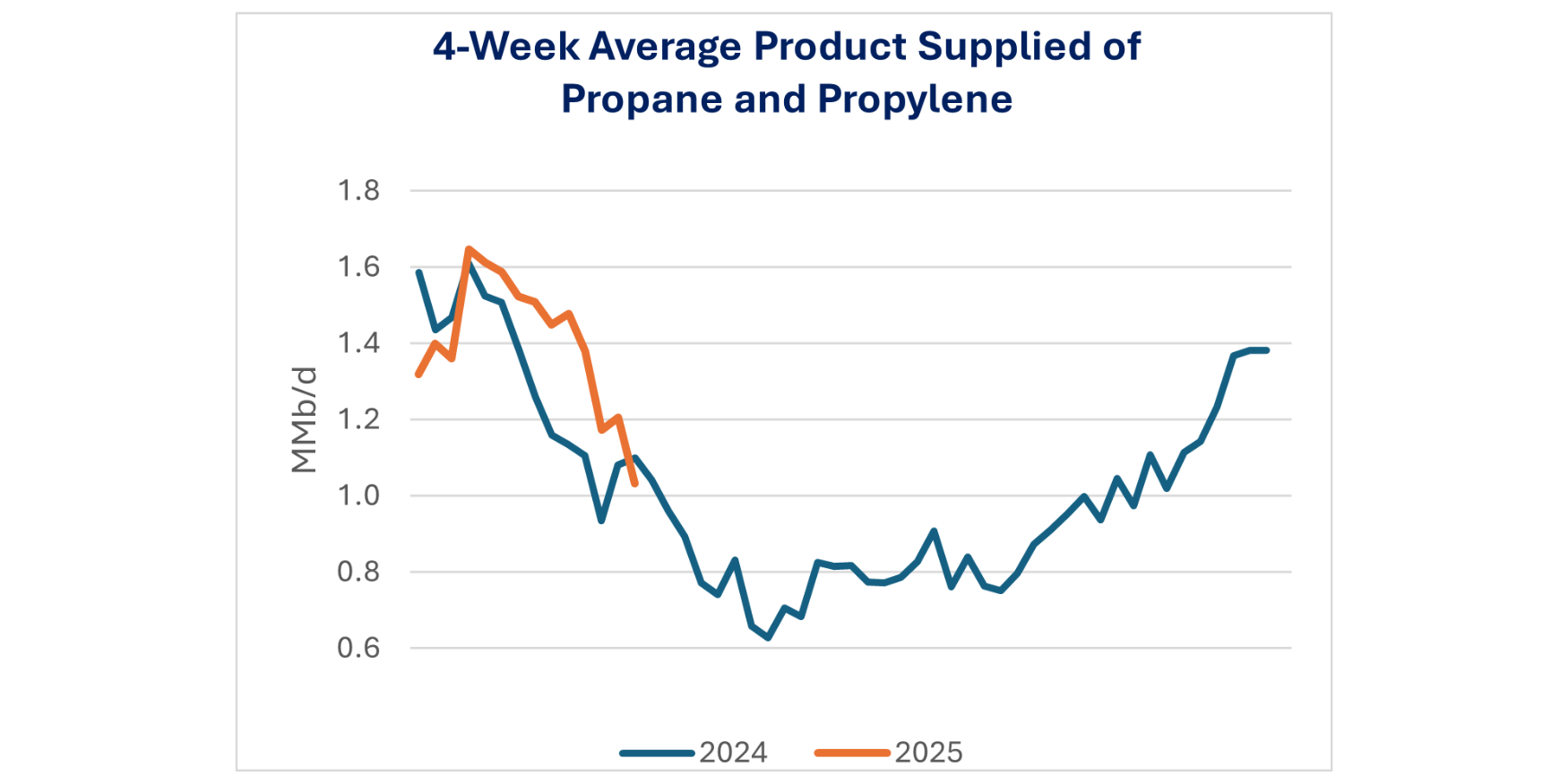

Purity Product Spotlight:

Weekly propane and propylene exports has fallen off a cliff in October ’24. We estimate year-to-date LPG exports through September are higher in 2024 than ’23 by 11%. October ’24 exports however are 12% lower than October ’23, which has led to propane inventories spiking to 103.1 MMbbl. Hurricane Milton had a likely impact on delaying LPG loadings, and we expect to see the weekly number rebound for the next data set for the week ending 10/18.

Data Points & Product Release Calendar:

-1.png)

-1.png)

-3.png)