Executive Summary: Rigs: The US total rig count decreased by 9 for the August 4 week, down to 559 from 568. Flows: The total interstate gas meter sample is down 0.8% W-o-W, driven by declines in the Anadarko, ArkLaTex and Marcellus. Infrastructure: New gas investments support NGL growth from the Permian Basin. Purity Product: Propane and propylene exports top 2 MMb/d for fifth time in 2024.

Rigs:

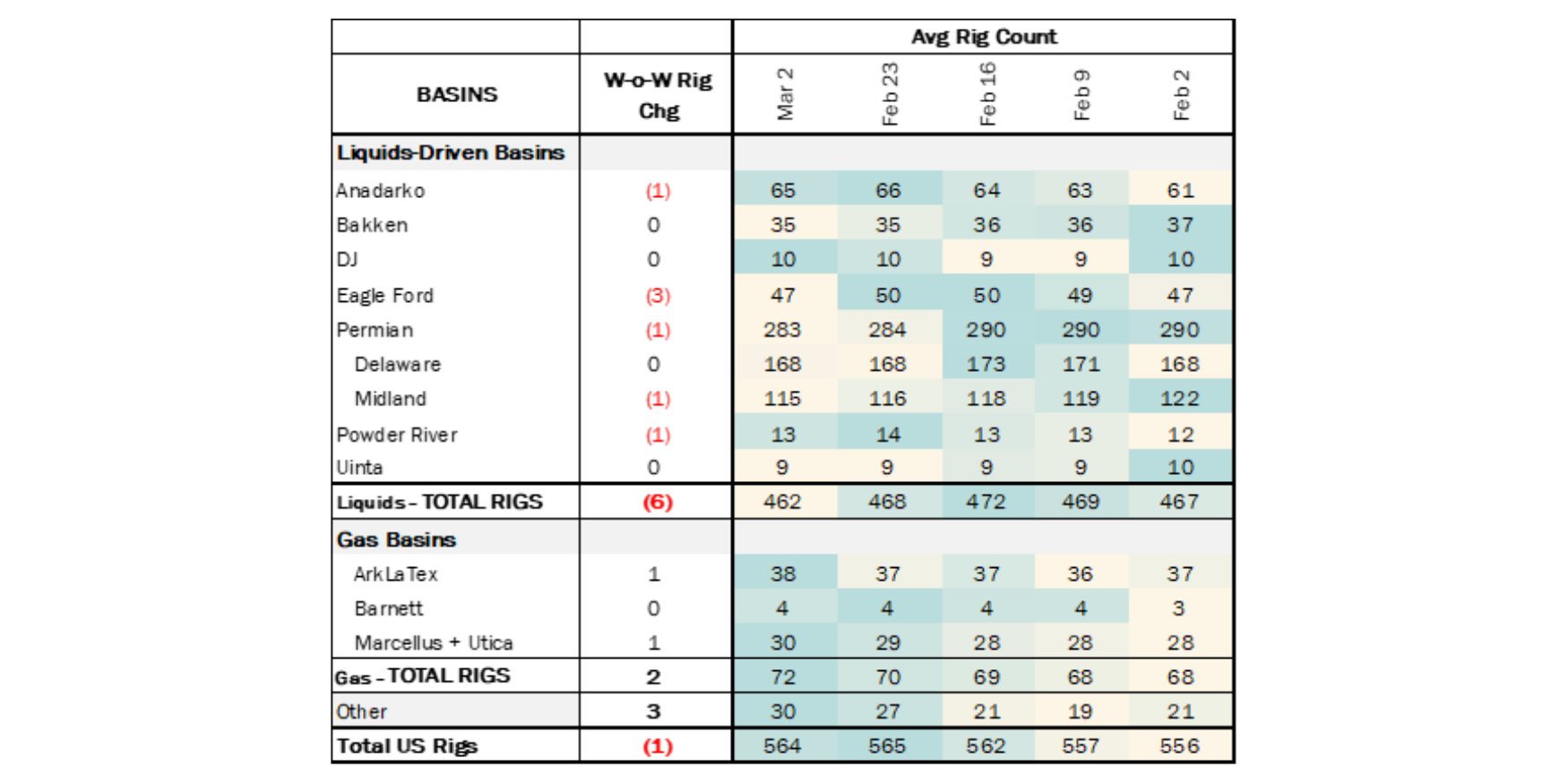

The US rig count decreased by 9 for the August 4 week, down to 559 from 568. Liquids-driven basins saw a decrease of 6 rigs, moving the count from 464 to 458. The Anadarko and Eagle Ford basins each decreased by 1 rig, whereas producers in the Bakken removed 2 rigs, and the Permian basin rig count declined by 3. The Powder River Basin gained 1 rig.

In the Anadarko Basin, operator Mack Energy removed 1 rig. In the Bakken, operators Chord Energy and Kraken Resources each released 1 rig. In the Eagle Ford play in South Texas, Crescent Energy dropped 1 rig. In the Delaware Basin, Spur Energy Partners dropped 1 rig, and Exxon (XOM) decreased its rig count by 2 in the Midland Basin.

Flows:

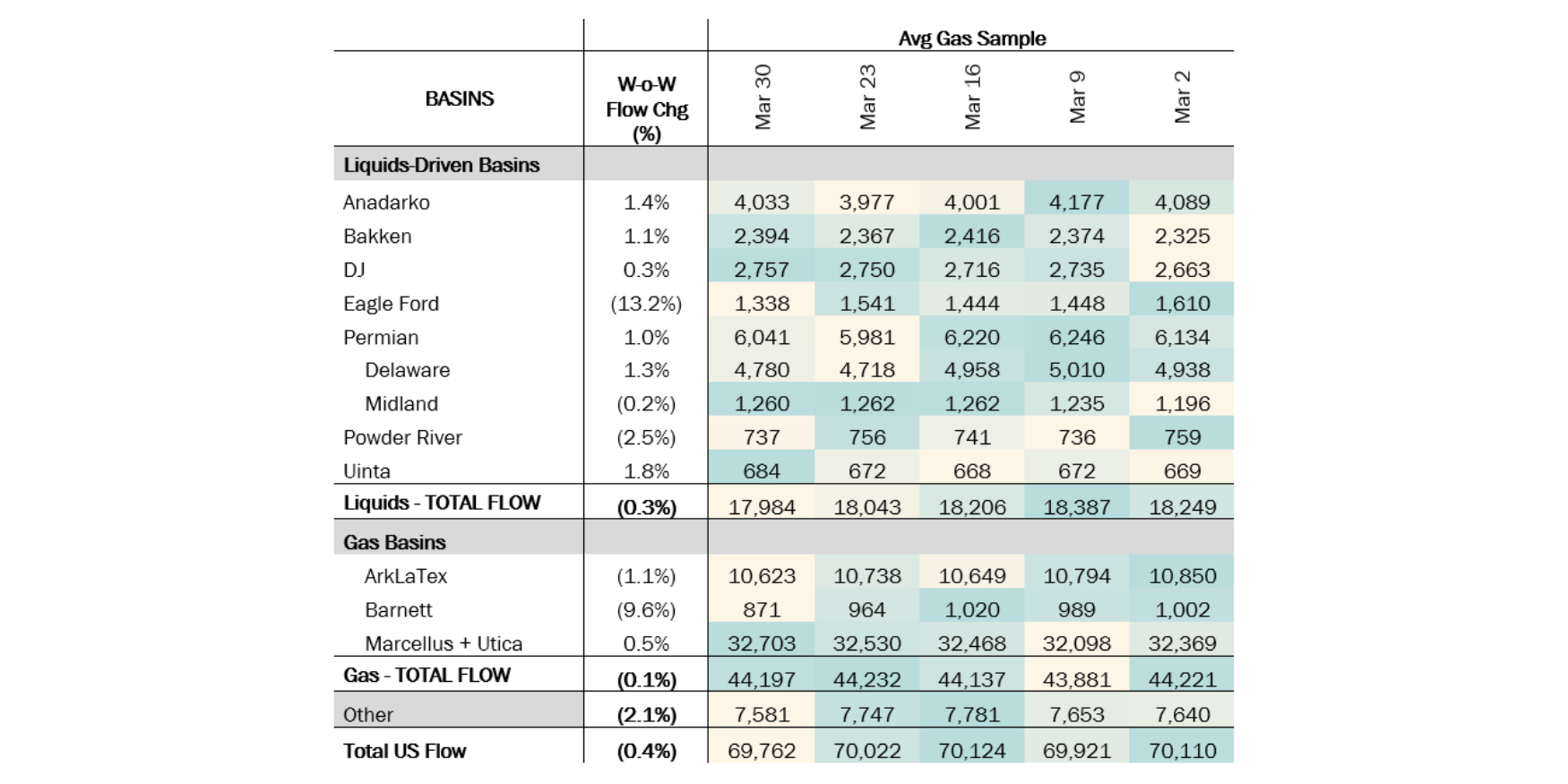

Anadarko Basin pipeline samples dropped 3% W-o-W, likely due to rerouting for scheduled maintenance on the NGPL system. The work on NGPL will reduce available pipeline capacity by 34% in the coming days. Additionally, a force majeure event at NGPL’s Liberty County, TX compressor station will further limit eastbound capacity until further notice.

In the Permian Basin, Waha hub prices continue to face discounts. The pipeline sample dropped by 2% W-o-W, possibly due to ongoing maintenance at nine KMI El Paso pipeline locations. Conversely, Midland samples increased by 3%, likely due to rerouted volumes to El Paso and NNG pipelines as NGPL’s TexOk Zone remains constrained.

The ArkLaTex sample saw a 1% W-o-W decline. In the Powder River Basin, samples fell 2% due to decreased volumes on MIGC and Tallgrass Interstate Gas Transmission pipelines, possibly due to a slight reduction in active rigs over the past three weeks. Colorado Interstate Gas Pipeline is preparing for further capacity reductions due to scheduled maintenance on the Cheyenne segment from August 20-22, and on the Greasewood compressor from August 27-28, reducing capacity by 251 MMcf/d and 120 MMcf/d, respectively.

The ArkLaTex sample saw a 1% W-o-W decline. In the Powder River Basin, samples fell 2% due to decreased volumes on MIGC and Tallgrass Interstate Gas Transmission pipelines, possibly due to a slight reduction in active rigs over the past three weeks. Colorado Interstate Gas is preparing for further capacity reductions due to scheduled maintenance on the Cheyenne segment from August 20-22, and at the Greasewood compressor from August 27-28, reducing capacity by 251 MMcf/d and 120 MMcf/d, respectively.

*W-o-W change is for the two most recent weeks.

Infrastructure:

East Daley sees Permian Basin gas production growing by 1.7 Bcf/d in 2024 as egress constraints are relieved by new pipelines over the next two years. The Matterhorn pipeline is expected to come online in September and add 2.5 Bcf/d of egress capacity. WhiteWater Midstream confirmed it expects an additional pipeline (Blackcomb) to come online in 2H26 and add another 2.5 Bcf/d of capacity to the Waha to South Texas route.

Permian production growth is supported by producer guidance and new plant expansions announced from companies like Energy Transfer (ET), Enterprise (EPD), Western Midstream (WES), EOG and Targa (TRGP), among others. From 2024–26 the Permian will see processing capacity increase by around 3.7 Bcf/d (2.4 Bcf/d in the Delaware and 1.3 Bcf/d in the Midland). Based on our current production forecast, we expect processing utilization will be 82% for 2024 and will increase to 88% by 2026.

This new infrastructure will contribute to NGL supply growth and help fill the expected 1.2 MMb/d of pipeline expansions over the next two years. East Daley Analytics is tracking five pipeline expansions in the NGL Hub Model that will loosen NGL pipeline egress from the Permian Basin, and starting soon. Targa Resources (TRGP) plans to begin service on the 400 Mb/d Daytona NGL Pipeline in 3Q or 4Q24. Other expansions ahead include:

- YE24: ONEOK’s (OKE) WestTX NGL expansion (190 Mb/d)

- 2Q25: Enterprise Product’s (EPD) Bahia Pipeline (600 Mb/d)

- 2Q25: MPLX and EPIC’s combined BANGL and EPIC expansions (150 Mb/d)

- 2026: Energy Transfer’s (ET) Lone Star expansion (~90 Mb/d)

Purity Product Spotlight:

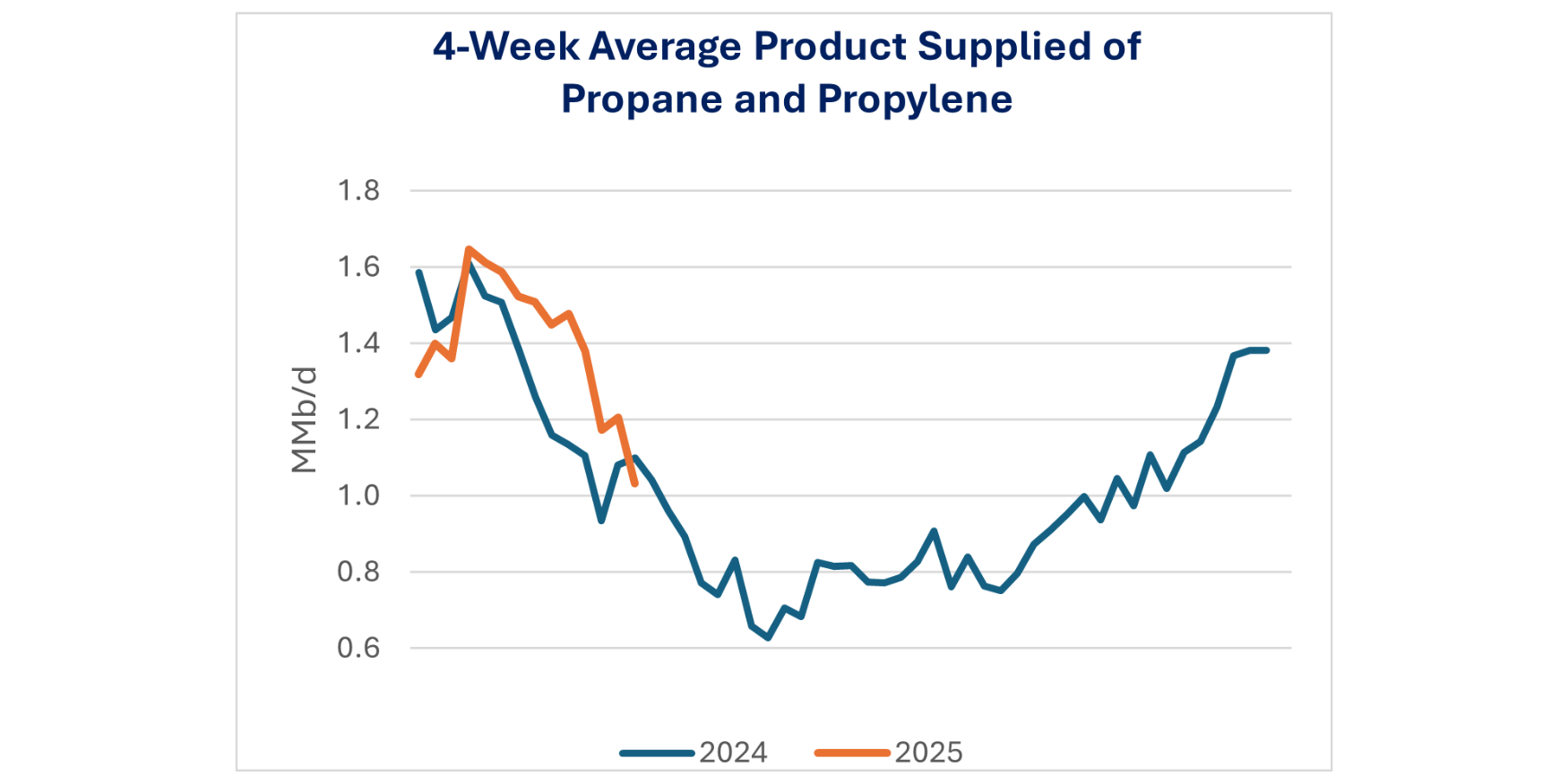

Weekly US exports of propane and propylene eclipsed 2 MMb/d for the fifth time this year, and the weekly storage number indicated a 2 MMbbl build to 92.1 MMbbl. Export demand has remained strong because of high Chinese demand to run propane dehydration (PDH) units. BW LPG reported earnings this morning and noted China’s LPG imports reached an all-time high in June. Interestingly, the run-rate has declined post-June. Some of that decline could be attributed to low LPG exports from the US in July (Hurricane Beryl) combined with PDH maintenance in China. In August, LPG exports are trending up 10% M-o-M and 11% Y-o-Y.

Data Points & Product Release Calendar:

-1.png)

-1.png)

-3.png)