Executive Summary: Rigs: The total US rig count decreased 6 rigs W-o-W to 582 for the March 24 week, down from 588. Flows: The US interstate gas sample was flat W-o-W for the week of April 7. Infrastructure: East Daley has released the latest March ‘24 production forecasts for Crude, Gas and NGLs, with the main changes taking place in the Northeast and Permian regions. Purity Product: The weighted average Mont Belvieu NGL price per gallon is up 9.5% Q-o-Q (see chart below), providing upside to midstream companies with commodity-linked G&P contracts.

Rigs:

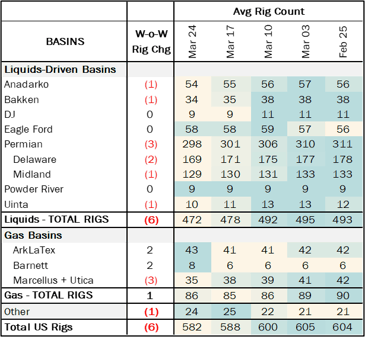

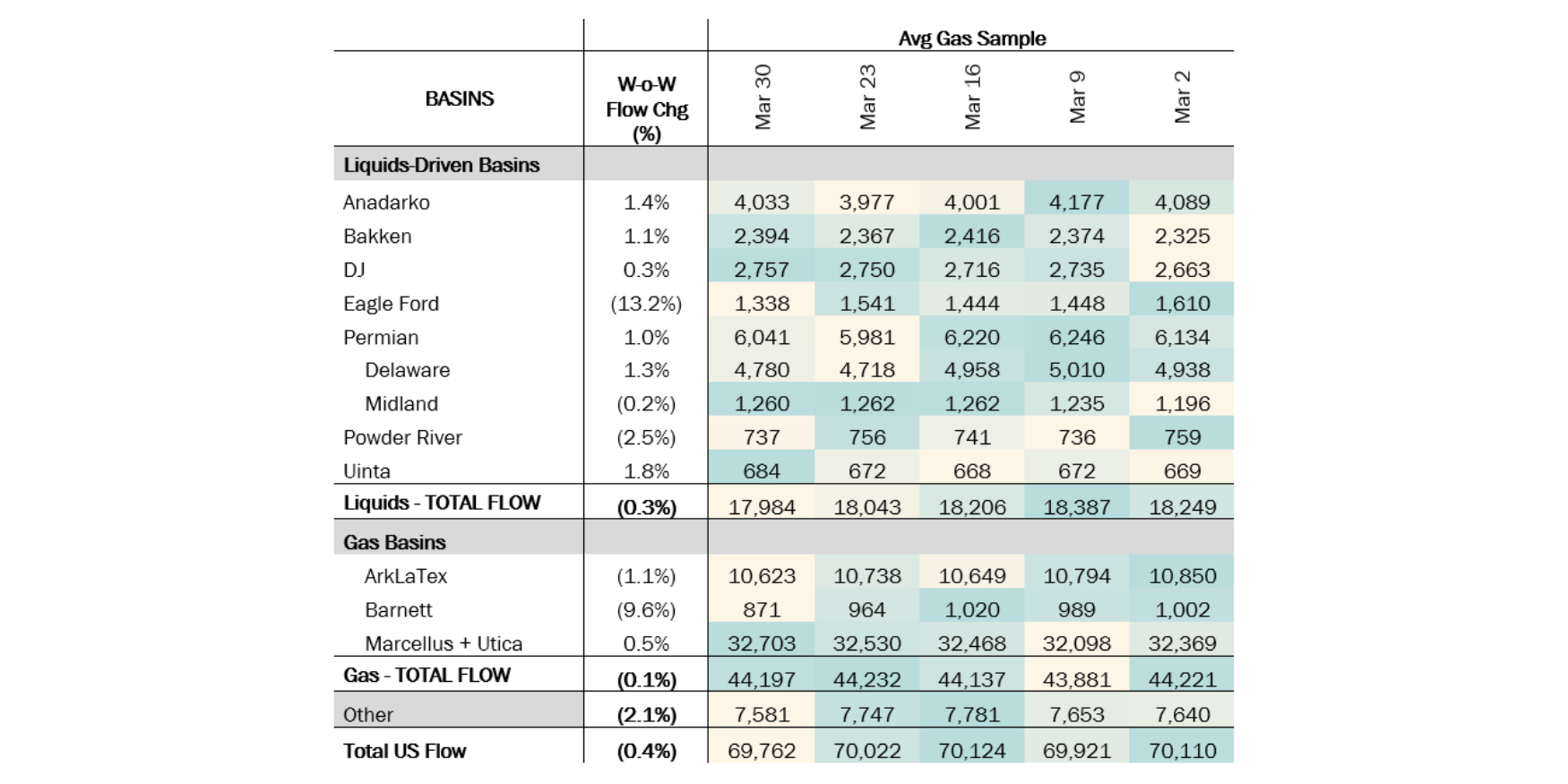

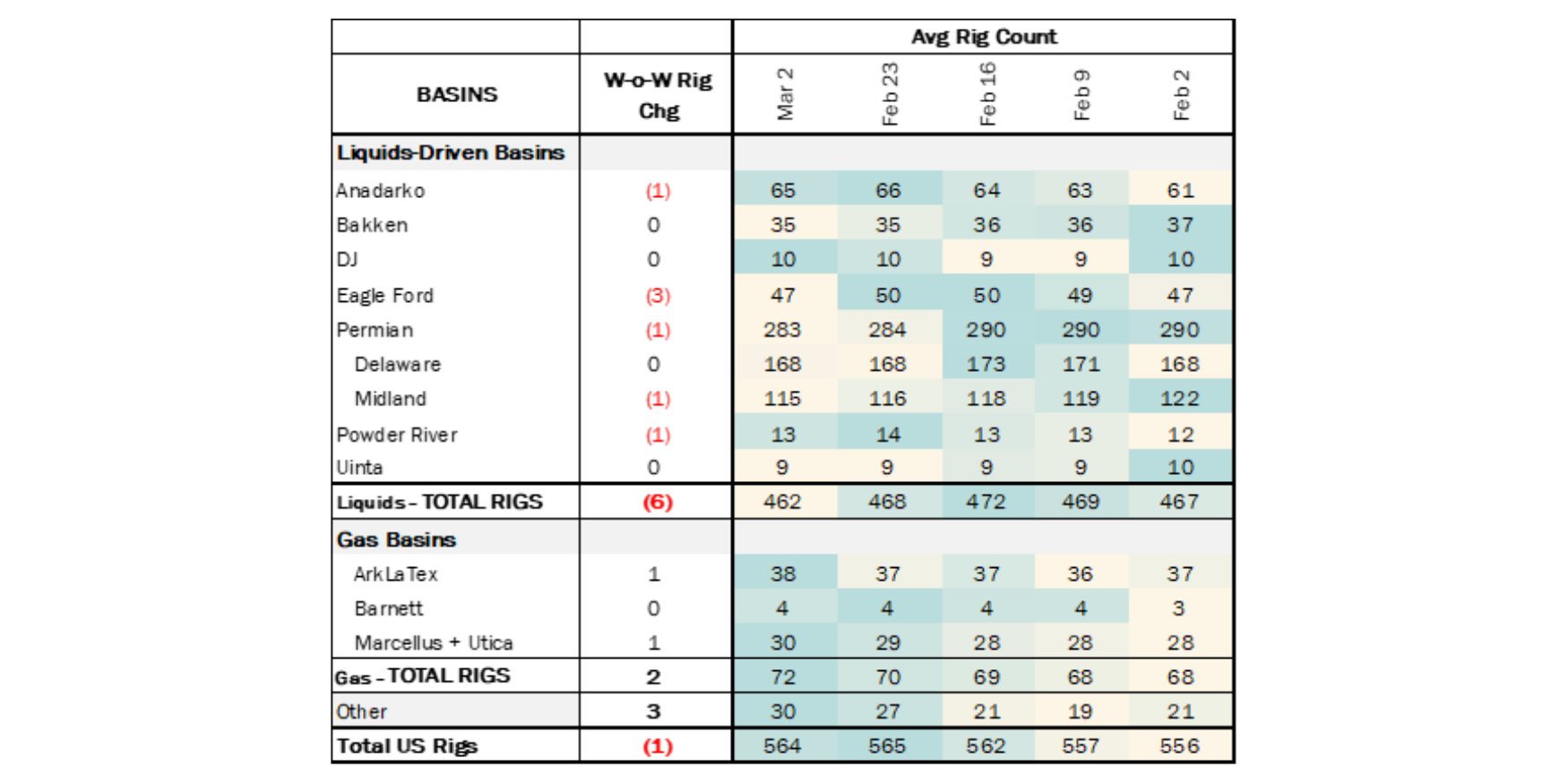

The total US rig count decreased 6 rigs W-o-W to 582 for the March 24 week, down from 588. Liquids-driven basins accounted for most of the changes with the Anadarko, Bakken and Uinta each losing 1 rig W-o-W. The Permian Basin lost 3 rigs W-o-W, with the Delaware losing 2 rigs and the Midland dropping 1 rig.

In the Midland, Pioneer Natural Resources dropped 1 rig from its program, moving to 20 from 21 rigs. In the Delaware, Marathon and Exxon both idled 1 rig, down to 2 and 8 rigs respectively. Other operators dropping a rig W-o-W include Mack Energy (Anadarko), Continental Resources (Bakken) and XCL Resources (Uinta).

Flows:

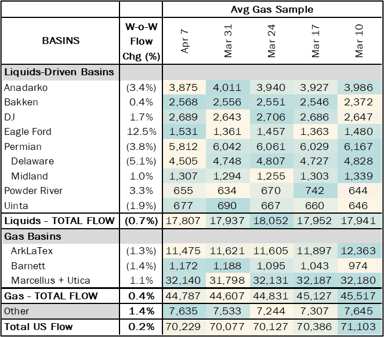

The US interstate gas sample was flat W-o-W for the week of April 7. Gas-driven basins were relatively flat with some puts and takes between the Haynesville (ArkLaTex) and the Northeast (Marcellus + Utica).

Gas samples in liquids-targeted basins fell slightly by 0.7% W-o-W. The primary driver is a drop in the Delaware Basin gas sample. Ongoing maintenance on the El Paso gas pipeline continues to restrict supply, and we are seeing a dip in volumes as a result. Additionally, Gulf Coast Express has announced future maintenance which should keep Waha trading at a steep discount until linefill begins on the new Matterhorn pipeline.

The Eagle Ford flow sample is up 12.5%. However the flow sample coverage is about 25% with a large error range. We have seen no corroborating evidence via price or flows through infrastructure to confirm any real variability in supply.

Infrastructure:

East Daley has released the latest March ‘24 production forecasts for Crude, Gas and NGLs, with the main changes taking place in the Northeast and Permian regions.

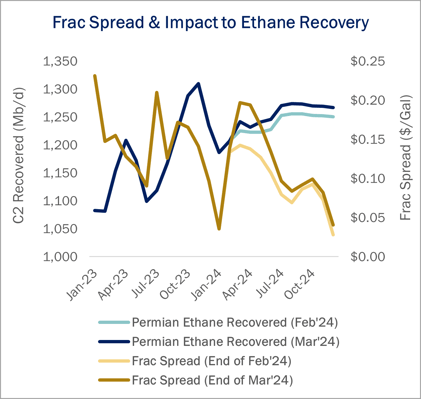

In the Northeast, our ethane recovery forecast decreased along with our gas production forecast. We have revised our supply outlook lower as producers like EQT have curtailed production and delayed start-up of new wells in response to low natural gas prices. However, we have increased our NGL supply outlook in the Permian in response to falling Waha prices.

Waha gas traded at an average of $0.30/MMBtu for February and March in response to tight overall takeaway and maintenance restrictions on some pipelines. Kinder Morgan (KMI) has been conducting maintenance on the El Paso pipeline system in the Delaware Basin since March, limiting some flows. Waha spot prices have traded negative at times in response. With more maintenance scheduled, including work on the Gulf Coast Express Pipeline, the market is pricing in low Waha prices until 2H24.

As a result, the frac spread has widened to Mont Belvieu C2 in our latest updates. With ethane prices holding more firm at Mont Belvieu, the incentive to extract has increased.

The figure above compares EDA’s February and March forecasts for Permian NGL production. In the February ‘24 forecast, NGL production from April to YE24 averaged about 3,079 Mb/d for the Permian.

For the March ’24 forecast, EDA has increased the production outlook considering the drop in Waha prices. We now expect total NGL production in the Permian to average 3,103 Mb/d from April to YE24, about +23 Mb/d vs last month’s forecast (see figure).

A higher frac spread between Mont Belvieu C2 and Waha gas prices has historically incentivized more ethane recovery. Hence, we have also increased ethane recovery in the Permian to average 1,260 Mb/d from April to YE24 in our March ’24 forecast (+17 Mb/d vs the February ’24 forecast of 1,244 Mb/d). EDA’s updated NGL volumes outlook by PADD and basin can be found in our latest Purity Product Forecast dashboard.

Purity Product Spotlight:

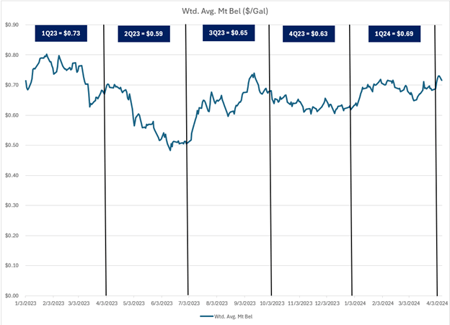

The weighted average Mont Belvieu NGL price per gallon is up 9.5% Q-o-Q (see chart below), providing upside to midstream companies with commodity-linked G&P contracts. Enterprise Products (EPD), Targa Resources (TRGP), and EnLink Midstream are a few companies with commodity exposure, and we have baked that upside (net of hedges) into our Financial Blueprint model updates ahead of the 1Q24 earnings season.

-1.png)

-1.png)

-3.png)