Executive Summary: Rigs: The US total rig count decreased by 2 for the August 18 week, down to 563 from 565. Flows: In the Anadarko Basin, flows on NGPL and Northern Natural Gas Pipeline are up, likely from 50 rigs active in the basin over the last month. Infrastructure: The Permian and Williston basins are both constrained by inadequate gas egress capacity. Purity Product Spotlight: Exports of propane and propylene are up 10% in August ’24 vs August ’23 and up 6% QTD vs the prior year.

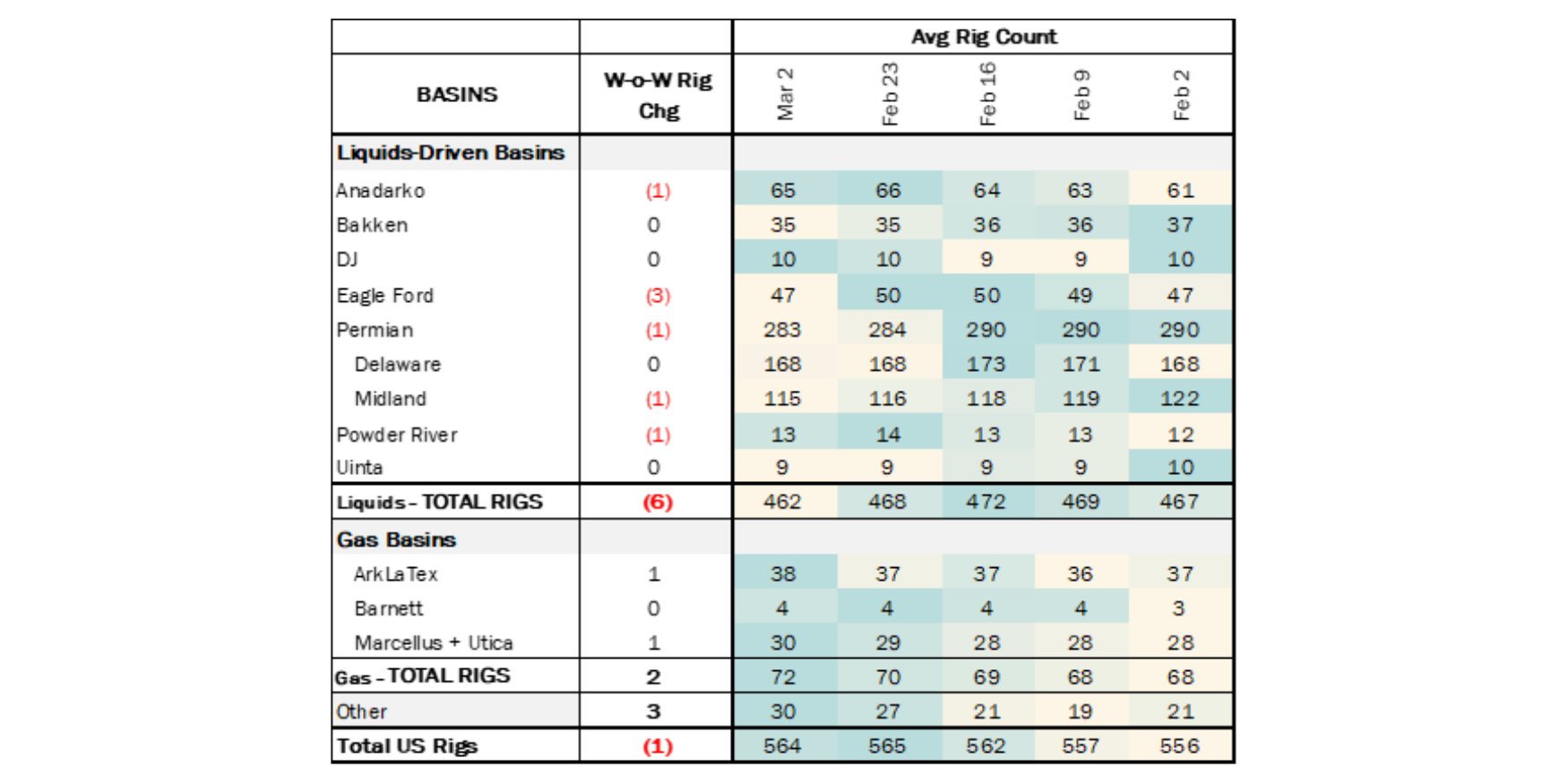

Rigs: The US total rig count decreased by 2 for the August 18 week, down to 563 from 565. Liquids-driven basins saw a decrease of 4 rigs, moving the count from 464 to 460. The Bakken and DJ basin counts each decreased by 2, whereas the Permian Basin lost 4 rigs on the week. On the other hand, the Anadarko Basin gained 3 rigs and the Powder River Basin rig count increased by 1.

In the Bakken, Continental Resources and Grayson Mill Operating LLC each dropped 1 rig. In the DJ Basin, Chevron and GMT Exploration each saw a loss of 1 rig. In the Delaware, Mewbourne Oil, EOG Resources and Chevron each dropped 1 rig. In the Midland, operator Civitas Resources laid down 1 rig.

Flows: In the Anadarko Basin, flows on NGPL and Northern Natural Gas Pipeline are up, likely from 50 rigs active in the basin over the last month. A force majeure east of 302 remains in place, limiting eastbound flows towards Louisiana until the end of September. In the Bakken, the gas sample increased by 121 MMcf/d from flows on the Northern Border Pipeline; 82% of this increase is associated with the North Roosevelt compressor station. This could potentially guide to increased production on the KMI – Bakken system which has currently 3 active rigs on the basin.

The Waha hub remains constrained as operators await the startup of Matterhorn. The Permian saw a small decrease in flows as some locations on the El Paso pipeline continue to be under scheduled maintenance. Both the Guadalupe and North Mainline stations will continue to see an average of 460 MMcf/d of reduced capacity across September. On the other side, the ArkLaTex and the Northeast saw a flat trend on the week.

*W-o-W change is for the two most recent weeks.

Infrastructure: The Permian and Williston basins are both constrained by inadequate gas egress capacity. But when it comes to managing ethane, that is where most of the similarities end.

In the Permian, ethane production has hit record highs to avoid low gas prices and leave as much space as possible on constrained gas pipes ahead of the Matterhorn pipeline start-up. While gas takeaway is also constrained in the Bakken play, much of the ethane is rejected back into the gas stream because the in-basin netback price is “out-of-the-money” compared to gas, given high transportation costs to market.

The decision to reject more Bakken ethane is reflected in the heating content of gas flowing on Northern Border Pipeline (NBPL). In recent years we have seen higher heating content on NBPL as inbound flows from Canada have been displaced by ethane-rich gas from the Bakken.

The egress dynamics will change for both natural gas and NGLs as new projects come online. On the natural gas side, TC Energy’s (TRP) Bison Express reversal project will add up to 300 MMcf/d of swing egress capacity. Bison Express opens the route from the Kurtz meter station in Morton County, ND to the Buffalo meter in Campbell County, WY.

The NGL scenario will change as ONEOK’s (OKE) Elk Creek Expansion adds 135 Mb/d of capacity by 1Q26. Another 85 Mb/d of capacity will come online when Kinder Morgan (KMI) finishes its planned conversion of the Double H crude oil pipeline out of the Bakken to NGL service.

For NGL production of 444 Mb/d, the basin has three main egress routes: Vantage, Elk Creek and OKE Bakken. In the basin there are six fractionators that produce C3 and C4+, which are trucked or railed to local market. Propane can also be injected into Alliance Pipeline to be processed on Aux Sable in Chicago. East Daley Analytics is planning to deliver a monthly Supply and Demand report that will allow clients to take a detailed dive into how purity products move from the Bakken to Canada and the Conway and Mont Belvieu markets.

Purity Product Spotlight: Exports of propane and propylene are up 10% in August ’24 vs August ’23 and up 6% QTD vs the prior year. This is keeping a lid on propane and propylene stocks at 93.1 MMbbl through August 23. As noted in our 3Q24 NGL webinar, we expect meaningful growth from Permian producers as soon as Matterhorn linefill begins sometime between mid-September and early October (see below).

The producers highlighted in green have actually revised up their production guidance for 4Q24 since earlier this year. For example, Chevron (CVX) said on its 2Q24 earnings call: “With strong momentum in our operating portfolio and predictable results from our non-operated and royalty acreage, we now expect full year production growth of about 15% and fourth quarter production to average around 940,000 barrels per day.” This compares to 867 MMboe/d in 4Q23 and CVX’s original 4Q24 guidance of 900 MMboe/d in February ’24. This will not impact peak storage into the fall, but it will make for a tight LPG export market into the 2024-25 winter months.