Exec Summary

Market Movers: Energy Transfer (ET) is looking to upsize its Desert Southwest pipeline after selling out the initial 1.5 Bcf/d of capacity in a recent open season.

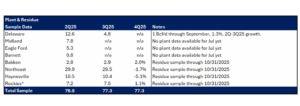

Estimated Quarterly Volumes: The Northeast meter point sample stepped down 2.6% from 3Q25.

Calendar: Updated Financial Models available Dec. 12.

Market Movers:

Energy Transfer (ET) is looking to upsize its Desert Southwest pipeline after selling out the initial 1.5 Bcf/d of capacity in a recent open season. The results confirm strong gas demand potential in the Southwest from utilities and data centers.

ET made waves this summer when it announced FID on Desert Southwest, a proposed expansion of its Transwestern Pipeline, before completing an open season. The project will add 516 miles of 42-inch pipe at an initial capacity of 1.5 Bcf/d, and with the potential for further expansion, ET said in the Aug. 6 announcement.

The decision to move forward without formal contracts showed confidence in Desert Southwest, a strategy validated by the results of the open season. The project sold all 1.5 Bcf/d of the initial capacity under 25-year contracts with investment-grade counterparties, ET revealed in its 3Q25 investor presentation. Moreover, since closing the initial open season, the project has “received significantly more interest than current planned capacity,” and the company is evaluating expansion options.

Desert Southwest has an expected 4Q29 in-service date, and ET confirmed the $5.3B Capex estimate. The company has entered into commitments with US pipe mills to lock in pipe delivery in 4Q27 at favorable prices, and anticipates 100% of the project’s pipe fabrication will be locked in soon.

Management is considering whether to upsize the project from 42- to 48-inch pipeline given the strong interest since the open season, executives said on the investor call. The move would potentially add 0.5-1.0 Bcf/d to delivery capacity.

The success of the proposed expansion comes as no surprise to East Daley Analytics. In the West Coast Supply & Demand Report, we had identified a growing imbalance in the Southwest from new utility and data center demand, before ET announced the Transwestern expansion. Gas consumption is increasing to support population growth and an emerging technology hub. Including the expected startup of ECA LNG on Mexico’s Pacific coast, we forecast a regional imbalance of over 1.6 Bcf/d by 2030. The Desert Southwest project will go a long way to fill this gap.

Data center development in Arizona has been strong as the AI boom continues, and gas continues to be the preferred fuel to generate power and reinforce that buildout. In the Data Center Demand Tracker, we are currently tracking nearly 20 data center projects in Maricopa County in Phoenix. If all those projects are powered by gas-fired generation, Maricopa could see nearly 1.2 Bcf/d of additional demand.

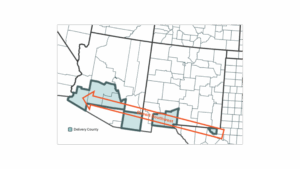

Desert Southwest is designed to deliver gas to seven counties across Texas, New Mexico and Arizona (see map), following existing pipeline easements for “between 75% to 99% of the route,” according to a project update on ET’s website. We expect Desert Southwest will largely follow the same route as El Paso Natural Gas’s South Mainline before interconnecting with Transwestern’s Phoenix lateral in Arizona.

In addition to building a new lateral, the expansion will also upgrade Transwestern’s existing Phoenix lateral. The project will modify an existing compressor and construct two new compressor stations to allow the lateral to move gas bidirectionally. The upgrades provide greater flexibility supplying gas into California further downstream.

The Permian Basin at a Crossroads: Download Why This Pipeline Boom is Different

The Permian’s next big buildout is already taking shape — but this time, the drivers aren’t producers chasing oil. East Daley’s latest white paper reveals how gas demand from AI data centers, LNG exports, and utilities is rewriting the midstream playbook. Over 9 Bcf/d of new capacity and $12 billion in investments are reshaping flows, turning the Permian into a gas powerhouse even as rigs decline. Read Part II: Why This Pipeline Boom is Different

Estimated Quarterly Volumes:

Notes: 4Q25 is expressed as Q-o-Q growth from 3Q25. Rockies is the sum of Big Horn, DJ, Green River, Piceance, Powder River, San Juan, Uinta and Wind River.

- The Haynesville meter point samples are down 5.1% from 3Q25. The DTM – Blue Union system is easing off its ramp from last quarter and is down 4.9% from 3Q25 and the Aethon – Kudo Midstream system is down 8.1% from 3Q25. Expand Energy is the largest producer behind the Blue Union system, responsible for 85% of the system’s volumes.

- Northeast meter point samples are down 1.7% from 3Q25. The ET – NEPA system is down 3.6% and the EQT – Eureka Midstream system is down 2.2% from 3Q25. Expand Energy is the largest producer behind the Blue Union system, responsible for 55% of the volumes.

Calendar: