Executive Summary: Rigs: The US total rig count decreased by 12 for the August 11 week, down to 544 from 556. Flows: Anadarko Basin samples rose 3.0% W-o-W after the end of pipeline maintenance. Infrastructure: Matterhorn pipeline start-up could slow Permian ethane recovery. Purity Product: Early Texas and New Mexico plant data indicates ethane production declined from May to June ’24 by almost 2%.

Rigs:

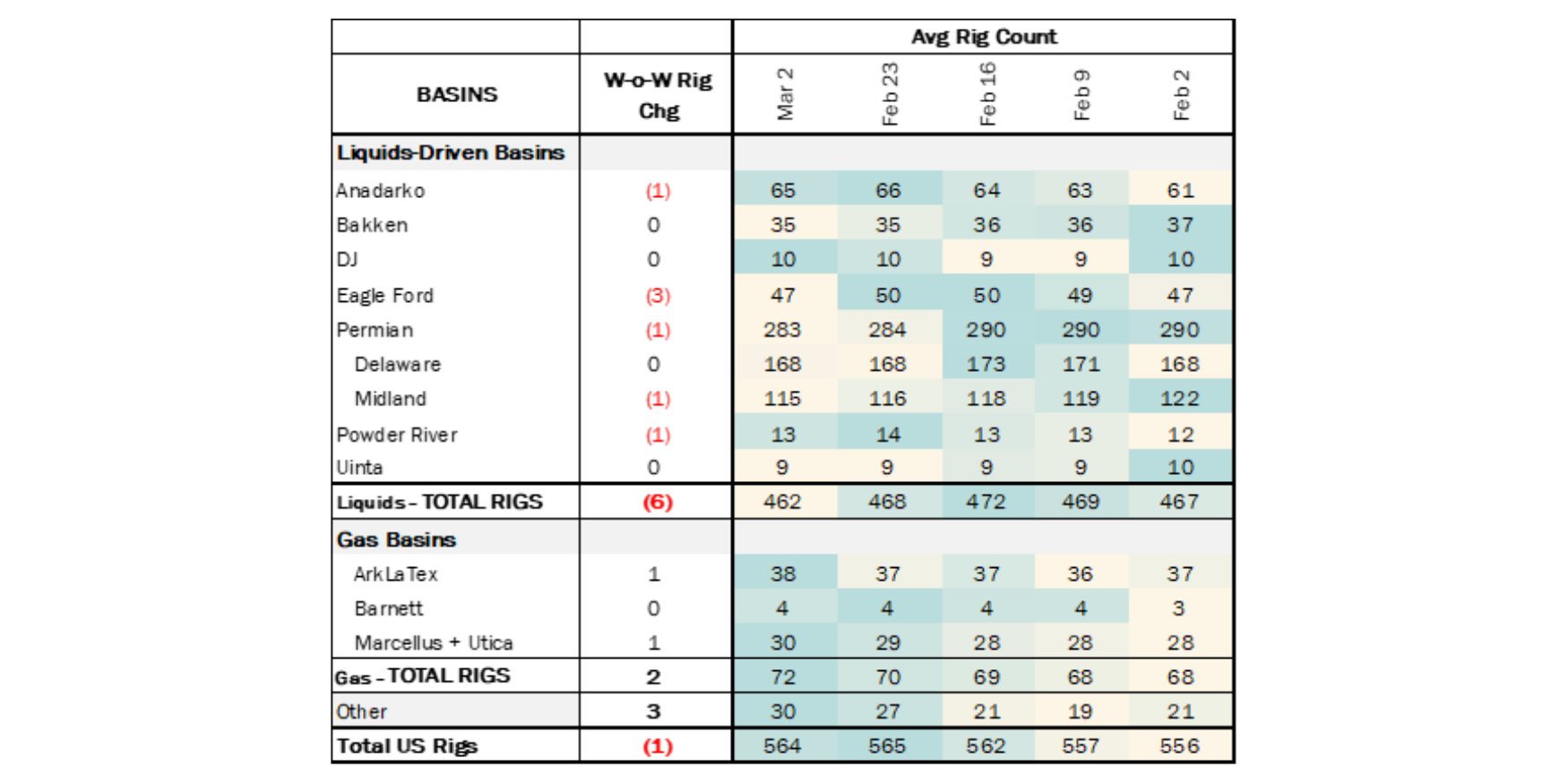

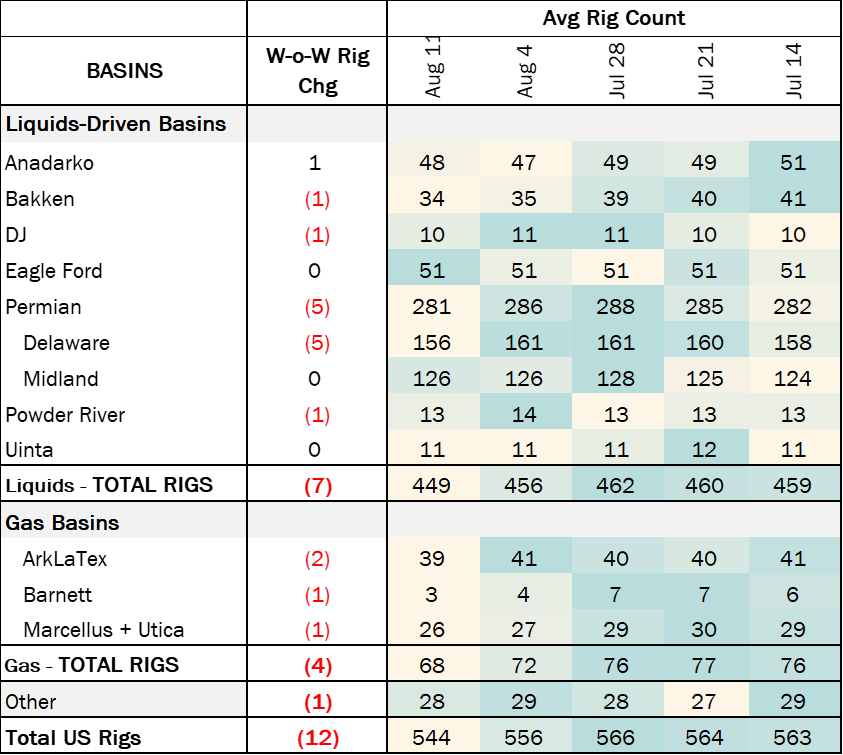

The US rig count decreased by 12 for the August 11 week, down to 544 from 556. Liquids-driven basins saw a loss of 7 rigs, moving the count from 456 to 449. The Bakken, DJ and Powder River basins each lost 1 rig, whereas the Permian Basin saw a decrease of 5 rigs, all based in the Delaware Basin. The Midland held steady at 126 rigs.

In the Bakken, operator Iron Oil removed 1 rig. In the DJ, operator H&R Well Services removed 1 rig. In the Delaware, Mewbourne Oil pulled 2 rigs, and EOG Resources, ConocoPhillips and Exxon each released 1 rig. In the Powder River Basin, Rockies Resources Holdings dropped 1 rig.

Flows:

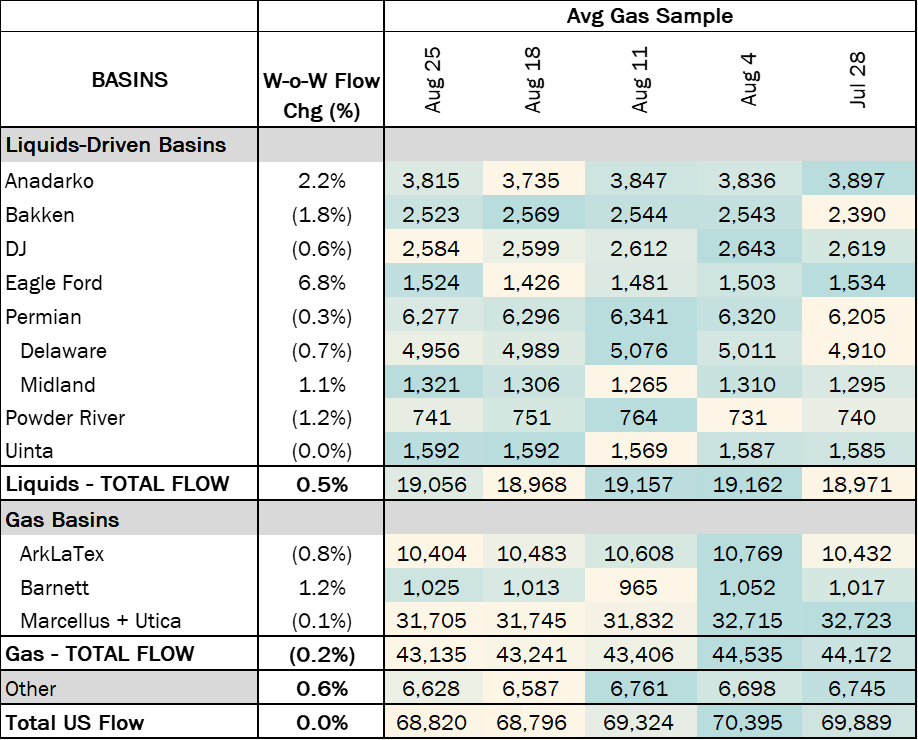

Anadarko Basin pipeline samples increased 3% W-o-W, likely due to the the finalization of scheduled maintenance on the central NGPL system. The work on NGPL reduced available capacity by 34% the week before. Utilization on Midcontinent Express Pipeline increased 15% W-o-W for rerouted gas from the NGPL’s Liberty County, TX compressor station that has set a limit to the eastbound capacity.

The Permian pipeline sample was unchanged W-o-W, as producers in the basin are waiting for Matterhorn to begin operations. The EPC contractor responsible for the Matterhorn Express Pipeline completed the “Golden Weld” on the system last week. Presumably, this marks the completion of physical pipeline construction for the project and expected linefill will commence by mid-September or early October.

The Northeast is relatively flat W-o-W though down 700 M-o-M, partly due to production cuts by EQT. The ArkLaTex region sample declined by 1% W-o-W. The decline is distributed across multiple pipelines, which could be an indicator of a slight decline in production.

*W-o-W change is for the two most recent weeks.

*W-o-W change is for the two most recent weeks.

The Permian pipeline sample was unchanged W-o-W, as producers in the basin are waiting for Matterhorn to begin operations. The EPC contractor responsible for the Matterhorn Express Pipeline completed the “Golden Weld” on the system last week. Presumably, this marks the completion of physical pipeline construction for the project and expected linefill will commence by mid-September or early October.

The Northeast is relatively flat W-o-W though down 700 M-o-M, partly due to production cuts by EQT. The ArkLaTex region sample declined by 1% W-o-W. The decline is distributed across multiple pipelines, which could be an indicator of a slight decline in production.

Infrastructure:

East Daley presented our 3Q24 NGL webinar, "Natural Gas Liquids Heading into a Super-Volatility Cycle" on August 28. We covered how NGLs had the pole position on hydrocarbon growth during 1H24 because of incentives to extract ethane from the egress-constrained Permian Basin.

This dynamic will change once Matterhorn Express Pipeline comes online. We expect Matterhorn to start operations between September 15 and October 1, allowing gas and crude production to grow significantly into 4Q24. In the short term, we expect less ethane extraction as Matterhorn supports Waha gas prices and narrows the frac spread. In the long term, more ethane will be required to meet international demand, and the 150+ Mb/d of ethane trapped in North Dakota is a call option with no expiration.

This dynamic will change once Matterhorn Express Pipeline comes online. We expect Matterhorn to start operations between September 15 and October 1, allowing gas and crude production to grow significantly into 4Q24. In the short term, we expect less ethane extraction as Matterhorn supports Waha gas prices and narrows the frac spread. In the long term, more ethane will be required to meet international demand, and the 150+ Mb/d of ethane trapped in North Dakota is a call option with no expiration.

EDA forecasts domestic ethane demand to be 5% higher in 2024 vs ’23. The next significant demand growth will occur when the CP Chem QatarEnergy facility (Golden Triangle Polymers plant) starts in mid-2026 in Orange County, TX. This will be followed by another ethane cracker in Plaquemines, LA backed by Shintech, a subsidiary of Japan's Shin-Etsu Chemical. The Shintech project is targeting start-up in fall/winter 2027. Regarding international demand, the next infrastructure expansions that will move the needle on exports are (i) the expected 25 Mb/d refrigeration expansion at Energy Transfer's (ET) Marcus Hook facility in July ’25 and (ii) the 120 Mb/d expansion for Enterprise's (EPD) Neches River facility with an in-service of October ’25.

Purity Product Spotlight:

An early look at EDA’s plant data for the states of Texas and New Mexico indicates ethane produced from processing plants declined from May to June ’24 by almost 2%.

The set is incomplete, yet early data shows pockets of slightly less ethane recovery at plants owned by EnLink Midstream (ENLC) and ET. Delaware sub-basin ethane recoveries are flat so far from May to June ’24, based on the available data.

Data Points & Product Release Calendar: