Executive Summary:

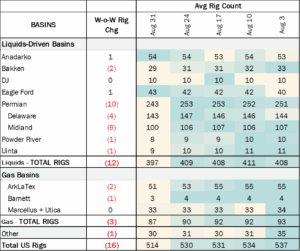

Rigs: The total US rig count decreased during the week of Aug 31 to 514.

Infrastructure: Plains to Sell US NGL Assets, Focus on Crude

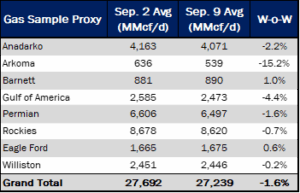

Supply & Demand: The US natural gas pipeline sample, a proxy for change in oil production, decreased 1.6% W-o-W across all liquids-focused basins.

Rigs:

The total US rig count decreased during the week of Aug 31 to 514. Liquids-driven basins decreased 12 rigs W-o-W from 409 to 397.

- Permian:

- Midland (-6): Vital Energy INC, Exxon, Diamondback Energy, Chevron Corporation

- Delaware (-4): Coterra Energy INC, Continental Resources

- Bakken (-2): Continental Resources, Chord Energy

- Powder River (-1): EOG Resources, INC

- Uinta (-1): Uinta Wax Operating, LLC

- Anadarko (+1): M & M Exploration CO

- Eagle Ford (+1): Redhawk Operating, LLC

Infrastructure:

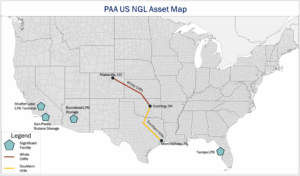

Plains All American (PAA) aims to become a crude oil midstream pure play, but a motley assortment of NGL assets stand in the way. After selling its Canadian NGL business, the company intends to shop its remaining US NGL portfolio.

In June, Plains reached a deal to sell its entire Canadian NGL business to Keyera for ~$3.75B. The sale will add $3B to PAA’s balance sheet and provide it with ample dry powder to pursue other bolt-on acquisitions. Following the announcement, PAA executives said they intend to sell the remaining US NGL assets over the next several years excluding select assets. PAA’s US NGL portfolio is relatively modest, yet also widely dispersed (see map). Those assets include the Shafter Lake LPG Terminal and San Pedro Butane Storage facility in California, Bumstead LPG Storage in Arizona, Tampa LPG in Florida, a 36% stake in White Cliffs LLC, and a scattering of other terminals and facilities across the Lower 48.

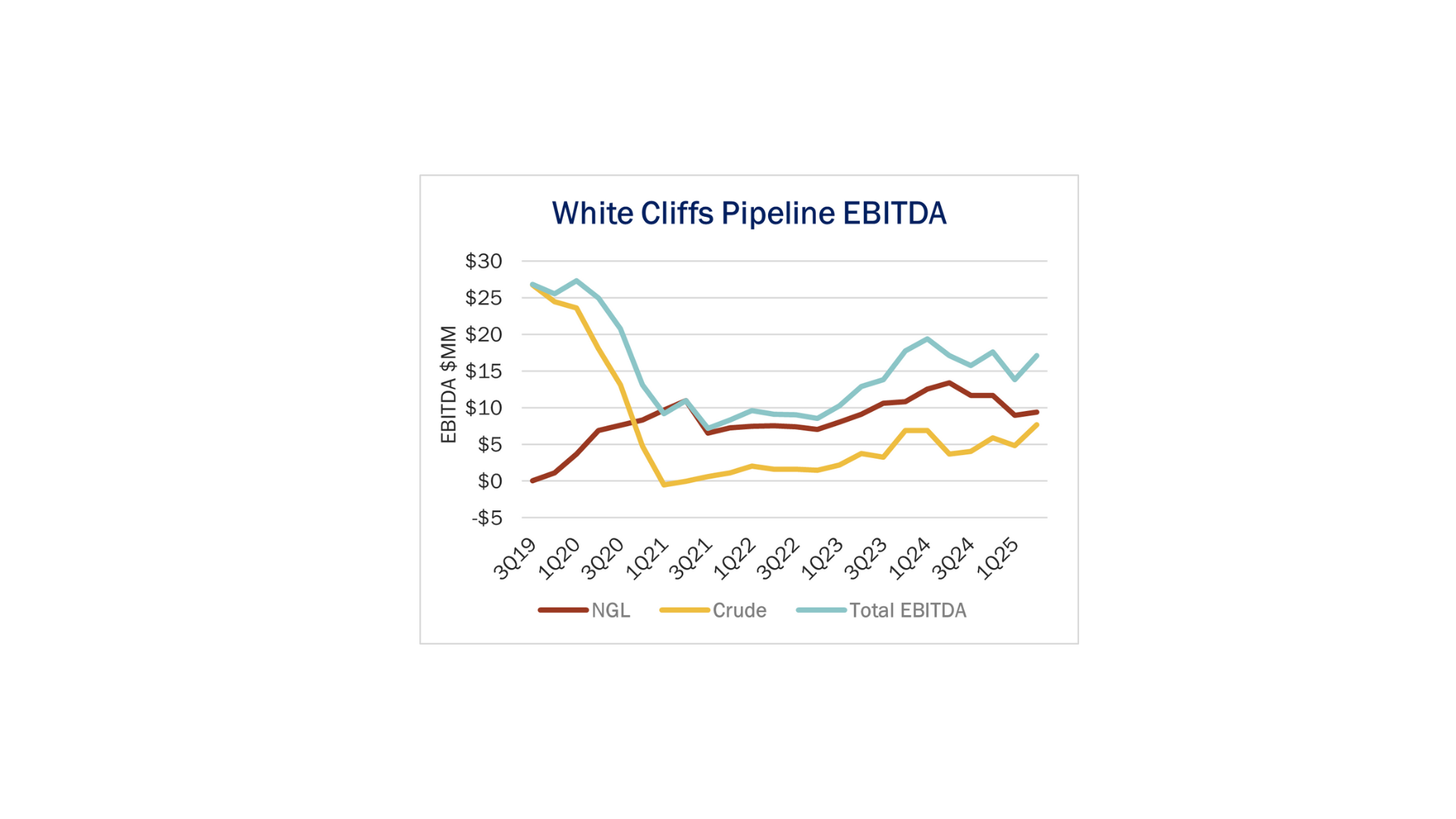

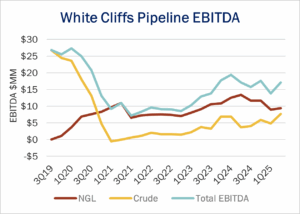

The White Cliffs Pipeline stake would likely be the most sought-after asset, though its ownership structure entangles its NGL and crude lines under one LLC, making its divestiture unlikely. This structure would make it a considerable challenge for PAA to divest its NGL line while retaining the crude line that integrates well with its footprint. Both lines run from Platteville, CO to Cushing, OK. The NGL pipeline serves as a key Y-grade outlet from the Denver Julesburg (DJ) and other Rockies basins, connecting to the Phillips 66 (PSX) owned Southern Hills Pipeline that provides connectivity to the Mont Belvieu Hub. White Cliffs has struggled post-pandemic to fill both its crude and NGL pipes. The NGL pipeline had an average modeled throughput of ~60 Mb/d in 2Q25, and the crude pipeline had average throughput of ~90 Mb/d, both below their respective capacities, according to East Daley’s Energy Data Studio.

Despite its struggles, White Cliff’s crude line remains relevant by steering volumes to PAA’s Cushing Terminal and running a route that is complementary to the Saddlehorn Pipeline (PAA 40% interest). The NGL line on the other hand is isolated from PAA’s scattered NGL footprint and appears more important to PSX’s NGL wellhead to water strategy. When White Cliffs converted one of its crude pipes to an NGL line in 2019 DCP Midstream (later acquired by PSX) reserved 50 Mbl/d of capacity until ~2030 allowing it to steer more NGL volumes onto its Southern Hills Pipeline. This effectively allows producers on its DJ G&P system to transport volumes directly to its Gulf Coast fractionators. This also pairs well with its existing interest in the Wattenberg and Front Range pipelines, both of which are substantial Y-grade egress routes out of the DJ.

While PAA’s stake in White Cliffs Pipeline is likely not for sale its motely assortment of terminals and storage facilities are. Despite their disparate geographies a buyer with an existing NGL footprint would be willing to pick them up for the right price. On PAA’s most recent earnings call executives estimated their US NGL portfolio’s value at between $100MM – $200MM. For PAA, monetizing their US NGL portfolio would free up cash that could be redeployed into other assets with higher synergistic potential. The company is clearly on the hunt, as reflected in PAA’s recent $1.57B investment in EPIC Crude.

Supply and Demand

The US natural gas pipeline sample, a proxy for change in oil production, decreased 1.6% W-o-W across all liquids-focused basins. Samples increased 1% in the Barnett and 0.6% in the Eagle Ford. The increases were offset by decreases of 15.2% in the Arkoma and 4.4% in the Gulf of America. The Rockies and the Gulf of America have a high correlation between gas volumes and crude oil volumes, whereas the Permian and Eagle Ford basins correlation is less than 45%.

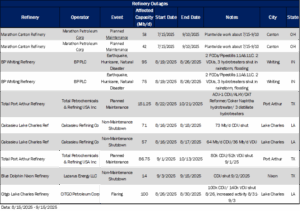

As of September 15th, there is currently ~252 Mb/d of refining capacity offline, including downtime for planned and unplanned maintenance. The Total Port Arthur Refinery accounts for 151.25 Mb/d capacity offline due to planned maintenance lasting till 10/21/2025.

Vessel traffic monitored by EDA along the Gulf Coast significantly increased W-o-W. There were 33 vessels loaded for the week ending September 13th and 21 the prior week.

Regulatory and Tariffs:

Presented by ARBO

Tariffs:

Gray Oak Pipeline, LLC: Certain available capacity discounts were increased.

Magellan Pipeline Company, L.P.: The tariffs were revised to add a new product and to update the product grade document to be consistent with ONEOK’s product grade documents.

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at [email protected] or phone at 202-505-5296. https://www.goarbo.com/