Executive Summary: Rigs: The US total rig count decreased by 2 for the July 28 week, down to 557 from 559. Flows: The total interstate gas meter sample is down 1.5% W-o-W, driven by declines in the Haynesville and Marcellus. Infrastructure: NGL takeaway capacity is extremely tight right now from the Permian Basin, but that dynamic is about to change. Purity Product: Ethane production from processing plants has hit record highs for three months straight.

Rigs:

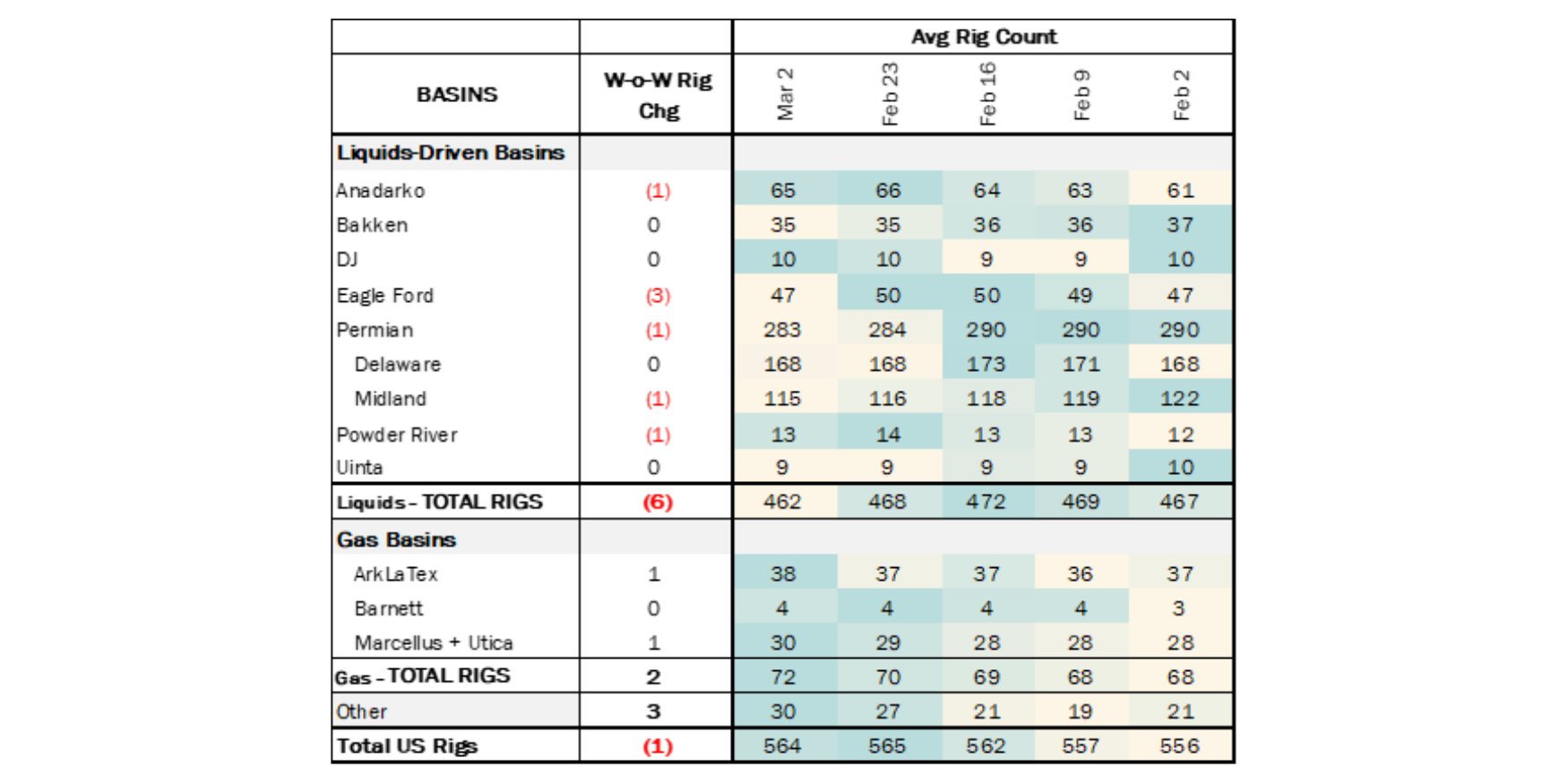

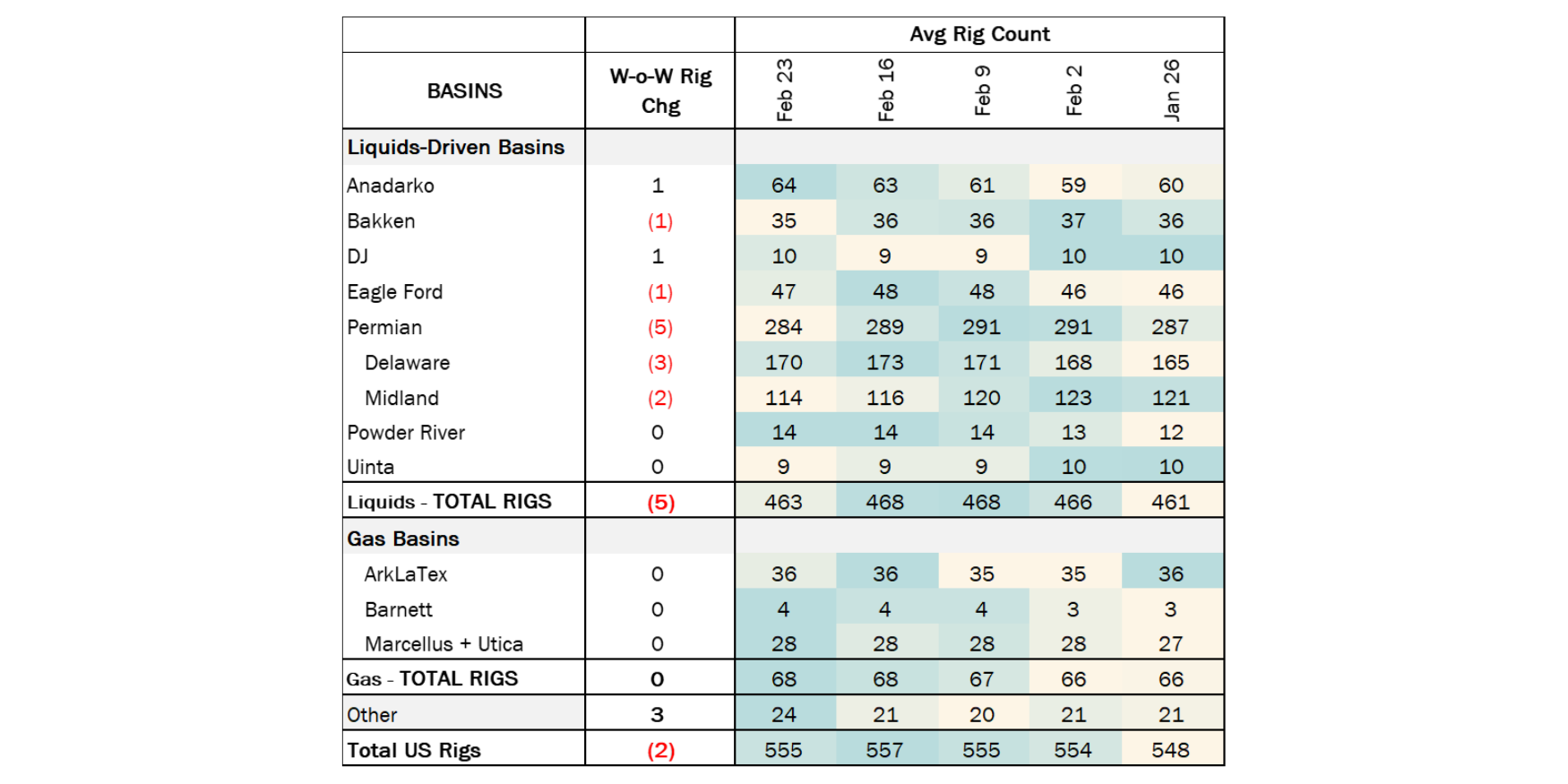

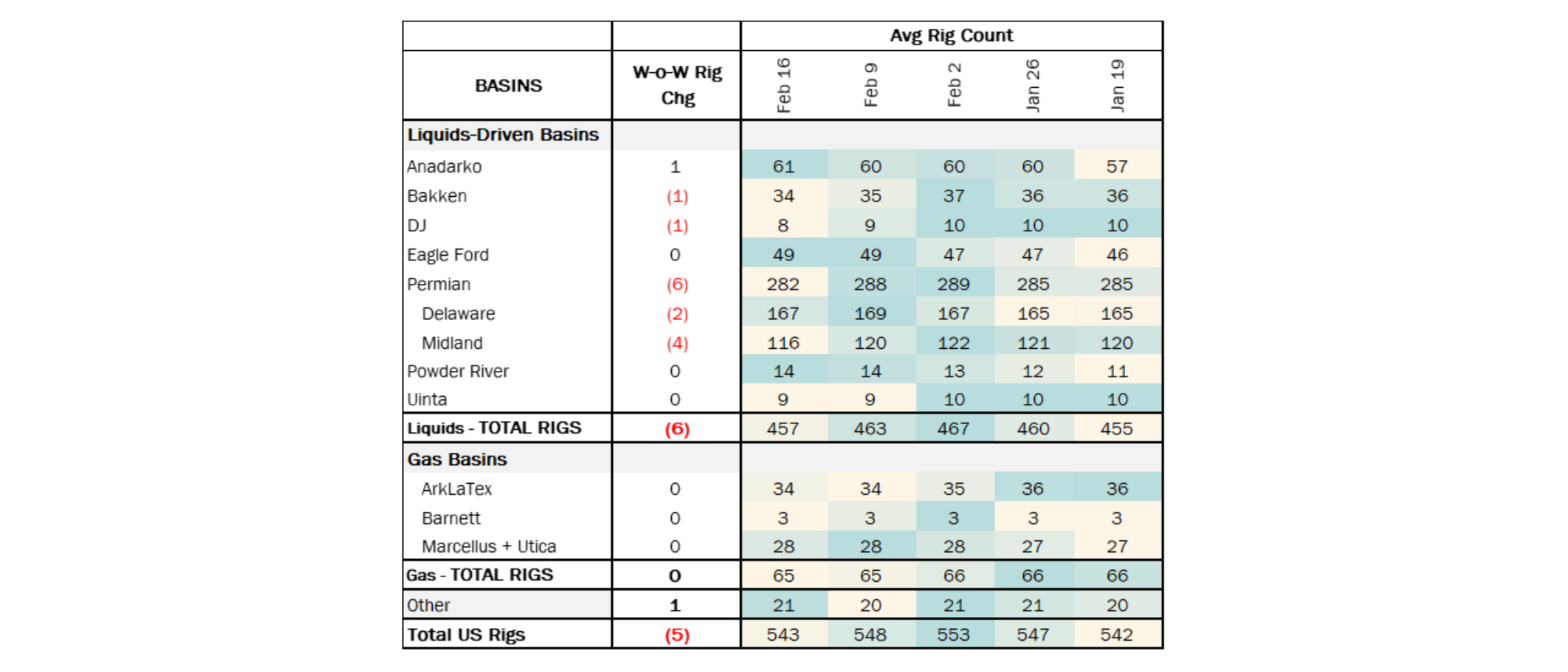

The US total rig count decreased by 2 for the July 28 week, down to 557 from 559. Liquids-driven basins saw a decrease of 3 rigs, moving the count from 454 to 451. The Anadarko Basin rig count decreased by 2, whereas the Permian and Unita basins each lost 1 rig.

In the Anadarko, operators Warwick Partners III and Wavetech Helium each removed 1 rig. In the Delaware Basin, Conoco Phillips and Continental Resources each laid down 1 rig, whereas Midland operator TRP Operating increased its rig count by 1. In the Uinta Basin, Morning Gun Exploration LLC dropped 1 rig.

Flows: The total interstate gas meter sample is down 1.5% W-o-W, driven by declines in the Haynesville and Marcellus.

The Northeast gas sample declined 3% W-o-W, with significant declines in NE and SW Pennsylvania (down 320 MMcf/d and 390 MMcf/d respectively), partially offset by an increase in West Virginia (up 360 MMcf/d). Systems in the region show varied performance; some run by Energy Transfer (ET), DT Midstream (DTM) and Equitrans (ETRN) were down significantly (with associated producers: CTRA, SWN and EQT) and others owned by Williams (WMB) and MPLX were up slightly (with associated producers: AM and EQT).

The Haynesville (ArkLaTex) region saw a 1.5% W-o-W decline in pipeline samples. In the Permian Basin, the Waha hub continues to be heavily discounted, with ongoing El Paso Natural Gas Pipeline maintenance expected to disrupt flows across multiple locations, impacting gas distribution in the region.

*W-o-W change is for the two most recent weeks.

Infrastructure:

NGL takeaway capacity is extremely tight right now from the Permian Basin, but that dynamic is about to change. Almost 1.2 MMb/d of pipeline capacity is set to come online in the next year out of the Permian. East Daley has seen this overbuild movie before, and we’re pretty sure how it will end.

East Daley Analytics is tracking five pipeline expansions in the NGL Hub Model that will loosen NGL pipeline egress from the Permian Basin, and starting soon. Targa Resources (TRGP) plans to begin service on the 400 Mb/d Daytona NGL Pipeline in 3Q or 4Q24. Other expansions ahead include:

- YE24: ONEOK’s (OKE) WestTX NGL expansion (190 Mb/d)

- 2Q25: Enterprise Product’s (EPD) Bahia Pipeline (600 Mb/d)

- 2Q25: MPLX and EPIC’s combined BANGL and EPIC expansions (150 Mb/d)

- 2026: Energy Transfer’s (ET) Lone Star expansion (~90 Mb/d)

These NGL pipeline expansions are shown in the table. Enterprise in 2Q25 plans to return Seminole Pipeline to crude service, reducing NGL takeaway from the Permian by 150 Mb/d. Otherwise, operators over the next 12 months will see significant new options open up to move their NGLs. We have seen this infrastructure overbuild movie before, and it’s usually legacy pipelines that end up offering free HBO to fill vacancy. In our NGL Hub Model, East Daley expects an average 2025 utilization rate just shy of 80% on pipelines exiting the Permian Basin (see figure).

Ownership of upstream NGL volumes will play a big role separating the winners and losers in this new dynamic. As shown in the table, Targa and MPLX can effectively fill their egress pipes with NGLs produced from their own G&P assets in the Midland and Delaware sub-basins, while Enterprise and ET control over half of the supply moving through their NGL pipelines.

The fight for NGL barrels has been a significant factor driving M&A activity recently in the Permian as the industry prepares for the shift ahead. We will look at the risks, and how companies can defend market share, in the weeks ahead. Check out East Daley’s NGLs webinar on August 28 to learn more.

Purity Product Spotlight:

Ethane production from processing plants has hit record highs for three months straight. As discussed in EDA’s Ethane Supply & Demand Report, tight gas egress out of the Permian coupled with maintenance on numerous gas pipelines like Gulf Coast Express (GCX), Permian Highway Pipeline (PHP) and El Paso Pipeline has stretched processing plant ethane recovery to the max. Early samples of state-reported plant ethane production (a leading indicator of EIA ethane data) suggests extraction actually declined from May to June. Plants that have reported a decline in ethane production include Enterprise Products’ (EPD) Orla and Mentone plants in the Delaware, as well as Kinetik’s (KNTK) Diamond plant. It’s too early to tell if this data represents a blip or a trend, but the next batch of data on September 1 should fill in some of the gaps.

Data Points & Product Release Calendar: