Executive Summary:

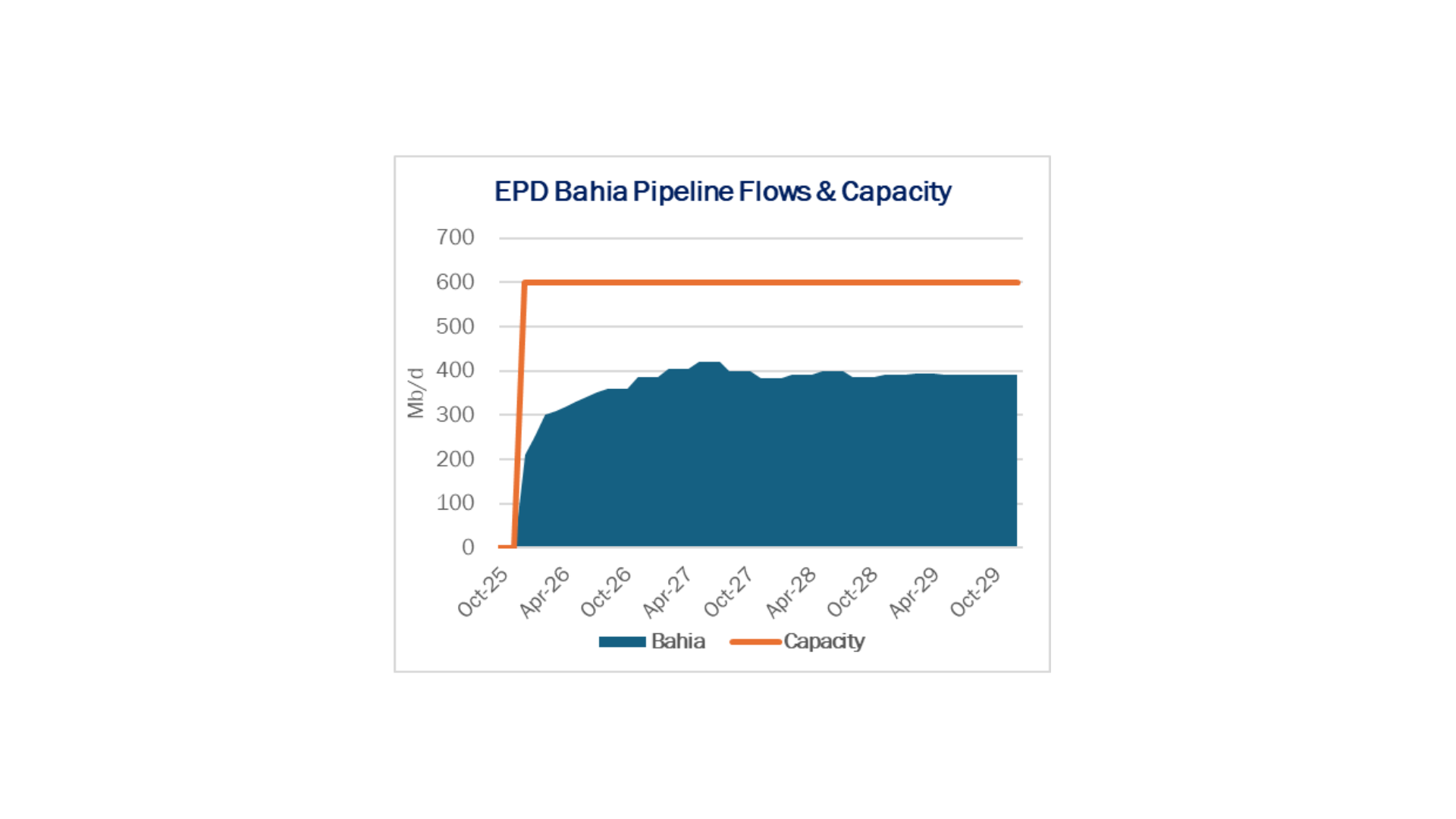

Infrastructure: Enterprise Products’ Bahia NGL pipeline is scheduled to enter service in December 2025, adding a major new artery from the Delaware and Midland basins to Mont Belvieu.

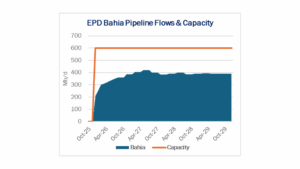

Exports: US NGL exports slipped 6.5% for the week ending Nov. 14, led by a sharp drop in LPG loadings at the Marcus Hook terminal.

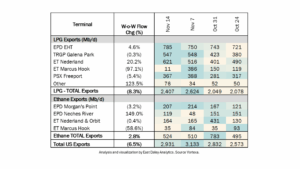

Rigs: The total US rig count decreased during the week of Nov. 2 to 514. Liquids-driven basins decreased 7 rigs W-o-W from 399 to 392.

Flows: US natural gas volumes in pipeline samples were flat for the week ending Nov. 16, averaging 69.2 Bcf/d.

Calendar: Nov. 24: NGL Production, Ethane S&D, Propane S&D

Infrastructure:

Enterprise Products’ (EPD) Bahia NGL pipeline is scheduled to enter service in December 2025, adding a major new artery from the Delaware and Midland basins to Mont Belvieu. The 550-mile system brings 600 Mb/d of Y-grade capacity, replacing legacy flows on Seminole Pipeline and increasing net Permian NGL takeaway by ~450 Mb/d.

East Daley expects a rapid ramp once Bahia is online. Seminole’s historical volumes provide a foundation for baseload throughput, and EPD will be highly motivated to rebalance flows across its network as Shin Oak approaches system limits.

With Seminole being converted back to crude service as the future Midland-to-Echo 2, EPD effectively trades a constrained NGL pipe for a high-value crude corridor while expanding Y-grade egress through Bahia. The shift underscores EPD’s long-term strategy: secure more barrels on its integrated value chain and protect its fractionation share at Mont Belvieu.

Strategically, Bahia adds to what is already shaping up as an overbuilt Permian NGL takeaway environment through 2026. But for EPD, the new line strengthens network optionality, protects Shin Oak reliability, and ensures the system can capture and move the next tranche of basin growth as new G&P plants come online.

The Permian Basin at a Crossroads: Download Why This Pipeline Boom is Different

The Permian’s next big buildout is already taking shape — but this time, the drivers aren’t producers chasing oil. East Daley’s latest white paper reveals how gas demand from AI data centers, LNG exports, and utilities is rewriting the midstream playbook. Over 9 Bcf/d of new capacity and $12 billion in investments are reshaping flows, turning the Permian into a gas powerhouse even as rigs decline. Read Part II: Why This Pipeline Boom is Different

Exports:

US NGL exports slipped 6.5% for the week ending Nov. 14. The headline movement came from a sharp collapse in LPG loadings at ET’s Marcus Hook — down nearly 100% — which was offset by a notable spike in ethane exports out of EPD’s Neches River terminal. Despite the contrasting shifts at individual docks, the combined effect leaves total US NGL exports showing only a modest decline.

Rigs:

The total US rig count decreased during the week of Nov. 2 to 514. Liquids-driven basins decreased 7 rigs W-o-W from 399 to 392.

- DJ (-1): BWAB Inc.

- Eagle Ford (-2): BP, Capital Star Oil & Gas

- Permian:

- Delaware (-3): Chevron, Permian Resources, Mewbourne Oil

- Midland (-2): ExxonMobil

Powder River (+1): Anschutz

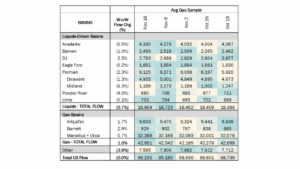

Flows:

US natural gas volumes in pipeline samples were flat for the week ending Nov. 16, averaging 69.2 Bcf/d.

Major gas basin samples gained 1.0% W-o-W to average 43.0 Bcf/d. The Haynesville sample increased 1.7% to 9.6 Bcf/d, while the Marcellus+Utica sample gained 0.7% to 32.4 Bcf/d.

Samples in liquids-focused basins decreased 0.7% to 18.6 Bcf/d. The Permian sample declined 2.3% to 6.1 Bcf/d, while the Denver-Julesburg sample gained 3.5% W-o-W.

Calendar: