Executive Summary: Infrastructure: MPLX is acquiring full ownership of BANGL for $715MM, expanding its reach from the Permian to export docks. Rigs: The US rig count decreased by 5 during the week of February 16 to 543. Flows: Total US pipeline volumes have increased from February's levels last week. Natural gas pipeline samples increased 3.4% W-o-W for the March 2 week, rising from 67.8 Bcf/d to 70.1 Bcf/d. Calendar: NVGS Earnings March 13th.

Meet East Daley at the OPIS NGL Summit

East Daley is attending the OPIS NGL Summit March 10-11th! We’ll present our perspective on NGL markets at the conference in Charlotte Harbor, FL and look forward to meeting other attendees. Reach out to schedule a meeting at the OPIS NGL Summit.

Infrastructure:

MPLX will acquire the remaining 55% interest in BANGL Pipeline for $715MM from affiliates of WhiteWater and Diamondback Energy. The deal for BANGL expands MPLX’s footprint in the Permian Basin and extends its reach to NGL export docks.

The Deal: MPLX will take full control of the BANGL system from the Permian to fractionation markets on the Gulf Coast. BANGL can transport up to 250 Mb/d of NGLs currently, and a planned expansion will increase capacity to 300 Mb/d by 2H26.

The companies expect to close the deal in July 2025, according to the February 28 announcement. MPLX said it expects mid-teen returns from the acquisition.

What We Like: Securing full ownership of BANGL aligns with MPLX's strategy to control the entire NGL value chain from wellhead to water.

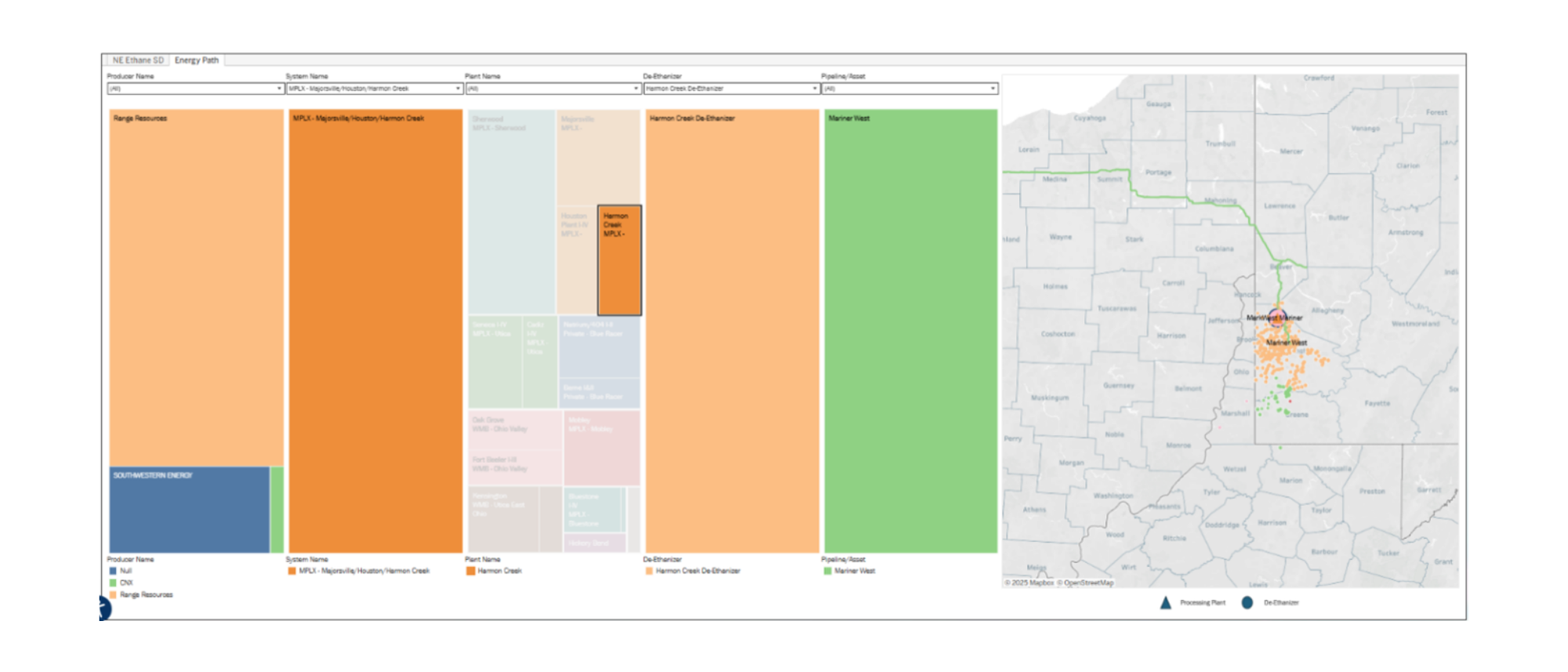

The map from East Daley’s NGL Hub Model shows NGL pipelines to the Texas Gulf Coast. EDA estimates that MPLX currently produces ~150 Mb/d of NGLs from its processing plants in the Permian, and sends those volumes to the Robstown and Sweeny fracs on the Texas coast. By 2029, we model MPLX will produce 210 Mb/d of NGLs from its Permian assets, and will be able redirect those liquids to its new fracs under development in Texas City. MPLX can also use BANGL to secure barrels for the new export facility it is developing under a joint venture with ONEOK (OKE).

The Knock-On Effect: The BANGL acquisition introduces downside risk for Phillips 66 (PSX) as MPLX shifts volumes away from PSX’s NGL infrastructure. Phillips owns the Sweeny fractionation complex and is acquiring the Robstown frac via the $2.2B EPIC acquisition. BANGL ownership gives MPLX more flexibility to reduce reliance on PSX systems.

PSX’s NGL infrastructure. Phillips owns the Sweeny fractionation complex and is acquiring the Robstown frac via the $2.2B EPIC acquisition. BANGL ownership gives MPLX more flexibility to reduce reliance on PSX systems.

Rigs:

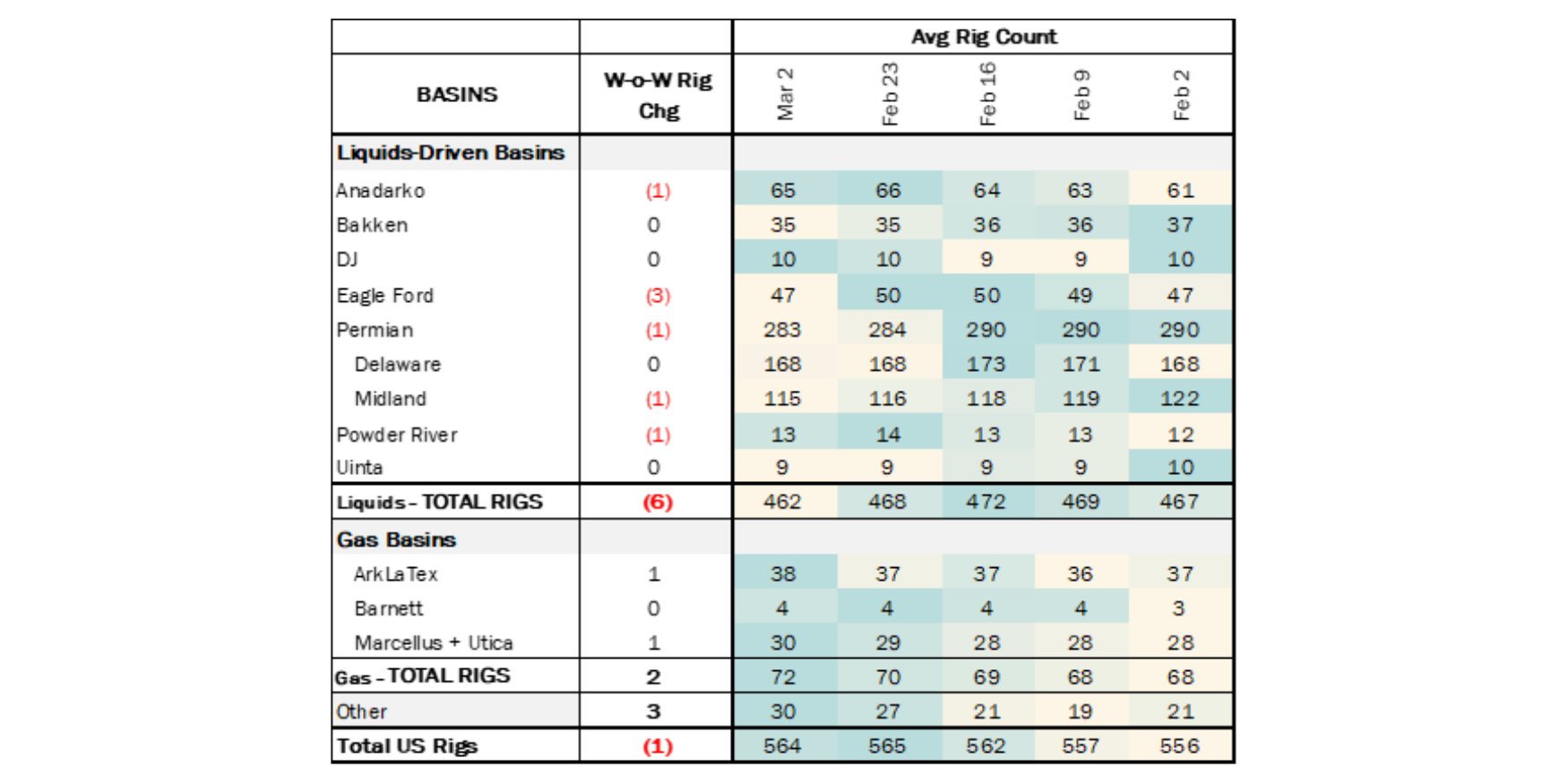

The total US rig count decreased by 5 during the week of February 16 to 543. Liquids-driven basins decreased by 6 W-o-W to 457.

- Permian (-6):

- Midland (-4): Exxon, Diamondback Energy, Chevron, Civitas Resources

- Delaware (-2): Mewbourne Oil, Devon Energy

- Bakken (-1): Continental Resources

- DJ (-1): Chevron

- Anadarko (+1): Citation Oil & Gas

Flows:

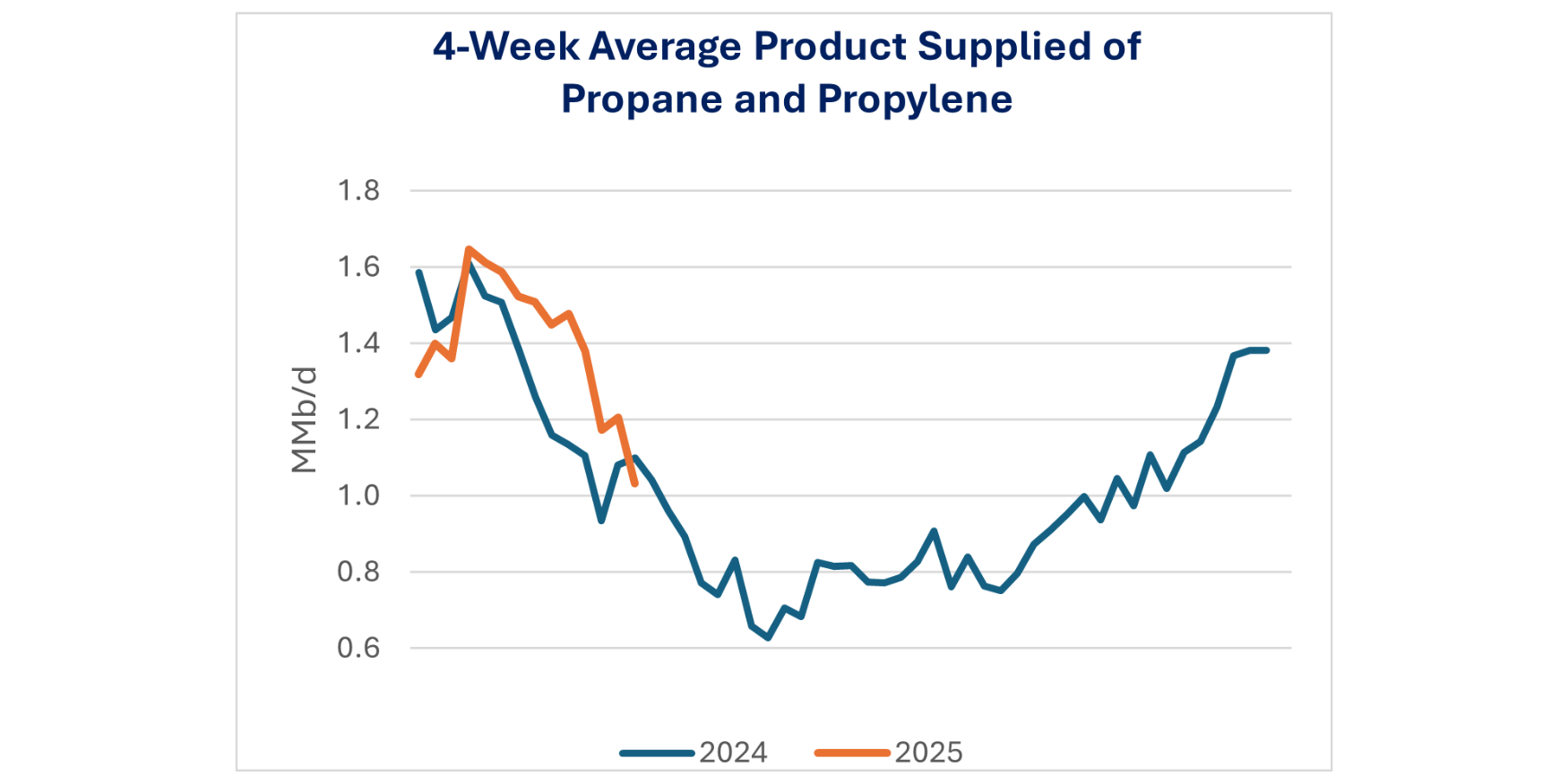

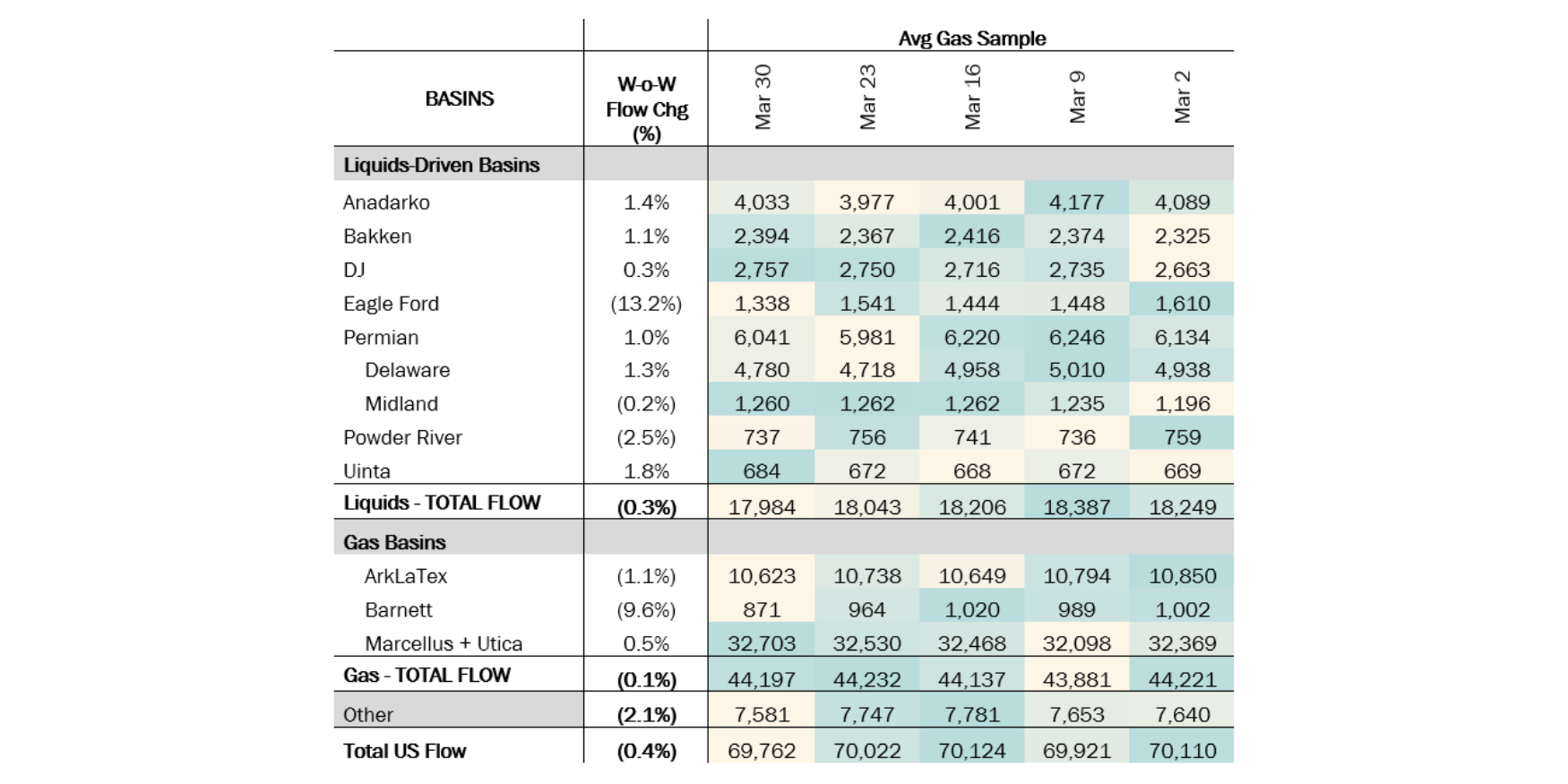

Total US pipeline volumes have increased from February's levels last week. Natural gas pipeline samples increased 3.4% W-o-W for the March 2 week, rising from 67.8 Bcf/d to 70.1 Bcf/d.

Liquids basins saw the most significant increases. The Anadarko led with a 26% W-o-W increase, followed by the Bakken and Powder River at 7% each and the DJ at 6%. This suggests strong production momentum in these basins recovering from winter freeze-offs. Other basin samples from the ArkLaTex (10,850 MMcf/d) and Permian (6,134 MMcf/d) showed steady but moderate growth. The Permian Basin continues to be a key production hub with a 4% increase in flows.

On the downside, the Barnett sample experienced a sharp 24% W-o-W decline, dropping from 1,312 to 1,002 MMcf/d. The Uinta remained stable with no change, while most other regions saw small gains.

*W-o-W change is for the two most recent weeks.

Data Points & Product Release Calendar:

-1.png)

-1.png)

-3.png)