Executive Summary: Rigs: The total US rig count decreased by 6 rigs for the June 2 week, down to 558 from 564. Flows: The U.S. interstate gas sample was up 0.4 Bcf/d (1%) W-o-W for the week of June 16. Infrastructure: More NGL fractionators in the U.S. Gulf Coast are needed. Purity Product Spotlight: The weekly data on U.S. Exports of Propane & Propylene is up by 20% so far in 2Q24 vs. 2Q23.

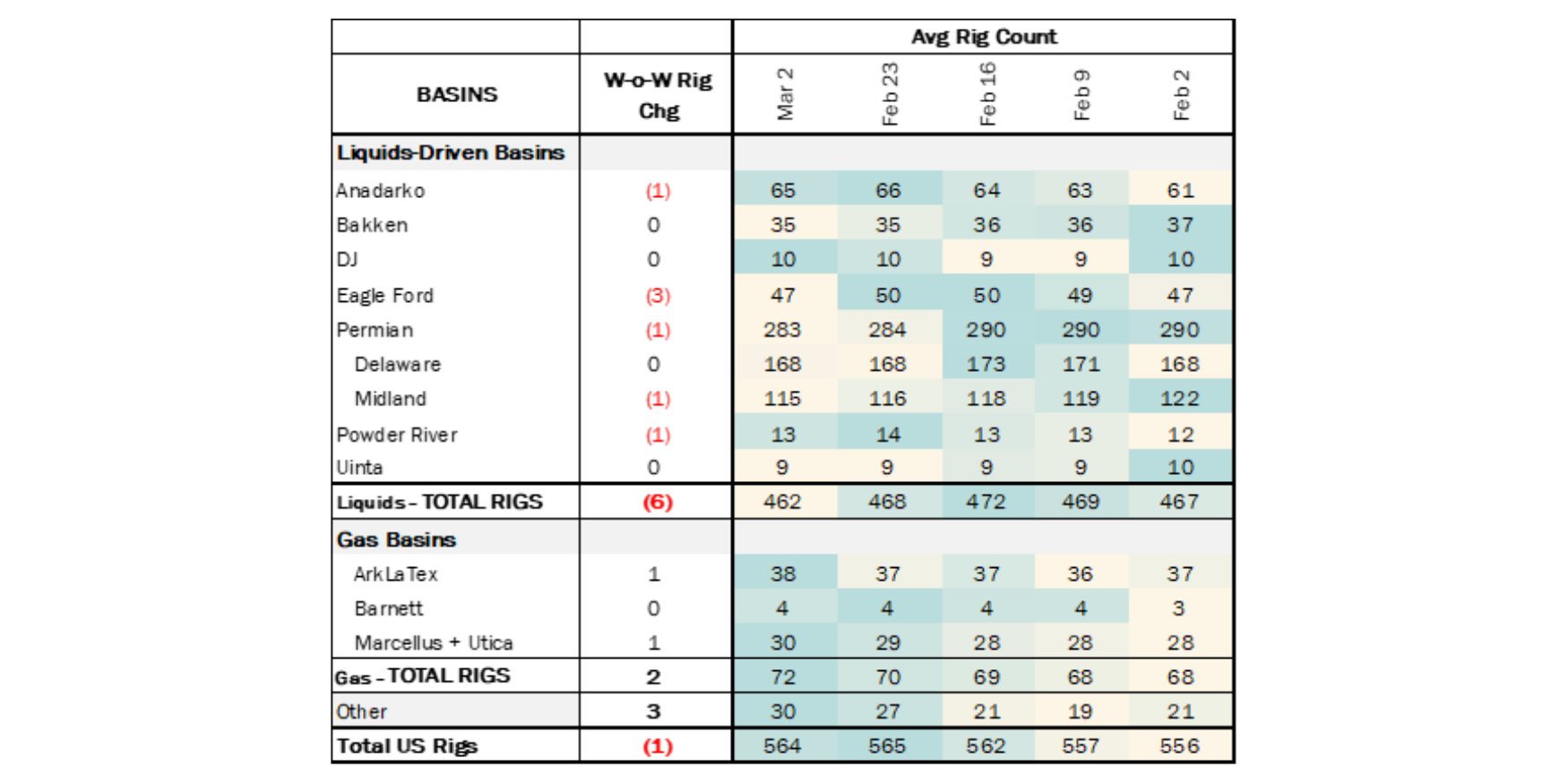

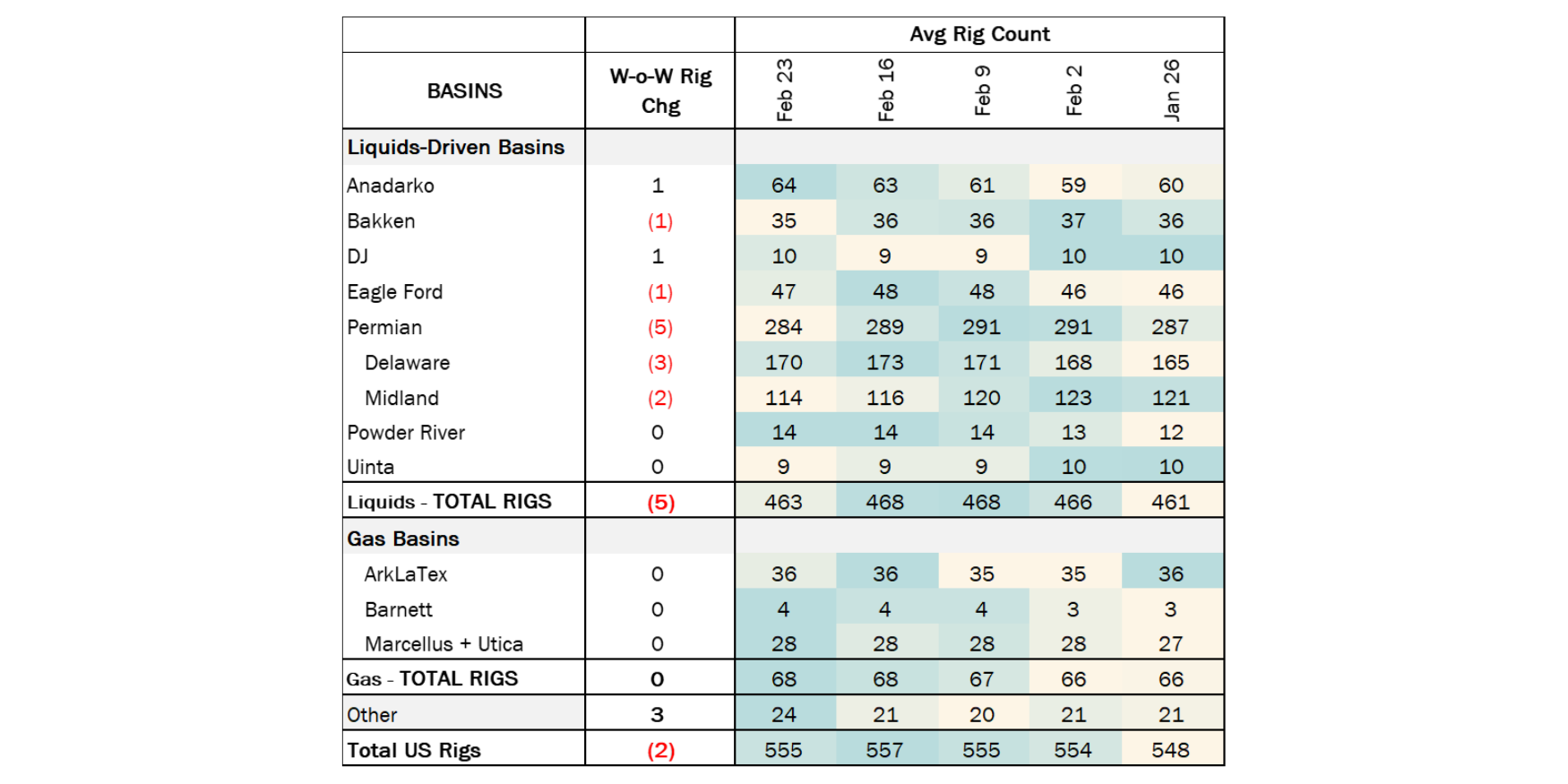

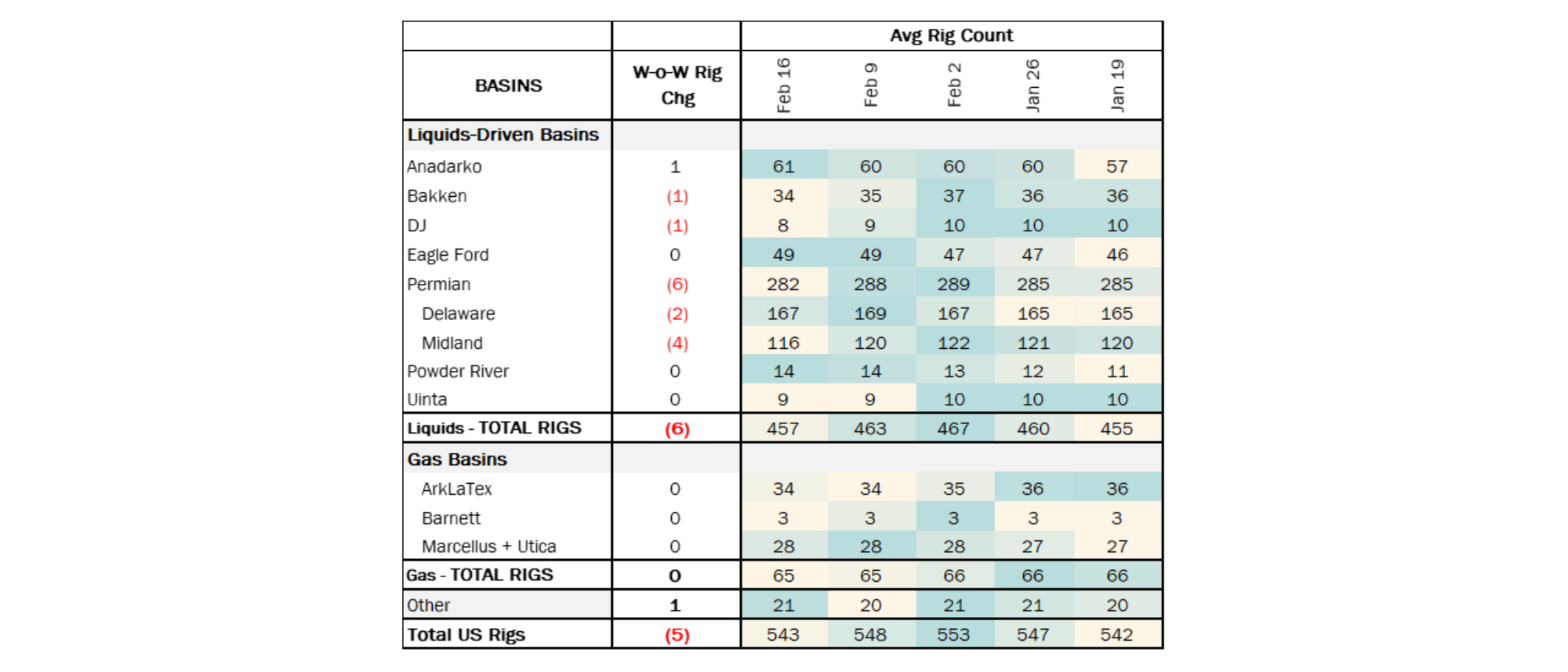

Rigs: The total US rig count decreased by 6 rigs for the June 2 week, down to 558 from 564. Liquids-driven basins drove the decline, down 7 rigs W-o-W to a total of 455. The Permian decreased 4 rigs W-o-W, losing 2 in the Delaware and the Midland. The Eagle Ford gained 2 rigs and the Anadarko lost 2 W-o-W.

In the Delaware, operators EOG Resources and Conoco Phillips each subtracted 1 rig. Exxon and Endeavor Energy operating in the Midland each removed 1 rig. Eagle Ford operators EOG Resources and CML Exploration both added 1 rig W-o-W.

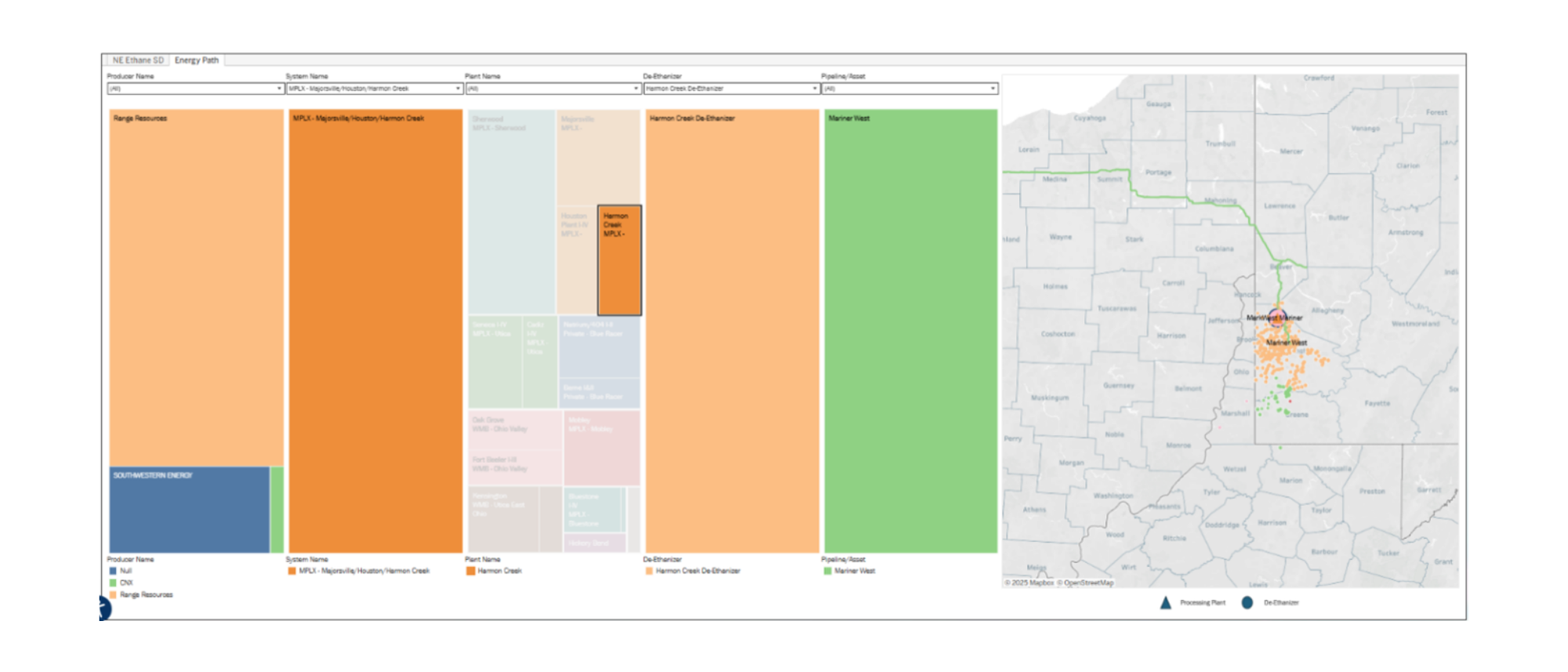

Flows: The U.S. interstate gas sample was up 0.4 Bcf/d (1%) W-o-W for the week of June 16. Gas-driven basins remain relatively flat. The prior trend of declines in Haynesville (ArkLaTex) and Northeast (Marcellus + Utica) seem to have ceased. EQT brought ~1 Bcf/d of Northeast production back online in late May due to stronger prices and in preparation for the start-up of Mountain Valley Pipeline (MVP).

Samples in liquids-focused basins increased slightly 0.4 Bcf/d (2%) W-o-W. The sample in the Permian suggests that production in the basin has remained relatively flat, but there has been rerouting between interstate and intrastate pipelines as capacity constraints on egress pipelines continue in the region. The flow restrictions, as shown in our latest Permian Supply and Demand report, should keep Waha trading at a steep discount until the new Matterhorn pipeline begins. We anticipate Matterhorn will start taking line-fill in July.

Despite rig counts dropping in the Delaware because of M&A activity, EDA expects efficiency gains among the top producers will offset the impact. EDA forecasts 1.2 Bcf/d of growth in 2024 and 2.3 Bcf/d of growth in 2025 of gross gas production.

In our May Macro Supply and Demand Forecast, EDA models Lower 48 gas production to average 102.4 Bcf/d in 2024, which is slightly above what we are expecting for the June release.

Infrastructure: More NGL fractionators in the U.S. Gulf Coast are needed. NGL frac capacity in the Mt. Belvieu market is barely keeping up with NGL y-grade supply growth. This is despite a number of announced capital projects to expand capacity. These projects include:

- 1Q25: ONEOK’s MB-6 project, capacity of 125 Mb/d.

- 1Q25: Targa’s CBF Train 10, capacity of 120 Mb/d.

- 2H25: Enterprise Product’s Frac Train 14, capacity of 195 Mb/d.

- 3Q26: Targa’s CBF Train 11, capacity of 150 Mb/d

These projects will become operational just in time as reflected by the sustained average utilization rate of 100% through 2027 (see figure below). We expect an additional frac expansion project or two will be announced in 2H24 adding to the 2026 build-out Targa started with the announcement of Train 11 on its 1Q24 earnings call.

Purity Product Spotlight: The weekly data on U.S. Exports of Propane & Propylene is up by 20% so far in 2Q24 vs. 2Q23. There are still a few weeks of reported data remaining in 2Q24, but the early indication is that U.S. Gulf Coast propane exports will match those gains with EPD, ET, TRGP, and PSX being the winners of strong international demand.

Since the weekly data point includes propylene, it’s not a perfect indicator of monthly propane exports specific to the USGC but the relationship has a correlation of 0.91 over the past 12 months.

Data Points & Product Release Calendar: