Executive Summary:

Infrastructure: Targa’s Speedway pipeline will extend its advantage in the race for Permian NGLs.

Exports: Total US NGL exports increased 6% for the week ending Oct. 5, driven by higher volumes from ET’s Nederland terminal.

Rigs: The US lost 2 rigs for the week of Sept. 27, bringing the total rig count to 529.

Flows: US natural gas volumes averaged 69.5 Bcf/d in pipeline samples for the week ending Oct. 5, down 0.6% W-o-W.

Infrastructure:

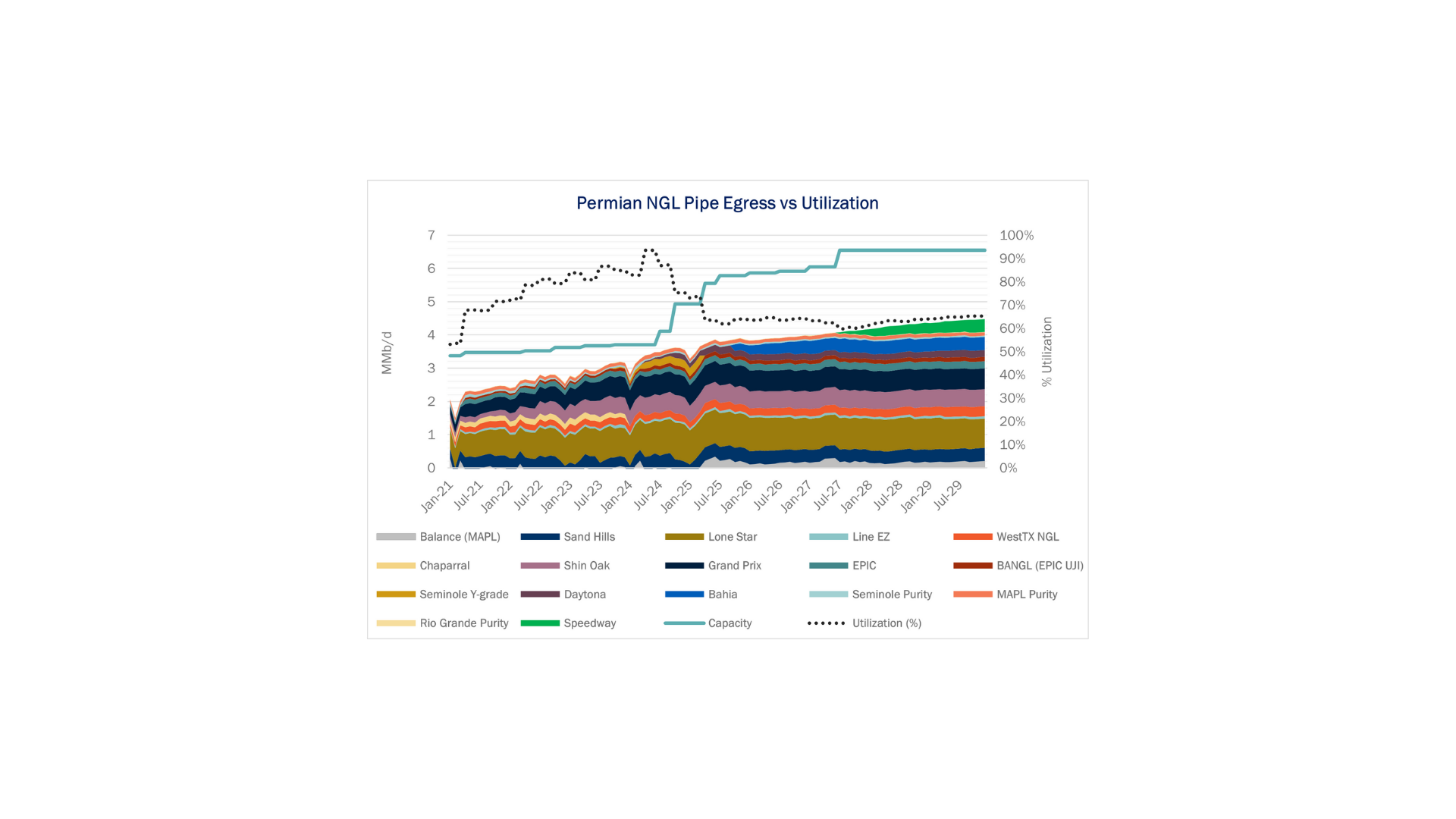

Targa Resources (TRGP) last week announced the Speedway NGL Pipeline, a new Permian-to-Mont Belvieu system, alongside the Yeti gas plant and Buffalo Run Midland-Delaware residue interconnect. The new pipeline is likely to exacerbate an industry fight for NGL barrels and result in significant spare capacity out of the Permian.

Management framed the new projects as the next steps in its “wellhead-to-water” strategy as TRGP’s existing NGL transport to Mont Belvieu approaches nameplate limits. The 30-inch Speedway will span roughly 500 miles and have initial capacity of ~500 Mb/d, expandable to ~1.0 MMb/d. Targa is targeting in-service in 3Q27 at an estimated cost of $1.6B.

Targa points to ~961 Mb/d of NGLs already moving into Mont Belvieu in 2Q25, essentially at system nameplate, and highlights 1.4 Bcf/d of new Permian processing under construction that could add ~200 Mb/d of incremental NGL supply by Speedway’s startup. To handle these volumes, the company is also advancing downstream fractionation expansions, including Trains 11 (150 Mb/d, 2Q26) and 12 (150 Mb/d, 1Q27) in Mont Belvieu, as well as LPG export debottlenecks through 3Q27.

The Speedway build recalls the trajectory of Grand Prix, which ramped to ~1 MMb/d at Mont Belvieu in six years after its 3Q19 startup. For Speedway, Targa projects baseload throughput of 210–240 Mb/d from its announced Permian plants, meaning the line could run half full at the start of operations. If Targa sustains the ~140 Mb/d annual NGL growth it achieved during the Grand Prix buildout, Speedway’s initial 500 Mb/d could be filled within about two years post-startup, around 2029. With Grand Prix essentially maxed out today, Speedway provides much-needed headroom, though TRGP must carefully sync fractionation and LPG export expansions to avoid system bottlenecks.

The gains for Targa are likely to come at the expense of others in the NGL space. From a market perspective, Speedway adds to an already overbuilt Permian NGL pipe grid. East Daley’s NGL Hub Model shows ~2.27 MMb/d of spare capacity today out of the Permian Basin — equivalent to 4.5 Speedways. When Speedway enters service, basin-wide utilization will dip to ~60% and remain under 70% for the rest of the decade.

In this context, the rationale for another NGL pipe is less about fee maximization and more about volume capture. Targa is uniquely positioned among peers: according to East Daley’s Permian Energy Path, TRGP produces ~200 Mb/d more NGLs than its nearest competitor. Speedway ensures these incremental NGL barrels stay captive on Targa assets from the wellhead to the dock.

This strategy will further tighten the squeeze on competitors like Phillips 66 (PSX), ONEOK (OKE) and MPLX, who are struggling for NGL barrels relative to pipe space. By locking in its own growth volumes, TRGP reinforces its integrated model and furthers its leading position in the Permian NGL value chain.

The main uncertainty in our outlook is the pace of supply growth. Developers have reached FID on several major Permian gas pipelines recently, including Desert Southwest by Energy Transfer (ET) and Eiger Express by the Matterhorn JV. East Daley anticipates significant spare egress capacity for Permian natural gas once these are built. However, if producers target more gas-focused acreage to fill them, NGL production will also increase. Faster supply growth would lift all boats and ameliorate the competitive pressures we anticipate for the industry to secure NGL barrels.

Bottom line: Speedway is less about market balance and more about control. Targa is building for itself, not the market, and in doing so extends its advantage in the Permian from processing plants through fractionation and export.

Exports:

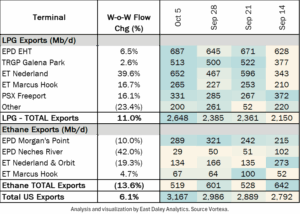

Total US NGL exports increased 6% W-o-W for the week ending Oct. 5, driven by higher volumes across LPG docks. Energy Transfer’s Nederland terminal led the way, up 40% W-o-W. In contrast, ethane exports declined at all docks except ET’s Marcus Hook, which posted a modest 5% gain.

Rigs:

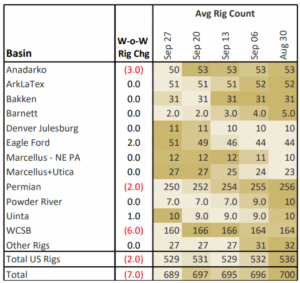

The US lost 2 rigs for the week of Sept. 27, bringing the total rig count to 529. The Anadarko (-3) and Permian (-2) lost rigs while the Eagle Ford (+2) and Uinta (+1) gained rigs W-o-W.

At the company level, PSX (-4), Iron Horse Midstream (-2), ET (-1), MPLX (-1), WES (-1), OKE (-1), XTO Energy (-1), Hess (-1) and Vaquero (-1) lost rigs while ENLC (+5), TRGP (+1), KMI (+1), Salt Creek Midstream (+1), and San Mateo Midstream (+1) gained rigs W-o-W.

See East Daley Analytics’ weekly Rig Activity Tracker for more information on rigs by basin and company.

Flows:

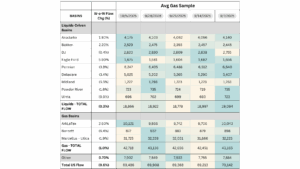

US natural gas volumes averaged 69.5 Bcf/d in pipeline samples for the week ending Oct. 5, down 0.6% W-o-W.

Major gas basin samples decreased 1.0% W-o-W to 42.7 Bcf/d. The Haynesville sample increased 2.6% to 10.1 Bcf/d, while the Marcellus+Utica sample declined 1.9% to 31.7 Bcf/d.

Samples in liquids-focused basins declined 0.3% W-o-W to 18.9 Bcf/d. The Permian sample fell 3.8% to 6.2 Bcf/d, while the Eagle Ford sample rose 5.9%.

Calendar: