Exec Summary

Market Movers: With the Fayetteville shale in structural decline, the Fayetteville Express Pipeline has potential optionality for the right owner willing to bet on higher gas prices.

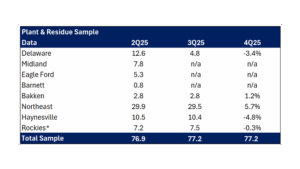

Estimated Quarterly Volumes: Northeast meter point samples are up 5.7% from 3Q25.

Calendar: Updated Financial Models available Dec. 12.

Market Movers:

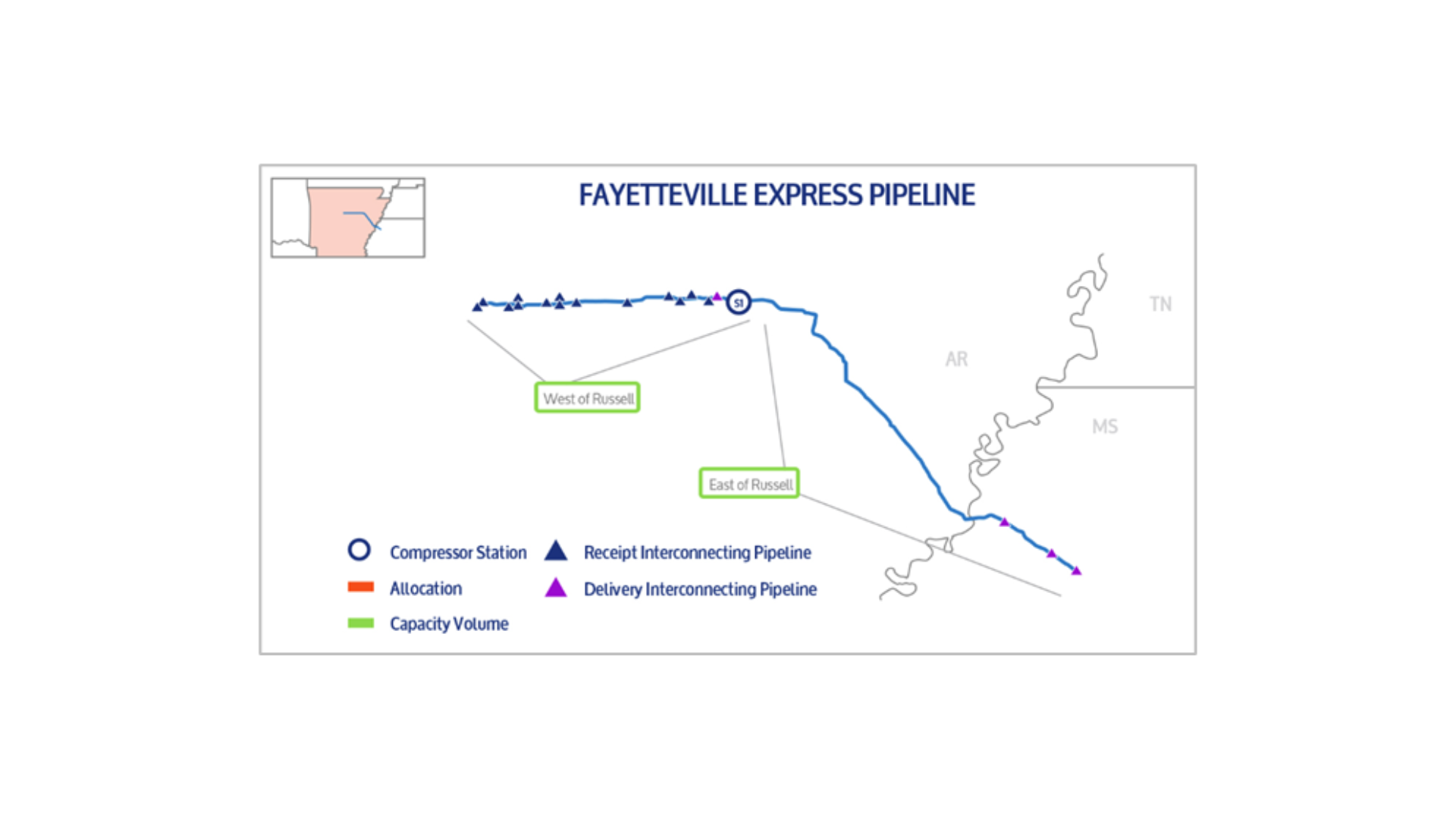

Energy Transfer (ET) and Kinder Morgan (KMI) each own 50% of the 2.0 Bcf/d Fayetteville Express Pipeline (FEP), a 185-mile, 42-inch line moving dry gas from the mature Fayetteville shale into ET’s Trunkline system in Mississippi. With the Fayetteville in structural decline, FEP has potential optionality for the right owner willing to bet on higher gas prices.

The former Southwestern Energy (now Coterra Energy (CTRA)) was the dominant Fayetteville operator before exiting the play in late 2018, selling its upstream and related midstream gathering business to private equity-backed Flywheel Energy for $1.865B.

For KMI, the asset is non-operated, generates modest earnings, and has a declining profile as contracts roll off. FEP has already flagged “adverse economic conditions” in regulatory filings, and postings show meaningful unsubscribed capacity, a weak fit with KMI’s rotation toward higher-growth pipes and storage.

For Energy Transfer, the same facts cut the other way. ET already operates FEP and wholly owns Trunkline Pipeline for downstream access. ET is also developing the 16.5 Mtpa Lake Charles LNG project, which will rely on Trunkline for feedgas. Owning 100% of FEP would simplify tariff and operating decisions along the corridor connecting the Fayetteville to Lake Charles, concentrating any upside from recontracting or repurposing the lateral.

Economically, the Fayetteville is a high-cost swing basin. The play is in harvest mode at a $3/MMBtu Henry Hub price, with legacy wells managed for cash and little justification for new drilling. If gas moves into a $4 range, the remaining core rock and refrac candidates start to work again, and sustained prices over $5 could support a modest rig program and targeted completions.

ET still has higher-return uses for capital in the Permian and to support its NGL value chain. But if KMI moves to prune non-core JVs, ET is the obvious consolidator and could turn a challenged Fayetteville pipe into a strategic bolt-on for its LNG ambitions.

Investor Takeaway: FEP screens as a logical non-core sale for KMI and a clean-up buy for ET, but any transaction must compete with ET’s other growth projects for capital.

The Permian Basin at a Crossroads: Download Why This Pipeline Boom is Different

The Permian’s next big buildout is already taking shape — but this time, the drivers aren’t producers chasing oil. East Daley’s latest white paper reveals how gas demand from AI data centers, LNG exports, and utilities is rewriting the midstream playbook. Over 9 Bcf/d of new capacity and $12 billion in investments are reshaping flows, turning the Permian into a gas powerhouse even as rigs decline. Read Part II: Why This Pipeline Boom is Different

Estimated Quarterly Volumes:

Notes: 4Q25 is expressed as Q-o-Q growth from 3Q25. Rockies is the sum of Big Horn, DJ, Green River, Piceance, Powder River, San Juan, Uinta and Wind River.

- Rockies meter point samples are down 0.3% from 3Q25. The EPD-Meeker system is down 1.2% from 3Q25 and the WMB–Willow Creek system is down 2.8% from 3Q25. Flywheel Energy is the largest producer behind the EPD-Meeker system, responsible for 81% of the volumes.

- The Bakken meter point samples are up 1.2% from 3Q25. The Palermo system is up 2.2% from 3Q25 and the KMI–Bakken system is down 15.8% from 3Q25. Continental Energy is the largest producer behind the KMI system, responsible for 28% of the volumes.

Calendar: