Executive Summary: Rigs: The total rig count decreased by 12 for the September 1 week, down to 556 from 568. Flows: Constraints at the Waha hub persist as operators await the start-up of Matterhorn. Infrastructure: Though unloved now, East Daley believes the Bakken will play a larger role as a supplier of ethane than commodity markets give credit. Purity Product Spotlight: EDA anticipates significant propane supply growth once Matterhorn comes online.

Rigs: The total rig count decreased by 12 for the September 1 week, down to 556 from 568. Liquid-driven basin rigs decreased by 11 from 461 to 450. The Permian Basin dropped 5 rigs, for a total Y-o-Y rig decline totaling 40 rigs. The Anadarko and Powder River basins each declined by 2 rigs whereas the Eagle Ford and Uinta basins each dropped 1.

- Midland: Endeavor Energy dropped (2), APA Corp and Texland Petroleum (1) each

- Delaware: Devon Energy Corporation (1)

- Anadarko: 89 Energy III Inc and Calyx Energy III (1) each

- Eagle Ford: Crescent Energy Company (1)

- Powder River: True Companies and Hilcorp (1) each

- Uinta: Uinta Wax Operating (1)

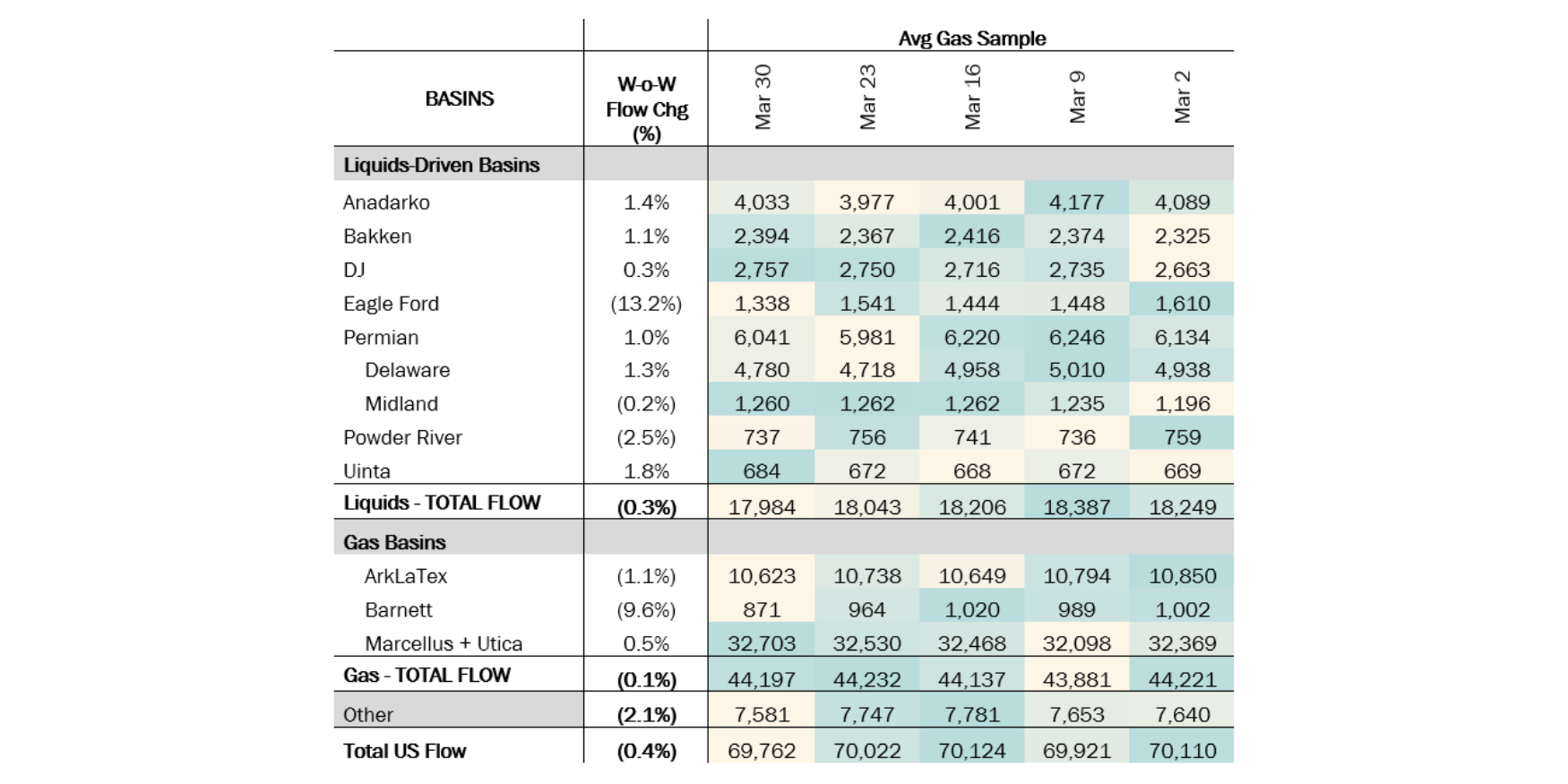

Flows: Constraints at the Waha hub persist as operators await the start-up of Matterhorn. On its 2Q24 earnings call, EnLink Midstream (ENLC) executives said they “expect the pipeline to be in service in the month of September. That's maybe a 2-week difference to what the original plan was toward the very end of August, but a very minor delay in the grand scheme of things, some of that weather related with Hurricane Beryl”. This week, the Permian Basin saw a slight increase in flows due to the completion of scheduled maintenance at various points on the El Paso pipeline.

*W-o-W change is for the two most recent weeks.

Meanwhile, flows in the ArkLaTex region decreased 2% W-o-W as production may have been impacted by Hurricane Francine. East Daley estimated an average of 1.25 Bcf/d has been curtailed this year in the basin. We also see the impact of the hurricane on offshore oil and gas production in the Gulf of Mexico (GOM) during the week of October 9. The shutdown of multiple platforms, including large producers like Shell and Chevron, temporarily reduced production. The GOM pipeline sample dropped 42% from 2.4 Bcf/d on the first week of September to 1.3 Bcf/d on the week of the storm. Partial impacts can still be seen from the latest pipeline sample for September 18 of 1.9 Bcf/d, or 0.5 Bcf/d below the average for the first week of September.

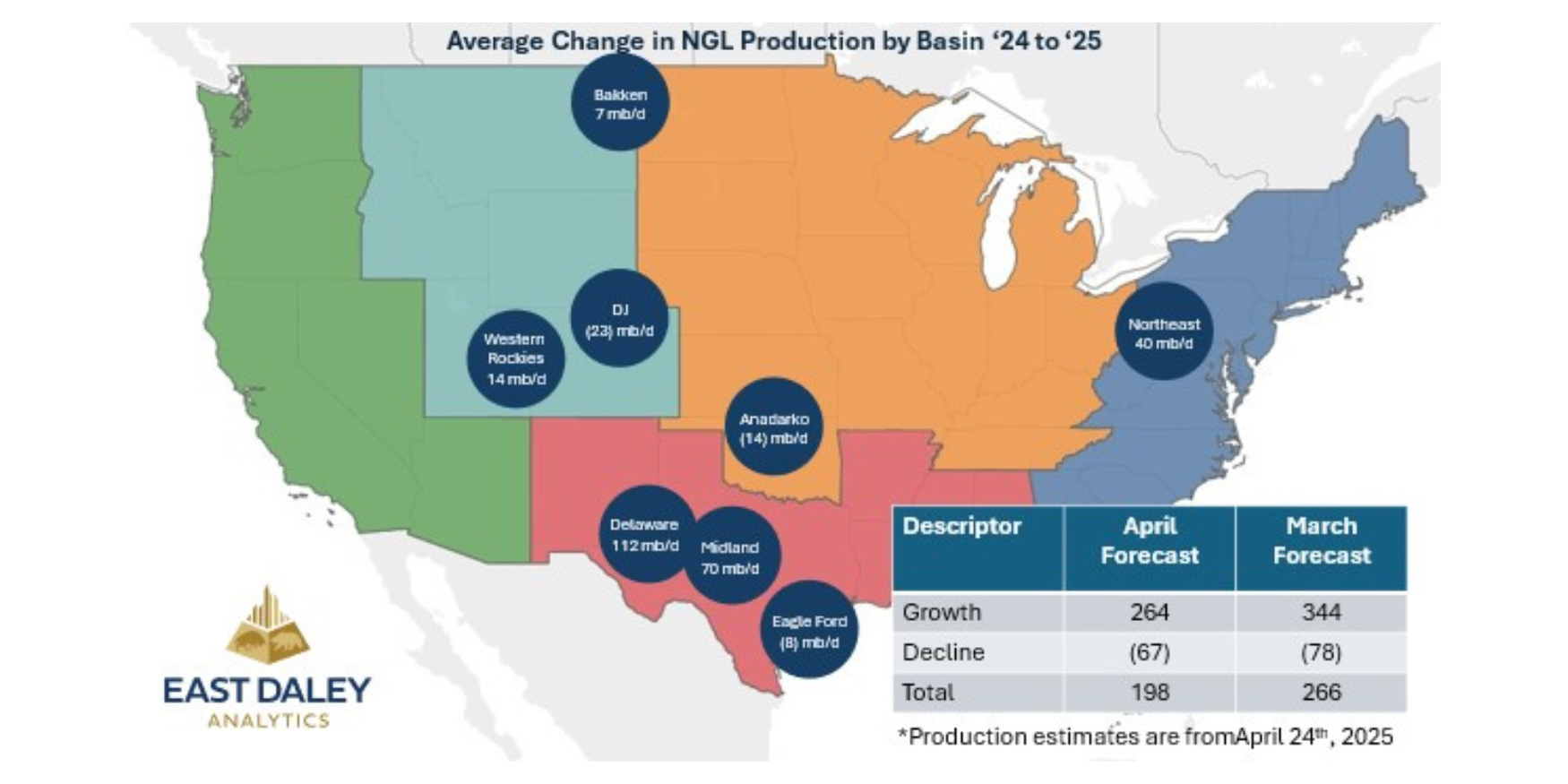

Infrastructure: Though unloved now, East Daley believes the Bakken will play a larger role as a supplier of ethane than commodity markets give credit. If correct, we anticipate more ethane will be shipped to the Gulf Coast, and more EBTIDA generation for ONEOK (OKE).

Location is the biggest hurdle for the Bakken. North Dakota is far from Mont Belvieu, the fastest growing demand market, setting a high cost to move trapped ethane to Texas. The Bakken is much farther away from market than the Permian, Eagle Ford or Anadarko, so the in-basin price netback is not as competitive.

The spot price of ethane at Mont Belvieu is about $0.16/gal today, but the contango-shaped curve indicates prices around $0.25/gal in 2026. From the Bakken, shippers (mostly producers) pay a bundled transportation and fractionation (T&F) rate of ~$0.30/gal to move molecules to Mont Belvieu.

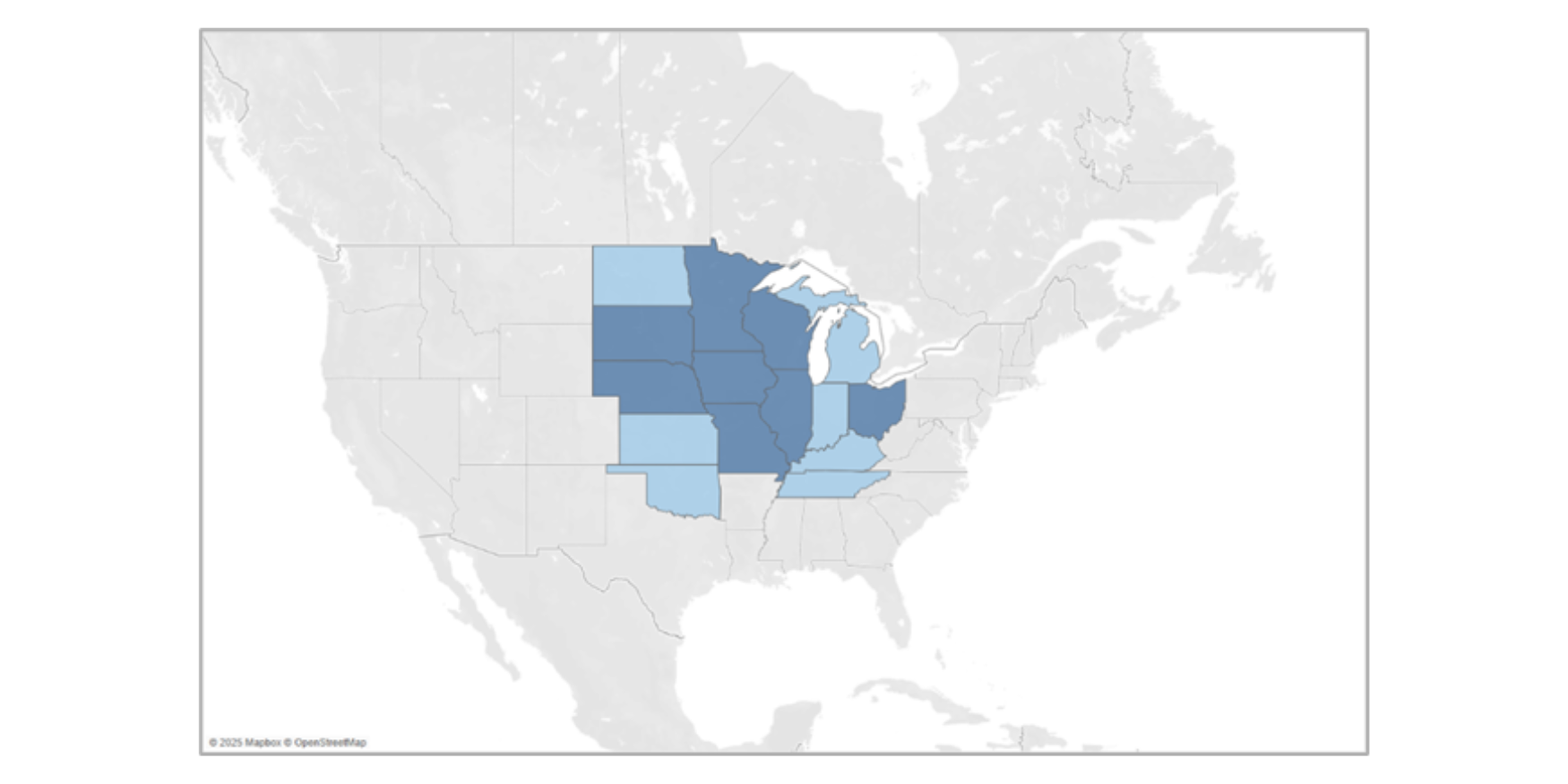

As shown in the map, ethane does not move at these prices. Instead, it is sold as a gas molecule down Northern Border Pipeline, where the price on a $/gal equivalent is higher. This is why our Bakken NGL forecast looks flat (see figure) and mirrors EDA’s outlook on overall oil and gas production growth in the Bakken. Northern Border does have limits to the amount of ethane that can be delivered before the composite Btu content becomes too high.

Here’s the key thing to ethane – the market does not require more drilling or completion capital to yield more supply. The marginal cost to cool down cryogenic plants (especially in the Bakken winter season) to extract the lightest end of the NGL barrel is minimal.

Instead, the invisible hand of the market must act as a catalyst to flip the switch on processing plants. That catalyst could come from ONEOK, where the internal economics may tell a different story than what market prices suggest.

Referring again to the map, the only cost OKE incurs to move its own ethane supply (“equity barrels”) to market is the variable T&F cost. EDA estimates this is $0.07-$0.09/gal from the Bakken to Mont Belvieu. When viewed in this context, the c2 netback price becomes 1) positive at $0.16-0.18/gal and 2) greater than the equivalent per-gallon price if sold as gas at AECO prices in 2026.

EDA recently gave our view why OKE is opting to rebuild the Medford fractionator in Oklahoma. We believe most of the NGL supply growth that supports the Medford frac will come from the Bakken (less so the Permian or Anadarko), as discussed in greater detail in EDA’s 3Q24 follow-up webinar to clients.

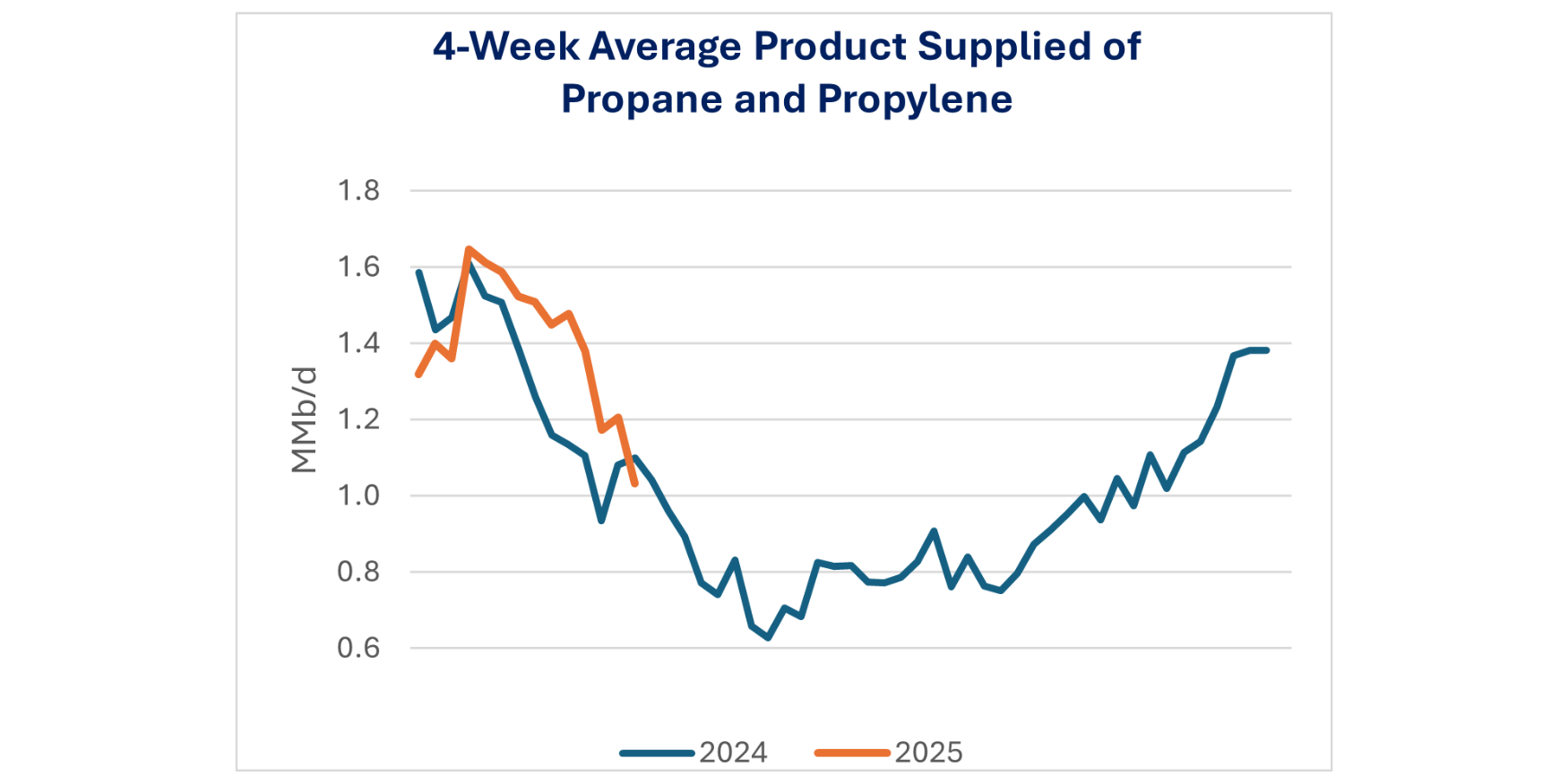

Purity Product Spotlight: EDA anticipates significant propane supply growth once Matterhorn comes online. Major producers like Chevron, ExxonMobil, Matador Resources, and Vital have all projected production growth into 4Q24.

On the demand side, domestic propane consumption has decreased Y-o-Y, largely due to lower seasonally adjusted demand. This trend was particularly evident in March 2024, when demand was significantly lower compared to the same period in 2023. On the export front, the US has seen a rise in propane and propylene exports, up 9% from August 2023 to August 2024. The first week of September 2024 saw exports hit 1,833 Mb/d, a 6% increase over the average weekly exports from September 2023.

Propane storage levels are expected to peak at around 100 MMbbl in September 2024. While the market appears reasonably priced, there is moderate downside risk heading into winter as Permian NGLs, including propane and butane, are expected to flood the Gulf Coast, potentially pushing LPG docks to their limits. Total LPG exports are primarily driven by propane and normal butane from the Gulf Coast and to a lesser degree, the Northeast. The risk of capacity constraints on the docks will be relieved by upcoming project on the Gulf Coast area that will add an average of 830 Mb/d of capacity. A detailed list of projects and dock utilization is availbale in our monthly Propane Supply and Demand report.

-1.png)