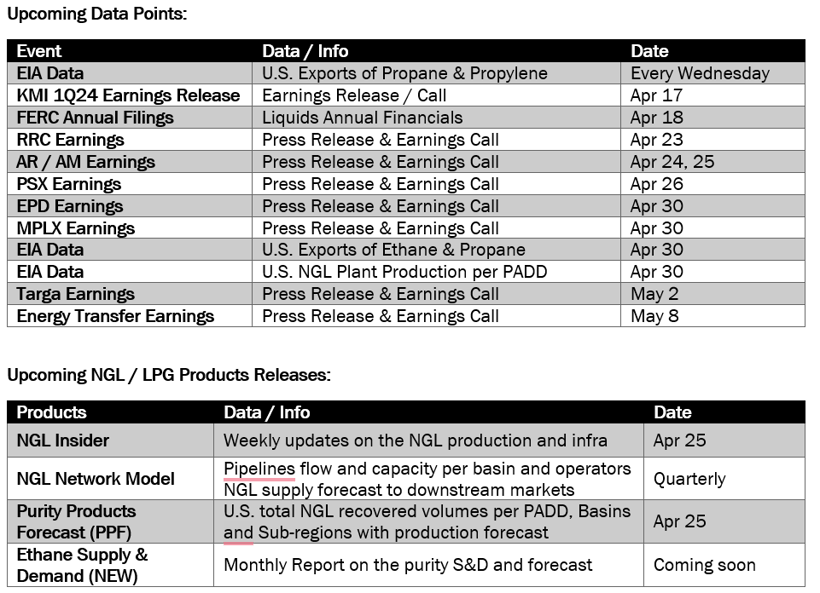

Executive Summary: Rigs: The total US rig count stayed flat W-o-W at 582 rigs for the March 31 week. Flows: The US interstate gas sample fell 2.8% W-o-W for the April 14 week, mainly driven by gas-focused basins. Infrastructure: Moss Lake Partners surprised the market with its proposed DeLa Express rich-gas pipeline linking Permian gas supply to Port Arthur, TX and Cameron Parish, LA demand markets. Purity Product Spotlight: Enterprise Products (EPD) and Energy Transfer (ET) will report 1Q24 earnings results on Apr 30 and May 8, potentially shedding light on 1Q24 ethane export volumes out of PADD 1 (ET’s Marcus Hook dock) and PADD 3 (EPD’s Morgan’s Point and ET’s Nederland docks).

Rigs:

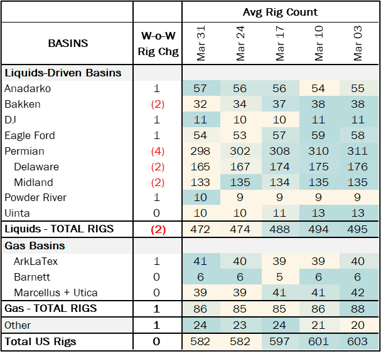

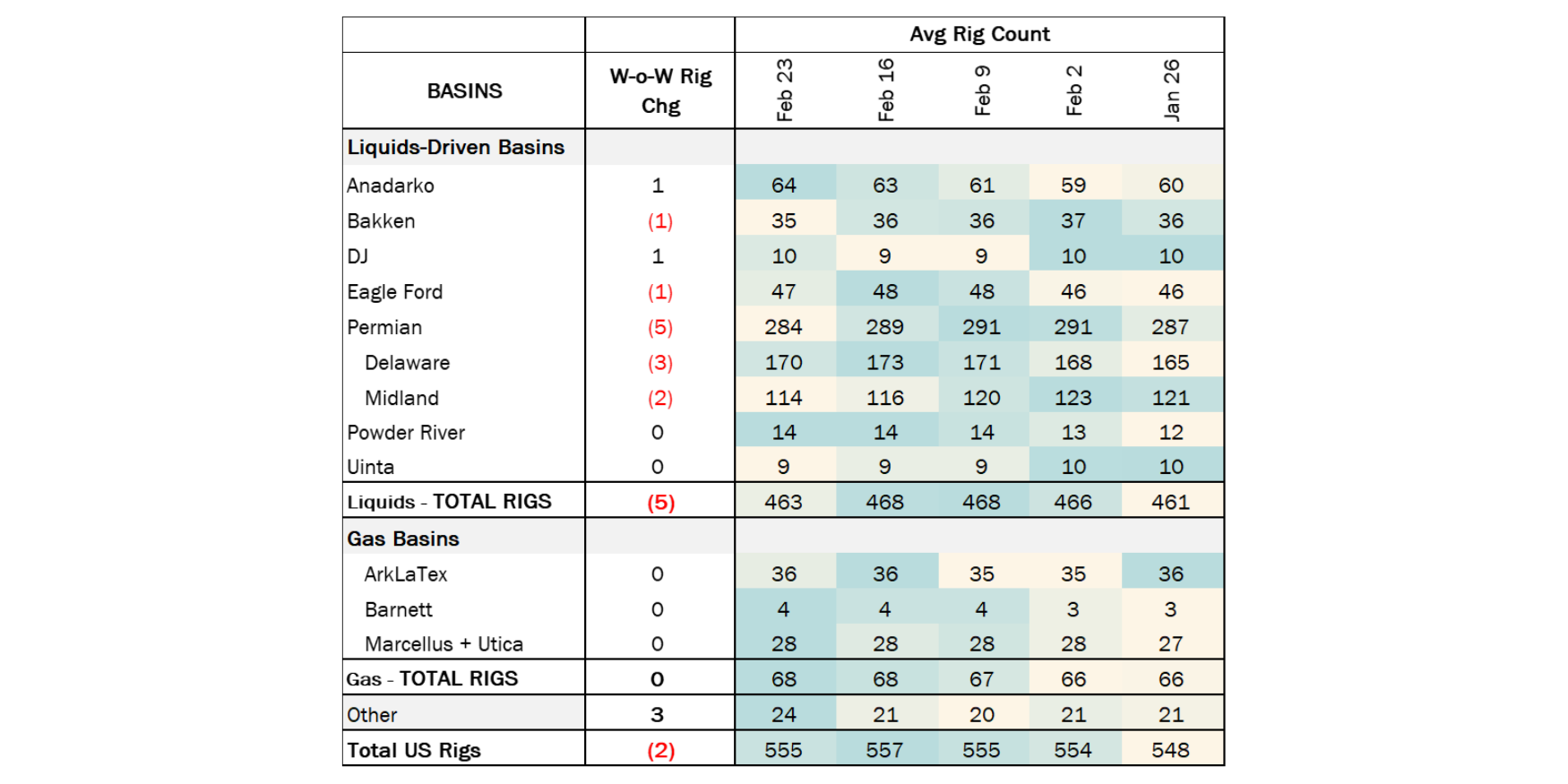

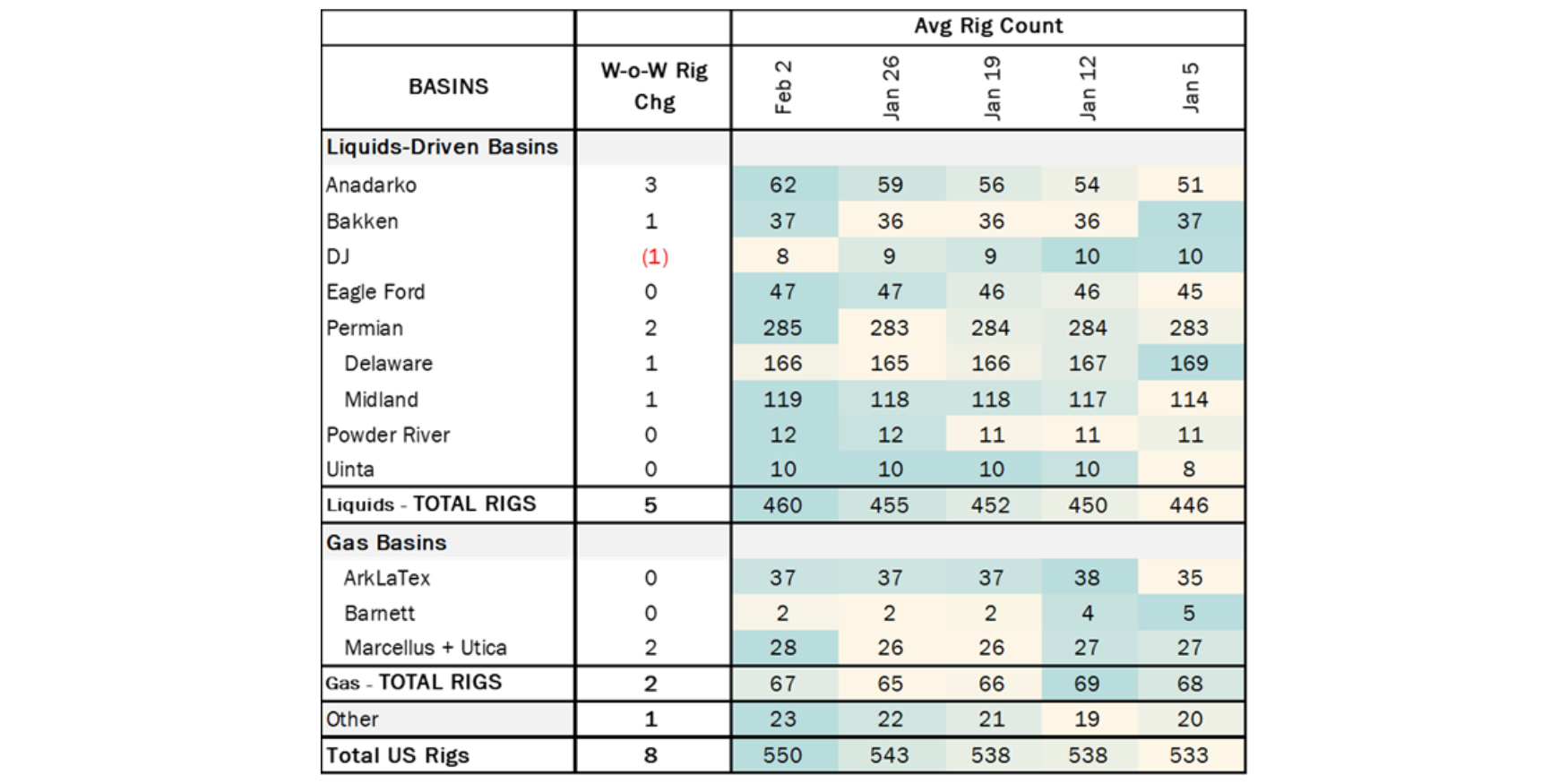

The total US rig count stayed flat W-o-W at 582 rigs for the March 31 week. However, liquids-driven basins did see rigs decline W-o-W to 472 rigs total, down 2 from 474 rigs the previous week. The Permian led the change by losing 4 rigs, 2 in the Delaware and 2 in the Midland. The Bakken also lost 2 rigs. The Anadarko, DJ, Eagle Ford and Powder River basins each added 1 rig W-o-W.

In the Delaware, Chevron (CVX) and Exxon (XOM) each dropped 1 rig W-o-W. Chevron now has 9 rigs in the Delaware and Exxon has 6. In the Midland, Diamondback Energy (FANG) and Pioneer Natural Resources (PXD) each shed 1 rig. Hess and Chord Energy each dropped 1 rig from systems in the Bakken.

Flows:

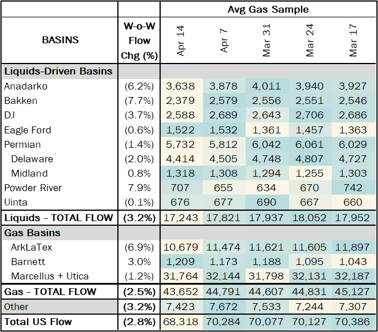

The US interstate gas sample fell 2.8% W-o-W for the April 14 week, mainly driven by gas-focused basins. Ongoing declines in the ArkLaTex (Haynesville) and Northeast samples dropped the total sample in the gas-driven regions to 2.5% W-o-W.

Production in the Haynesville have been sliding for six weeks, with some pipeline reporting underperformance recently as physical volumes have dropped faster than nominations. Producers in the Northeast like EQT are still limiting production and delaying the start of new wells.

In liquid-driven basins, the gas sample fell 3% due to ongoing maintenance on the El Paso pipeline system. Flows will continue to be constrained as we expect additional maintenance on Gulf Coast Express soon.

Infrastructure:

Moss Lake Partners surprised the market with its proposed DeLa Express rich-gas pipeline linking Permian gas supply to Port Arthur, TX and Cameron Parish, LA demand markets. The project would also provide access to Hackberry NGL, Moss Lake’s affiliated NGL export project, according to the project’s filing with the Federal Energy Regulatory Commission (FERC).

Downstream NGL assets in Cameron Parish include Targa Resources’ (TRGP) Lake Charles fractionator, according to EDA’s NGL Network Model. With nameplate capacity of 55 Mb/d, the Lake Charles frac splits ethane and propane for the local petrochemical market. Moss Lake’s NGL project also could access international markets via LPG exports.

DeLa Express is in the early days, and reminds EDA of the Bluegrass Pipeline and Moss Lake joint venture formed between Williams (WMB) and Boardwalk Pipeline more than a decade ago. That project was designed to transport growing NGL supply from the Northeast to a newly constructed fractionator, expanded NGL storage facilities, and an LPG export terminal. The companies ultimately dissolved the JV in September 2014 due to a lack of customer commitments. Interest in the project waned as WTI oil prices fell from more than $105/bbl in June ’14 to the $30s by January ‘16.

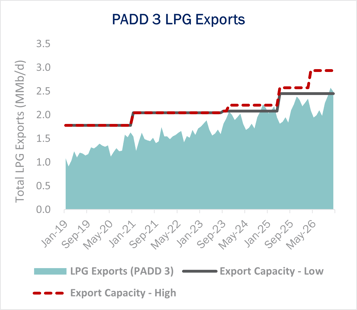

New LPG export projects from Energy Transfer (ET) and Enterprise Products (EPD) will help meet growing LPG supply from the Permian Basin. Based on EDA’s NGL Network Model, those projects will add 730 Mb/d of capacity and ease export tightness until 2027, when growing NGL supply will catch up with infrastructure capacity once again.

As noted in the FERC filing, DeLa Express has a planned in-service date of July 2028. Whether Moss Lake or another party, we expect steady supply growth will require more investments in export dock capacity.

Purity Product Spotlight:

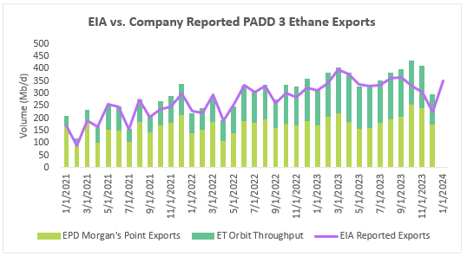

Enterprise Products (EPD) and Energy Transfer (ET) will report 1Q24 earnings results on Apr 30 and May 8, potentially shedding light on 1Q24 ethane export volumes out of PADD 1 (ET’s Marcus Hook dock) and PADD 3 (EPD’s Morgan’s Point and ET’s Nederland docks).

The purple line in the chart shows a dip in 4Q23 exports, followed by a rebound in January ’24, according to EIA data. It is unclear why exports declined in 4Q23 to the lowest level since 3Q22; the decline was likely due to lower spot volume demand.

ET’s Nederland ethane export dock is fed by its Orbit ethane pipeline. The Orbit assets are owned by a JV with Satellite Petrochemical USA, a subsidiary of Chinese-based Satellite Chemical Co. The project is supported by a long-term 150 Mb/d contract to feed Satellite’s ethane petrochemical crackers in China’s Jiangsu Province.

-1.png)

-1.png)